Spruce Point is pleased to issue a unique investment research opinion on Premier, Inc. ( “PINC” or “the Company”), a healthcare services organization.

Q2 hedge fund letters, conference, scoops etc

The report outlines how Premier, Inc faces 55% – 75% downside risk to approximately $8 to $15 per share. The report explores the potential devastating financial impact to Premier of two upcoming contract renewal periods where Spruce Point believes common sense and basic stewardship will dictate that member owners will significantly renegotiate their shareback rates to market levels now that their equity in Premier is fully vested.

Executive Summary

Short PINC: Spruce Point Sees 55%-75% Downside To $8-$15 Per Share

Premier, Inc. (“PINC” or “the Company”) is a group purchasing organization (GPO) which, due to a unique pre-IPO restructuring agreement, is temporarily generating twice the earnings which its business model can sustain organically. In exchange for rights to Premierequity, its “member owner” hospitals agreed to five or seven-year contracts through which they would accept administrative fee rebates (“sharebacks”) roughly half what they could get from competing GPOs. Those contracts are nearing expiration. Complacent sell side analysts, satisfied by Premier’s historical renewal rates among member owner hospitals accepting below-market sharebacks, forecast Premier earnings as though its prevailingeconomics are sustainable in perpetuity. However, with most member owner equity now having vested, hospitals with expiring contracts are far less incented to remain with Premier at sub-market shareback rates. Premier’s two largest members, whose below-market contracts are set to auto-renew on Oct 1, 2019, could announce their intention to opt out by next week (effective Oct 1, 2020), with remaining member owners set to announce the same as soon as Oct 1, 2020 (effective Oct 1, 2021). This would cause Premier to underperform FY22-23 consensus revenue by >26% and EBITDA by >50%.

- Unique Pre-IPO Restructuring Skews Company Economics: Premier was mutually owned by its member owner hospitals prior to its 2013 IPO. To free up cash for Premier to invest in ancillary services, these hospitals agreed to accept sharebacks of 30% –less than half the market rate of 60-75% –in exchange for equity in Premier and modest tax-related distributions. These agreements were structured to last only five or seven years. While most member owners signed to five-year deals renewed their agreements on similar terms, they most likely did so to avoid having to forfeit their as-yet unvested equity (~30% of their respective equity allocations at the time). Premier’s two largest GPO members, whose seven-year contracts expire on Oct 1, 2020, will have no unvested equity remaining by the time their deals are scheduled to expire, and therefore have far greater incentive not to renew their Premier-friendly deals on the Oct 1, 2019 opt-out deadline. As admin fees carry 100% incremental margins, changes in net admin fees have an overwhelming impact on Premier’s bottom line. The loss of Premier’s two largest GPO members or the restructuring of their agreements could cut Premier’s FY21 EBITDA by 9-17%.

- Increased SharebackCould Be Highly Material To Hospitals With Expiring Deals: Greater New York Hospital Association (GNYHA), Premier’s largest GPO member and a 10% Premier customer, is one of the hospitals whose contract is set to auto-renew next week. By analyzing tax filings, Spruce Point has found that, by receiving a market-rate shareback, GNYHA’s total income could increase by 33%. We believe that GNYHA may have a responsibility to its member hospitals to seek sharebacks more in-line with market rates, and anticipate that it may not renew its current agreement.

- More Opt-Outs Likely To Follow: Member owners which renewed their five-year agreements in Oct 2017 can opt out once again as soon as Oct 1, 2020 (effective Oct 1, 2021) without losing unvested equity. Should all member owners receive market-rate sharebacks of 60-75%, Premier’s FY22-23 EBITDA would be cut by more than half.

- Complacent Sell-Side Assumes Favorable Economics Can Last Forever: Premier’s ~95% renewal rate during its 2017 renewal cycle appears to have convinced the sell side that renewal risk is near-nonexistent. It ignores the fact that, unlike the 2017 renewal class, member owners whose contracts are due to auto-renew next week will have no remaining unvested Premier shares, and will therefore no longer have to accept below-market sharebacks for access to Premier equity. Analysts also appear to underestimate the prevailing market shareback rate by benchmarking against MedAssets. MedAssets, a GPO which was until recently public, reported superficially below-average sharebacks due to its practice of bundling GPO agreements with ancillary services. Our market intel confirms that themarket-level shareback is 60-75% and rising.

- Emerging Signs That Hospitals Are Prepared To Exit: Member owners are divesting of Class B shares at an accelerating pace, perhaps reflecting their knowledge that Premier’s economics are set to correct in the near future. Large hospitals such as Johns Hopkins Medicine have already exited, sacrificing some of their unvested Class B shares to do so. New language introduced in Premier’s most recent 10-K (filed Aug 2019) suggests that renewal risk is rising.

- PINC Shares Valued As Though Current Economics Are Sustainable: PINC trades at a 6.6x FY22 EV/EBITDA multiple based on the sell-side’s inflated future earnings estimates. Reverting member owner hospitals to sustainable market-level sharebacks would cut consensus FY22 EBITDA in half. PINCshould also trade at a lower EBITDA multiple, as Premier’s true underlying economics are worse than the market believes. Valuing PINC shares at 4-5x FY22 EBITDA on an estimate of EBITDA >50% below the Street would imply that PINC shares are worth $8-$15, 55%-75% below current levels. Losing hospitals to competing GPOs could result in even more downside.

