Absolute Return Partners commentary for the month of October 2021, titled, “Why Much Wealth Must Be Confiscated.”

Q2 2021 hedge fund letters, conferences and more

By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. – John Maynard Keynes

- Why It Is US Inflation You Should Worry About

- The Fed’s Game Of Chess

- Inflation Peaks And Troughs Over Time

- Five Reasons Why It Is Time To Take Inflation Seriously

- Reason #1: Rapidly Rising Inflation Expectations

- Reason #2: Rising US Wages

- Reason #3: Rising Industrial Commodity Prices

- Reason #4: Bottlenecks And Other Supply Chain Distortions

- Why Inflation Is Akin To Confiscation Of Wealth

- Adding It All Up

Why It Is US Inflation You Should Worry About

Before I begin, let me caveat what is to follow by saying that this month’s Absolute Return Letter on inflation and confiscation of wealth is very US-centric, and there is a good reason for that. As you can see in Exhibit 1 below, US wealth-to-GDP has, since we emerged from the Global Financial Crisis in 2009, gone absolutely ballistic and is now – as at the 30th June – a whopping 623%.

Exhibit 1: US wealth-to-GDP (%)

Source: MacroStrategy Partner LLP

The long-term mean value of US wealth-to-GDP is about 380% so, at 623%, US wealth is now massively above what can be sustained longer term. There are some very good reasons why wealth cannot grow faster than GDP in the long run (based on economic growth theory) which I shall not bother you with. However, the fact stands – sooner or later, wealth-to-GDP will begin to mean-revert. Exhibit 1 covers US wealth only, as most other countries do not provide as much detail on wealth as the Americans do, but I can assure you that the US is an outlier in the context of wealth relative to GDP – at least in the OECD.

The biggest drivers of household wealth are (in that order) property, pension savings and holdings in private, typically family-owned, companies. Having said that, in most countries and particularly in the US, direct holdings of listed equities – i.e. holdings of listed equities other than those held in pension schemes – also make for a meaningful share of total wealth. Precisely for that reason, the rally in US equities in recent years accounts for much of the near vertical rise in wealth-to-GDP that Americans have enjoyed the last few years.

My point here is that, in the years to come, something will have to give to bring the long-term mean value of wealth-to-GDP back in line. I just don’t know what it is. Will property prices collapse? Will equities? Bonds? Possibly all of them? Or maybe none of them will collapse but, instead, GDP will continue to grow, whilst asset prices move broadly sideways so that, over an extended period of time, equilibrium will be re-established. It is impossible to say.

It is not only wealth that has grown to levels that cannot be sustained. The same has happened to debt. I regularly talk about debt supercycles, and I have argued for a few years that we are getting worryingly close to the end of the current debt supercycle. Debt can be destroyed by inflation, and it is in that context you should look at various central banks’ reaction to the recent pick-up in inflation. To me, it looks like central banks do indeed want to let some inflation loose. Otherwise, they would have taken more firm action already – particularly the Fed.

As is obvious from Exhibit 2, US inflation is in a league of its own at present. Of all the major OECD countries and regions, nowhere is inflation a bigger issue than it is over there right now. Below, I will argue that the two stories – excessive wealth growth and excessive inflation – are two sides of the same coin.

Exhibit 2: Consumer price inflation in various countries (%)

Source: Goldman Sachs Global Investment Research

Even if you never invest in the US, you should still read what is to follow. US financial markets are so big and so dominant these days that all markets will be affected if (when) the good fortunes in the US change. As an old Danish saying goes, when it rains on the priest, it dribbles on the bellringer.

The Fed’s Game Of Chess

Covid-19 has, for obvious reasons, been the main topic of the last 18 months, but a rather inconvenient inflation cocktail is brewing on the backburner, ready to cause havoc. This raises the all-important question – is the recent spike in inflation, as Fed Chairman Jerome Powell maintains, entirely transitory with few lasting effects, or are we flirting with mayhem?

