Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Q1 2020 hedge fund letters, conferences and more

Historically low bond yields threaten the diversification value of bonds in the traditional 60/40 allocation.

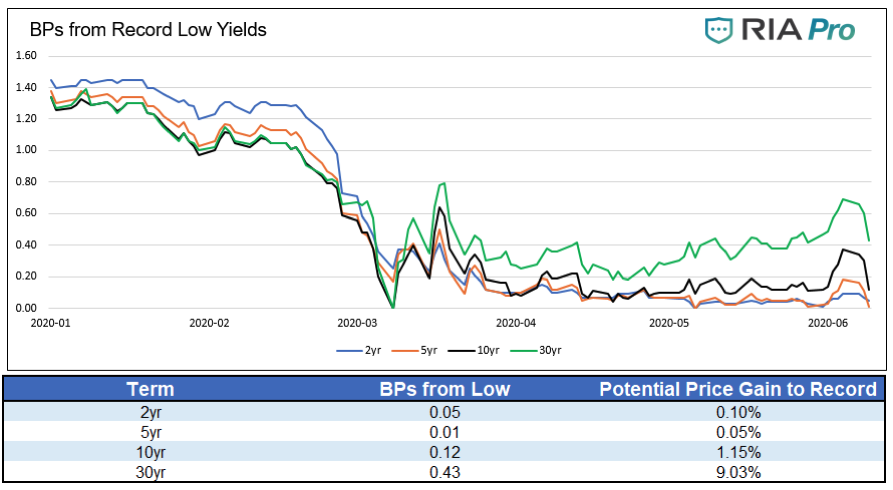

The graph below shows how many basis points benchmark U.S. Treasury securities are from their record lows. The table below the chart provides possible return scenarios if those bonds fall back to those records.

The potential upside in most Treasury bonds is marginal.

Do portfolio managers understand the repercussions of such a return outlook?

Traditional portfolio management

Many individual and institutional portfolios have allocations to stocks and bonds. For some investors, the ratio of stocks to bonds is static. For others, it vacillates based on risk preferences and market conditions. In any case, for investment advisors, pension funds and endowments, a required allocation to bonds is both an instinctive response and a legal requirement.

Bonds play an important role in portfolio management because they provide ballast to the risk exposure of equity markets. In the prior two bear markets, diversification using bonds proved very useful. In Greater Fool Bonds, I wrote the following:

Going back to what we described above as a balanced portfolio, investors benefited greatly during bear markets from the allocation to bonds in a simple 60/40 strategy (S&P/UST). For purposes of simplicity, we assume the full 40% allocation of bonds was in 10-year U.S. Treasuries. In most cases, investors would use other high quality fixed income categories such as mortgages and investment-grade corporates as well as a range of various maturities such as 2-year, 5-year, and 10-years.

The following analysis shows how allocations to bonds helped limit downside in the last two equity bear markets.

- From September 2007 through March 2009, a simple 60/40 (S&P 500/7-10 Yr. UST) portfolio returned -23.92%. An all-stock portfolio returned -45.76%. The 40% allocation to bonds reduced losses by 21.84%.

- From January 2000 through September 2002, a simple 60/40 (S&P 500/7-10 Yr. UST) portfolio returned –16.41%. An all-stock portfolio would have returned -42.46%. The 40% allocation to bonds reduced losses by 26.05%.

Heading into the two bear markets mentioned above, the 12-month average yield on ten-year U.S. Treasury bonds was 6.66% in 2000 and 4.52% in late 2007. At their lows, the yields fell to 3.87% and 2.43% for 2002 and 2008, respectively.”

A cursory glance at current yields highlights that those benefits are no longer available.

Read the full article here by Michael Lebowitz, Advisor Perspectives