Case Study: Premier Closely Mirrors Spruce Point’s Successful Call On 2U

Spruce Point believes that the circumstances facing Premier are extremely similar to those faced by education technology provider 2U (NASDAQ: TWOU) through 2018-19. In July 2018, Spruce Point published a “Strong Sell” recommendation on 2U, Inc. (NASDAQ: TWOU) which showed that the company’s tuition “take rate” (i.e. revenue share) on its online degree programs was under significant pressure: while 2Uclaimed historical take rates of over 60%, our FOIA requests demonstrated that intense competition had brought the market rate down to ~40%. Sell-side analysts nonetheless continued to assume that 2U could maintain its historical take rate until only recently, when management admittedonits Q2 earnings call that its core business was under fundamental pressure. The stock fell more than 60% the following day. Spruce Point believes that the circumstances facing Premier are very similar: while the sell side believes that Premier’s above-market shareback rates can last indefinitely into the future, Spruce Point finds evidence that near-term catalysts could force Company economics back in-line with the rest of the market.

Spruce Point Claims on 2U July 2018

- 2U take rate under heavy pressure with intensifying competition

- Margin pressure with continued shift towards short-course programs

- Sell side inappropriately modeling 2U economics as though historical margins were sustainable

TWOU CEO July 2019 Q2 Earnings Call

“…we’re adjusting our executional modelagainst the dynamic of this mainstreaming of online education in a way that meets this new market dynamic. Competition for students has increased. Programs will be slightly smaller than they were in the past.”

A Brief Primer On GPO Economics

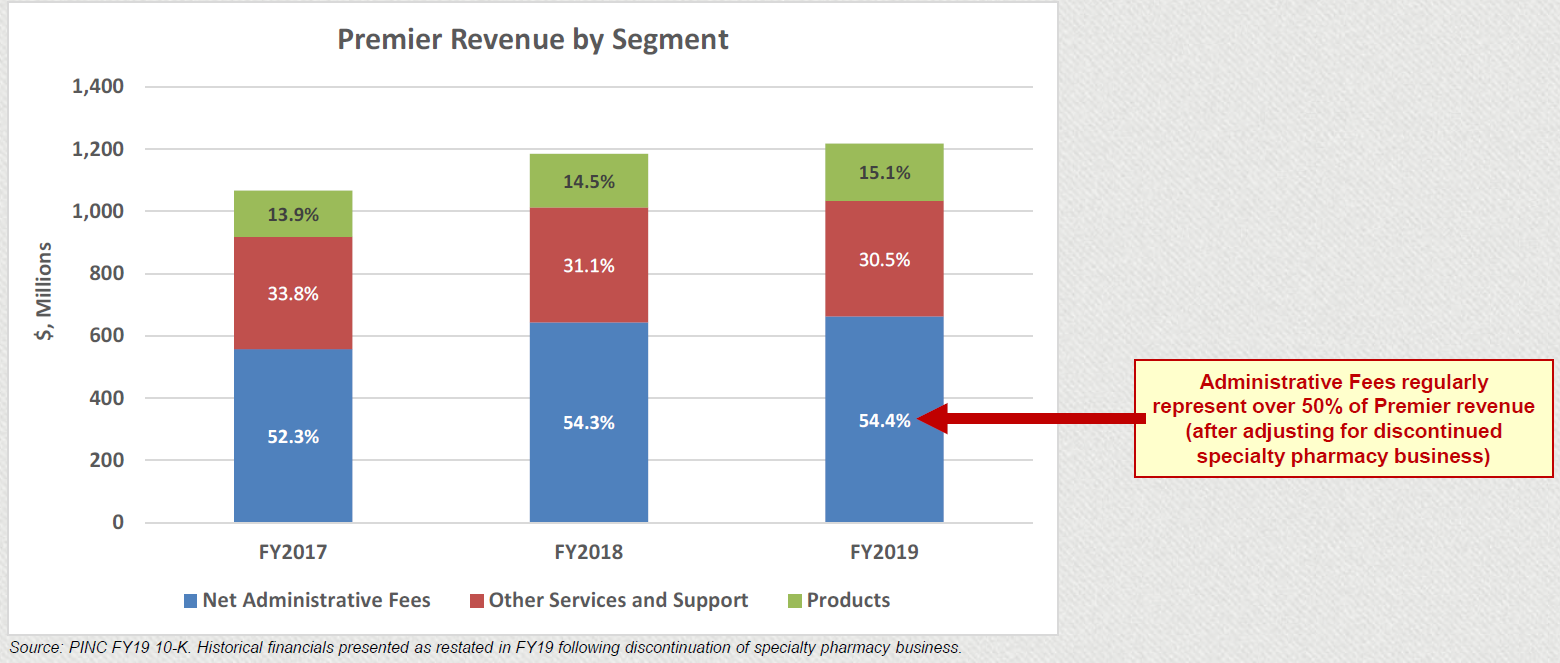

As a group-purchasing organization (GPO), Premier secures vendor discounts for its hospital members through the force of their collective purchasing power: per its 10-K, Premier represents more than 4,000 U.S. hospitals and health systems and over 175,000 other organizations as a GPO. As do other GPOs, Premier also generates revenue of its own by charging vendors an “administrative fee” of roughly 1.0% to 3.0% on product purchases. After returning a percentage of these fees to member hospitals as a “shareback,” or revenue sharing payment, the remainder is retained as GPO revenue. Premier also generates revenue through various other channels, including supply chain management,SaaS informatics offerings, and other consulting services (and, until recently, specialty pharmacy). Even then, following the recent divestiture of its specialty pharmacy business, administrative fees represent Premier’s most significant source of revenue by a meaningful margin, driving over 50% of sales ex-specialty pharmacy.

Read the full report here by Spruce Point Capital Management