“If we pay attention to cycles, we can come out ahead. If we study past cycles, understand their origins and import, and keep alert for the next one, we don’t have to reinvent the wheel in order to understand every investment environment anew. And we have less of a chance of being blindsided by events. We can master these recurring patterns for our betterment.”

“If an investor listens in this sense, he will be able to convert cycles from a wild, uncontrollable force that wreaks havoc, into a phenomenon that can be understood and taken advantage of: a vein that can be mined for significant outperformance.”

– Howard Marks, Mastering the Market Cycle

Q3 2019 hedge fund letters, conferences and more

Howard Marks, CFA, is Co-Chairman of Oaktree Capital—the firm he founded in 1995—and one of the most successful hedge fund managers in the business. I wrote about him here in June.

Years ago, my firm ran a leveraged multi-manager hedge fund strategy. We worked closely and successfully with Marks. You may be familiar with his popular letter titled, “Memos from Howard Marks.” You can find them here. If you don’t know much about him, you’ll get to know him through his writing and his insights and, I believe, he will help you to be a better investor. But don’t let it go to your head.

All investors face challenges when it comes to how to play the cards they’re dealt—no matter how experienced they are. The late financial historian, economist, and father of the efficient-market hypothesis, Peter L. Bernstein, captured what I find to be the difficulty and simplicity of investing:

A lot of investors feel it isn’t hard, they just don’t know how. Because the more you think this is easy, the more you persuade yourself that you can take the heat. And then, the sooner the oven gets hot, the more shocked you are and the worse you get burned. After 50 years in the investment business I still haven’t got it all clear.

And that’s okay, because I understand that I haven’t got it figured out. In a hundred years, I won’t have it all figured out. Understanding that we do not know the future is such a simple statement, but it’s so important. Investors do better where risk management is a conscious part of the process. Maximizing return is a strategy that makes sense only in very specific circumstances. In general, survival is the only road to riches. You should try to maximize return only if losses would not threaten your survival and if you have a compelling future need for the extra gains you might earn.

That’s great advice. In On My Radar, I try my best focus in on the global macro environment, valuations, investment sentiment, central bankers, market cycles, and risk management. My investment understanding has certainly grown since I first started out at Merrill Lynch back in 1984.

“If we pay attention to cycles, we can come out ahead.”

“Understanding that we do not know the future is such a simple statement, but it’s so important. Investors do better where risk management is a conscious part of the process.”

Sage advice. It’s about cycles, probabilities, and risk management.

Where do we sit in the cycle?

The current economic cycle is more than 10 years old—the longest on record. By almost all measures, equity market valuations are near record highs. The length of the cyclical bull market is now the longest in history. And most significant: we sit at the end of a long-term debt accumulation cycle. Moments like this one are problematic. That’s the bottom line.

I have just a few data points to share with you this week. We’ll take a look at some forward leading indicators on the U.S. economy, valuations, and then some trends in corporate earnings that we should keep on our radars.

Let’s start with the Cass Freight Shipments and Expenditures Indexes. These indexes are “two of the strongest proxies for what is happening in the overall U.S. freight markets, and as a result they are strong predictive indicators for the U.S. economy… Based on the trend since the beginning of the year, but especially the data over the last five months, the Cass Shipments Index is signaling that GDP may be negative, or at least come close to being negative, in Q3. If it does not, since reported GDP often lags the economic activity represented by freight flows, continued weakness in the Cass Shipments Index at the current magnitude should result in a negative Q4 GDP.” (Source: Cass Freight Index Report.)

Here are some key data points from the Cass report (hat tip to Pat Watson of Mauldin Economics for sharing the following):

- Weak volume and pricing in important air, rail, and truck markets point to economic contraction.

- Low spot transportation prices are consistent with disappointing housing starts and lackluster auto sales.

- Asian airfreight patterns suggest the region is on the verge of recession, if not already in one.

- Inbound air volumes to Shanghai have plummeted. This suggests lower demand for the components Chinese factories assemble into high-value tech devices.

- In the US, dry van volume is in line with capacity, suggesting the consumer economy is still relatively healthy. But seasonally, we should be seeing higher volume right now, and its absence is troubling.

- Whether we blame normal cycles or trade disputes, growing evidence from freight flows says the economy is beginning to contract.

Meanwhile the Federal Reserve has been cutting rates and now intends to restart QE.

It sounds bleak. Yet, when Susan and I visited Penn State this past week, she noted the many “help wanted” signs hanging in shop windows as we walked around the downtown business district. And while one could argue that college towns are recession proof, I’m also seeing large cranes in every city I visit—building activity is booming.

On Valuations

We have been talking about the coming pension crisis. You may have seen the news about General Electric’s pension and their plans to freeze their defined benefit plan. Meaning no mas, fini, done. This is just one marker on the road. John Mauldin wrote an excellent piece on the coming pension problems. You can find a link to his full piece titled, “Our Nuts are in Danger,” here.