The latest US consumer price inflation (CPI) report, whilst still raising a few eyebrows, leaned more towards Jeremy Powell’s side than the reports of previous months had done. Yes, core CPI is still running at an uncomfortably high level around 4% year-on-year, but (i) it was lower than in July and (ii) it was significantly below expectations. It is therefore tempting to hand the victory to Powell.

Under normal circumstances, I would probably give Powell and his fellow governors more credit that I am prepared to do at this moment in time. For starters, as I have already insinuated, I suspect that central bankers want inflation to rise, even if they are reluctant to admit it. The mountain of debt continues to grow, and having a bit of inflation is the least painful way to destroy some of all that debt again. The Fed Governors know this, although they’ll never admit that staying behind the curve is a deliberate strategy.

Secondly, we have never really escaped the ghosts of the Global Financial Crisis. Interest rates continue to be extraordinarily low, propping up wealth in society but also bolstering inflation and raising the gap between rich and poor which leads to all sorts of other problems – populists running more and more countries being just one of them.

Thirdly, COVID-19 has upset many of the mechanisms that, under normal circumstances, would validate Powell’s claim. The number of bottlenecks and other supply chain problems in industry is now running at excessive levels, and while this is a truly global problem, it causes the most inflation in those countries where the output gap is the lowest, i.e. the US.

Jeremy Powell, together with the majority of members on the Fed’s Open Market Committee, may be playing a rather hazardous game of chess, though, when arguing the spike is transitory. I recently gave my thoughts to ARP+ subscribers as to how to structure a portfolio, should inflation turn out to be more than a transitory problem. If you are a subscriber to ARP+ and haven’t listened to it yet. I strongly recommend you do so. You can find it here.

Inflation Peaks And Troughs Over Time

Since the Napoleonic wars of the early 19th century, we have been through several major spikes in inflation with the latest occurring in 1980 (Exhibit 3). As you can see, each major inflation peak has exceeded the previous peak in terms of severity, and each major inflation trough has been lower than the previous trough. Precisely why that is, I am not sure. Could it be the result of rising living standards, meaning that whatever is in demand is wanted by more and more people around the world? Maybe. Could it be the result of greater international interaction, leading to demand being more coordinated? Maybe. Or could it just be a coincidence? Maybe. If any of our readers have a view on this, I would be curious to hear what you think.

Exhibit 3: US commodity price index since 1795

Source: Janus Henderson

Since the end of World War II, Americans have ‘enjoyed’ six episodes of 5%+ annual CPI. The last of these episodes occurred just before the onset of the Global Financial Crisis, when sharply rising gas prices led to CPI in the US rising by 5.6% year-on-year in the summer of 2008 (Exhibit 4). As you can see, the current episode is bidding to join that club.

Exhibit 4: US CPI since World War II (%)

Source: The White House

Five Reasons Why It Is Time To Take Inflation Seriously

Now, there are some pretty powerful reasons to believe Powell could be wrong when claiming that inflation will soon fade again. Having said that, before I share those reasons with you, let me point out why I think it is in everybody’s interest for the Fed and other central banks to sit on their hands for a while.

Powell cannot publicly declare that it is now official Fed policy to stay behind the curve, as it will dramatically affect inflation expectations which could be devastating. Instead, he may have chosen to play a very shrewd game, where the tactic is to destroy debt by allowing inflation to run a little bit higher than what we would normally consider appropriate and by not raising interest rates as much as he would normally do, given what is happening to inflation.

This is a high-risk strategy which could backfire spectacularly if he gets it wrong. On the other hand, he could go down in history as the central banker who managed to wipe the debt slate clean, provided the strategy works. A noteworthy consequence of such a strategy, though, is that significant amounts of wealth will be confiscated, which is what inflation does to wealth. As that happens, wealth-to-GDP will begin to mean-revert towards its long-term mean value, hence why confiscation of wealth and destruction of debt are two sides of the same coin.

