The Lindy Effect: The expected remaining life of an item is proportional to its past life.

Q2 2020 hedge fund letters, conferences and more

“The Lindy effect is one of the most useful, robust, and universal heuristics I know.” – Nassim Taleb

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

In our last article, we presented the equity market returns as proxied by the S&P 500. We concluded that using U.S. equities as the proxy for equity market returns is incorrect. The primary issue is that proxying overall equity returns via U.S. equity returns is beset by survivorship and lookahead biases. U.S. equities in year 1900 were a much smaller component of the global markets than they are today. As of the date of this article, U.S. equities accounted for nearly 60% of global equity market capitalization. Generalizing from the U.S. relies on the extraordinary success its economy and financial markets enjoyed over the past 100 years, information that is available only in hindsight.

Shifting fortunes of sectors and industries

This leads us to another important risk that investment portfolios comprised of individual equities face. Investors are commonly told that they should buy and hold equities for the long-term. You only have to look at Warren Buffett for the success buy and hold investors can have.

If only it was that easy.

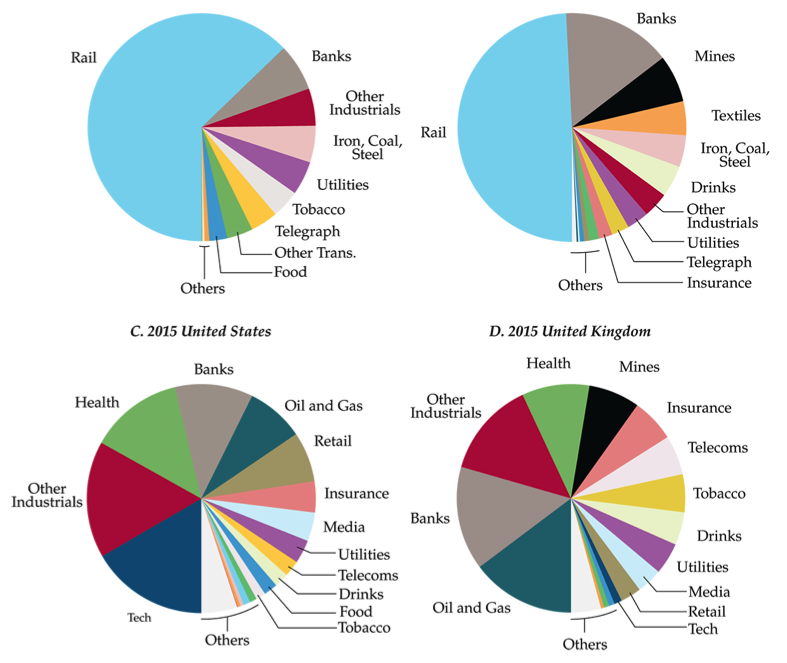

Much as the shifting fortune of countries, those of businesses and industries are ever evolving. Equity market benchmarks are constantly changing such that their composition, both in terms of industries and businesses, is ever evolving. Consider that in the U.S., railroads accounted for 63% of the total stock market value in 1900 and about 50% of the market value in the UK. Since then, railroads lost their prominence. They account for less than 1% of the market value in the U.S. and nearly 0% in the UK.

Figure 1 shows the composition of U.S. and UK’s equity markets in the years 1900 and 2015 as reported by Dimson, Marsh, and Staunton1. Even outside of railroads, there were significant shifts in the market’s composition. Indeed, of the U.S. firms listed in 1900, more than 80% of their value was in industries that are today small or extinct, with the corresponding number for the UK at 65%.

Figure 1: Relative sizes of word equity markets, 1900 vs 20162

Source: Financial Market History, Reflections on the Past for Investors Today, 2016

Read the full article here by Baijnath Ramraika and Prashant K. Trivedi, Advisor Perspectives