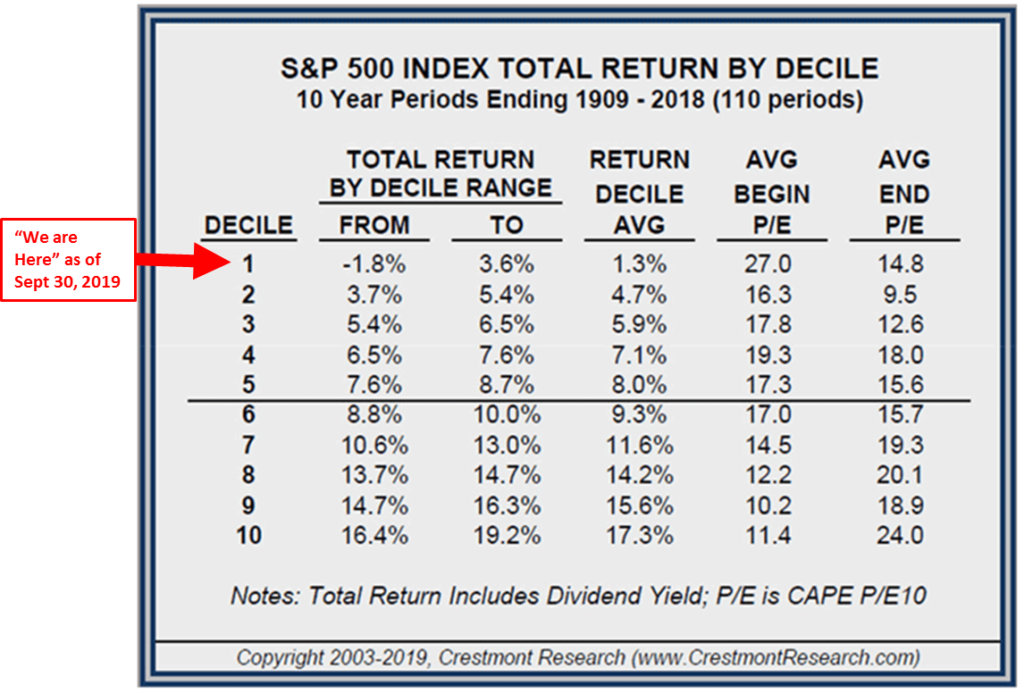

The average state pension is 50% underfunded, and the coming returns are not going to hit the 7% return bogeys most plans are calibrating. As you can see in the next chart from Crestmont Research, 10-year equity market returns are in the -1.8% to 3.6% range (annualized). With Baby Boomers nearing the “pay me” date and return probabilities well below the 7% targets, the pension crisis advances.

Source: Crestmont Research

We will have more GE-like announcements in the future, and face higher state and local taxes to cover those underfunded promises. More likely than not, benefits will be lower too.

Grab a coffee and find your favorite chair. You’ll find a chart showing the current path of corporate earnings—another late cycle data point—as well as the most recent Trade Signals. As Bernstein advised, “Maximizing return is a strategy that makes sense only in very specific circumstances. In general, survival is the only road to riches.” Keep your risk management processes firmly in place.

If a friend forwarded this email to you and you’d like to be on the weekly list, you can sign up to receive my free On My Radar letter here.

Follow me on Twitter @SBlumenthalCMG

Included in this week’s On My Radar:

- Weak Earnings Growth Prior to Recessions

- Trade Signals – The Trend Remains Your Friend

- Personal Note – Looking for W’s

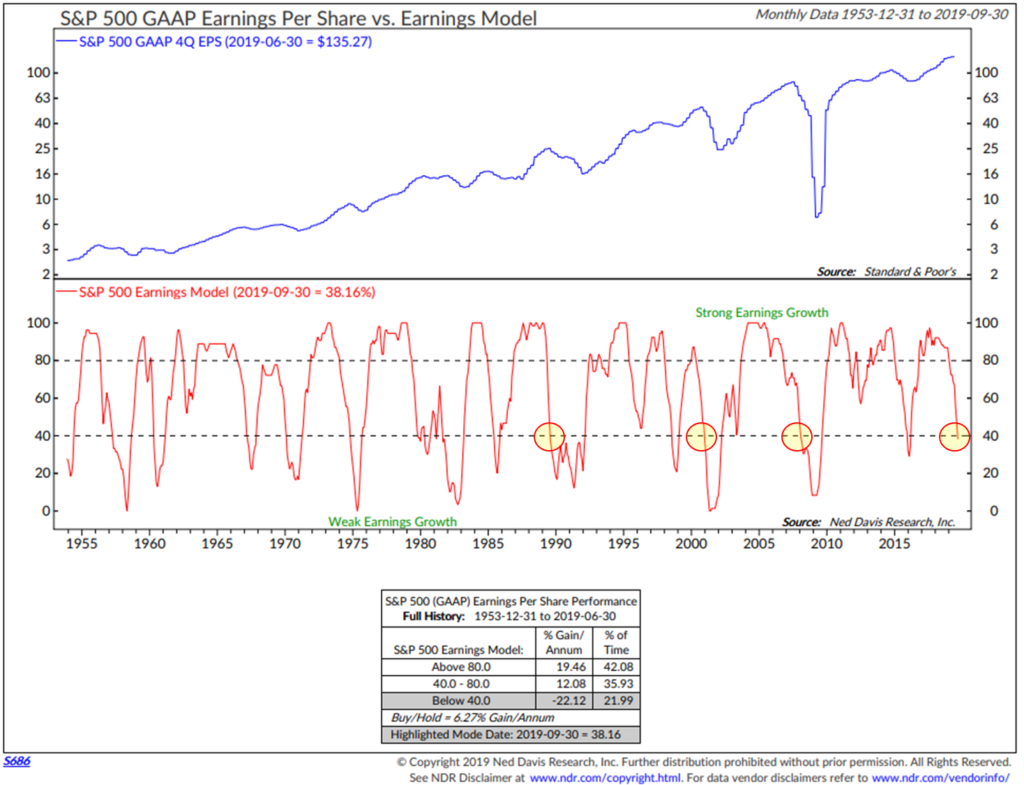

Weak Earnings Growth Prior to Recessions

Here’s how to read the chart:

- The chart breaks earnings growth into two main categories: Strong Earnings Growth and Weak Earnings Growth.

- Focus in on the yellow circles.

- Ned Davis Research’s Earnings Per Share vs. Earnings Model shows the trend has just moved into the Weak Earnings Zone.

- Finally, note the grey shaded area in the data box in the bottom of the chart. It shows the gain per annum of the S&P 500 index based on the trend in earnings. We are in the below 40 “Weak Earnings Growth” zone: -22.12% per annum.

Source: Ned Davis Research

Trade Signals – The Trend Remains Your Friend

October 16, 2019

S&P 500 Index — 2,990

Notable this week:

The weight of trend evidence for the U.S. equity, high quality fixed income and gold markets remains bullish. Extreme investor sentiment also supports the bullish trend. The downtrend in High Yield bonds has stalled and turned up… though not yet in a buy signal. There is no change in the recession watch data. I’ll be writing about the most recent Cass Freight Index report in Friday’s On My Radar. It has historically been a good leading economic indicator for the economy. That data is weak and shows the economy is slowing. Cass believes the data points to Q3 2019 GDP data coming showing zero to negative growth. We’ll also take a look at recent earnings data. The equity bull market remains aged and overvalued; however, the weight of trend evidence remains positive.

Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Click here for this week’s Trade Signals.

Personal Note – Looking for W’s

Susan, son Matthew, and I took a trip to Penn State Monday evening to watch son Kyle perform in She Kills Monsters. Kyle’s a sophomore theater student and this is the first show he’s been in since his high school days (freshmen are not allowed to perform). We were excited—really excited—to watch Kyle again. If you have a child or grandchild in theater you probably know the feeling.

The show was about a girl who lost her family in a car crash. She was never close with her younger sister, who was deeply introverted. She felt bad about that—the loss of her sister and, of course, the loss of her parents. After finding her sister’s Dungeons and Dragons (DnD) journal, which chronicled the mythical game the girl often played in her mind, she asked a DnD master to help her decode the journal to try to learn more about her sister and better connect with her in some way. By reading her sister’s journal and playing DnD, she was able to vanquish the emotional demons she had been harboring and begin to heal. We really enjoyed the show, and look forward to many more. Put that in the fun column.

I’m writing today’s OMR in the early morning hours from Indianapolis. I took a quick flight out for dinner and morning meetings with several advisor partners. Dinner was held at the Dallara IndyCar Factory near the Indianapolis Motor Speedway. Dinner was delicious–the smell of motor oil not so much.

I was both surprised and thrilled to run into Geoff Eliason from Peak Capital. Geoff and his team are some of the strategists in our CMG Mauldin Smart Core Strategy. After a few glasses of wine and great conversation with Geoff and Jared Wickes, it was time for bed. I needed to get up early to figure out what to share with you this week.

Jared Wickes of Capital Advisor Network and Steve at the Dallara IndyCar Factory

I hope you find On My Radar helpful. It sure helps me to think things through and do my best to understand where we are in the cycle. Are the odds stacked in our favor, with better investment opportunities and high return probabilities, or are potential returns low? Should I be playing more offense than defense or vice versa? Investing is a game of poker. Figuring out what the major players at the table are doing matters. Debt levels, valuations, length of business cycle, length of bull market—if you are a 60-40 investor, look down at your cards, consider the odds, and think about whether you have a winning hand. I suggest patience and broadening your investment opportunity set.

I have a great weekend ahead. Stepson Kieran has his senior day prior to a big game tomorrow at noon. Penn State plays Michigan later that evening. Golf is on the schedule for Sunday with daughter Brie, my Philadelphia Union plays the Red Bulls and the Eagles play the Dallas Cowboys Sunday night. A cold IPA or two and “W’s” are on my wish list.

Wishing you a fun-filled weekend.

Warm regards,

Stephen B. Blumenthal

Executive Chairman & CIO