Reason #1: Rapidly Rising Inflation Expectations

Inflation expectations drive future inflation more than anything else, hence why central bankers almost always spin the inflation story as gently as they can. They don’t want inflation expectations to rise. The logic is fairly simple. Should inflation expectations rise – as they currently do – employees will start demanding higher salaries, and businesses will begin to raise prices. As we have learnt in the past, it is a vicious circle which is hard to escape from.

Precisely for that reason, the fact that inflation expectations have indeed risen in recent months, both amongst households and businesses (Exhibits 5a-b) is a stark warning to Powell & Co. If rising inflation expectations turn out to be more than a blip on the curve, the recent spike in inflation may not be as transitory as Powell claims it is. I will certainly keep my eyes glued to the expectations data over the next few months. If the sharply rising expectations curve doesn’t soften relatively soon, I think you can forget all about the current bout of inflation being transitory.

Exhibit 5a: US household inflation expectations

Source: Goldman Sachs Global Investment Research

Exhibit 5b: US business inflation expectations

Source: Goldman Sachs Global Investment Research

Reason #2: Rising US Wages

Another key driver of inflation is wage growth, and a particularly good indicator is the leading indicator provided by Goldman Sachs in the wage survey they do regularly. The leading indicator is represented by the red line in Exhibit 6 below. As you can see, at present, it is rising quite sharply and is currently hovering around 4%. It is not yet in critical territory, but rising inflation expectations may cause further upward pressure on wages.

Exhibit 6: US wage tracker (%)

Source: Goldman Sachs Global Investment Research

Reason #3: Rising Industrial Commodity Prices

As you saw in Exhibit 3, there has always been a powerful link between commodity prices and inflation. In four of the six commodity supercycles we have been through since 1795, a peak in commodity prices has coincided with a peak in inflation. Only the post-WW II supercycle peak and the 2008 supercycle peak did not lead to a new peak in inflation.

Now, with energy prices, industrial metals prices and agricultural prices on the rise again, and with all three of them significantly above pre-pandemic levels (Exhibit 7), it is not unreasonable to worry about the impact rising commodity prices may have on inflation.

Exhibit 7: Energy, industrial metals and agricultural prices

Note: January 2020 = 100

Source: Goldman Sachs Global Investment Research

So far, the poorest countries have suffered the most (see for example this report) whereas, in the OECD, the main problem so far has been limited availability of various goods, but that can quickly change. Take for example the sharp rise in gas prices all over the OECD at the moment, and imagine what impact that is going to have on consumers’ disposable income as we approach Christmas.

Reason #4: Bottlenecks And Other Supply Chain Distortions

That brings me to the next reason – bottlenecks and other supply chain distortions. Allow me to share a personal story with you. My wife and I are currently house hunting and recently identified a well-located house. The only problem was that it required a new kitchen. My wife has fallen in love with a Danish kitchen manufacturer called Hanstholm Køkken, so I called them and asked if the horror stories going around were true – that it could take more than a year to have a new kitchen installed.

“Not correct as far as the kitchen itself is concerned”, the gentleman said to me, “but beware of long delivery times on appliances”. Apparently, slow semiconductor deliveries may cause delays of 6-12 months on various refrigerators, freezers and ovens, etc. It is no different from the stories you hear from the automobile industry at present.

Chip makers in Asia are struggling big time to meet post-Covid demand, and the problems are exacerbated by the fact that virtually the entire world is returning to near-normal conditions at the same time after having spent the last 18 months in the freezer (no pun intended).

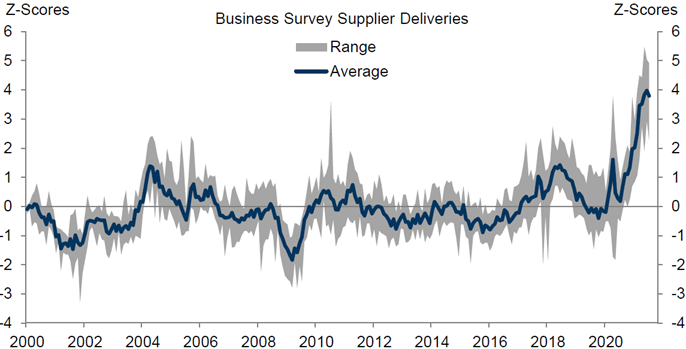

This is not only a great dinner story – it is a massive problem for the real economy (Exhibit 8). The chart below represents US bottlenecks only, but the problem is truly global in nature. A relatively small number of chip makers in the Far East supply semiconductors to the entire world and, when they struggle, it will have a meaningful effect on everything.

