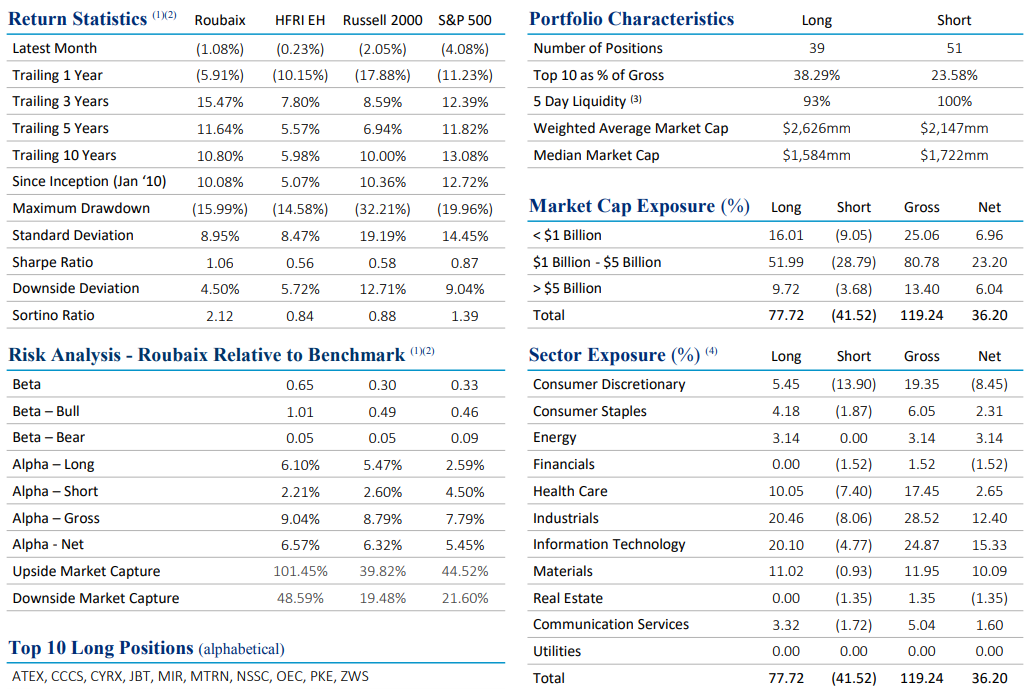

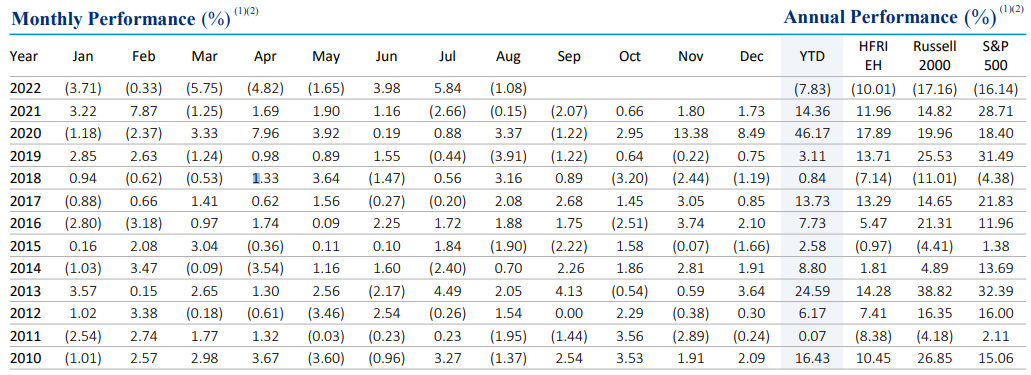

During August, the Roubaix Composite generated a net return of -1.08% relative to losses of -2.05% for the Russell 2000 TR Index and -0.23% for the HFRI Equity Hedge (Total) Index. On a year to date basis, the Composite generated a net return of -7.83% relative to losses of -17.16% for the Russell 2000 TR Index and -10.01% for the HFRI Equity Hedge (Total) Index. End of period net exposure was 36.20% compared to a 43.40% average since inception in January 2010.

The U.S. Federal Reserve was more straightforward in its commentary in August, alerting the market that they plan to increase interest rates until U.S. consumers feel enough “pain” to reduce demand and tame inflation. The translation is that the Fed wants lower housing prices and higher unemployment to ensure that any near-term decline in inflation is permanent, rather than the roller coaster ride of the Volcker era in the 1980s. The equity market simply got ahead of itself in July on the narrative that investors can simply look through continued rate hikes and an ensuing recession and buy stocks today for a potential rate cut in 2023. The Composite continues to invest long in select high quality growth stocks that are executing on their strategy today with little recession risk, along with “self-help” stories that should benefit from superior fiduciary decision making during any potential downturn. On the short side, we continue to monitor the energy situation in Europe for potential knock-on effects of a sharp reduction in industrial activity while broadly shorting U.S. consumer facing companies.