Exhibit 8: Business supplier deliveries

Note: Chart based on survey

Source: Goldman Sachs Global Investment Research

Why Inflation Is Akin To Confiscation Of Wealth

Inflation destroys purchasing power – simple as that. You shouldn’t worry about a modest pop in inflation, say, from 2% to 4%, which is roughly where we are now. That has happened relatively frequently, although not in recent years, and has only had a limited impact. In the bigger scheme of things, such a rise in inflation is largely inconsequential.

What you should worry about is a return of the conditions we last experienced in the late 1970s. I vividly remember how much inflation back then limited our ability to do what we wanted to do and how much wealth was confiscated. One could argue that at least the value of your property is likely to hold up, even when measured in real terms, should the inflation genie be let out of the bottle, and that is correct, but overall, much wealth will still be confiscated.

This was precisely the argument of John Maynard Keynes, arguably the greatest economist of all time, when he discussed inflation and its impact on wealth. In that context, it is noteworthy that the Federal Reserve Bank, in its mission statement, assures the nation that it is the Fed’s responsibility to “provide the nation with a safer, more flexible, and more stable monetary and financial system”. How that is compatible with deliberately staying behind the curve, as I argued earlier, I don’t know, but stranger things have happened.

The Federal Reserve Bank was created on the 23rd December, 1913, with the signing of the Federal Reserve Act by President Woodrow Wilson. Now, a century later, the purchasing power of a 1913 dollar is only a few cents (Exhibit 9). The chart is admittedly almost 15 years old, but an updated version wouldn’t lead to any other conclusion. This is why inflation is akin to confiscation of wealth.

Exhibit 9: Value of $1 in 1913 dollars

Source: US Bureau of Labor Statistics, The Market Oracle

Adding It All Up

By allowing inflation to run for a while, the objective is to destroy debt rather than to confiscate wealth. However, the latter is an unintended consequence of the former. I am often asked what is likely to kickstart the mean reversion process of wealth-to-GDP, and maybe this is the answer. Maybe central bankers around the world have decided to puncture the debt bubble through inflation, and the inevitable consequence of that will be a significant amount of wealth confiscation.

As I have stated frequently in the Absolute Return Letter, debt can only be destroyed in two ways – either through inflation or through default. As we all learnt in 2008, debt destruction through default is not a pleasant outcome, so it shouldn’t surprise anyone, if central bankers have chosen the inflation route instead.

Before I finish, just one more observation. Not everyone agrees that there is anything to worry about re inflation. See for example this article in the Financial Times from mid-September. The argument is essentially that today is more akin to the 1950s, which enjoyed rapid economic growth without inflation getting out of control, than it is reminiscent of the 1970. In other words, there is little to worry about, according to the author.

I am paid to worry about these sorts of things, though, so I don’t accept all those arguments at face value, but I obviously listen. Anything else would be plain stupid. I am not yet an inflation ‘convert’. To me, it is a risk more than a fait accompli, but expect me to spend more time on inflation over the next year or two than I have done in many, many years.

Niels C. Jensen

1 October 2021

Related Investment Megatrends

Our investment philosophy, and everything we do at ARP, is driven by the long-term Investment Megatrends which are identified and routinely debated by our investment team. Read more about related Megatrend/s for this article:

Mean Reversion of Wealth-to-GDP

About the Author

Niels Clemen Jensen founded Absolute Return Partners in 2002 and is Chief Investment Officer. He has over 30 years of investment banking and investment management experience and is author of The Absolute Return Letter.

In 2018, Harriman House published The End of Indexing, Niels’ first book.

Article by Absolute Return Partners