DRIP stands for Dividend Reinvestment Plan. When an investor is enrolled in a DRIP, it means that incoming dividend payments are used to purchase more shares of the issuing company – automatically.

Q1 hedge fund letters, conference, scoops etc

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

Many businesses offer DRIPs that require the investors to pay fees. Obviously, paying fees is a negative for investors. As a general rule, investors are better off avoiding DRIPs that charge fees.

Fortunately, many companies offer no-fee DRIPs. These allow investors to use their hard-earned dividends to build even larger positions in their favorite high-quality, dividend-paying companies – for free.

Dividend Aristocrats are the perfect complement to DRIPs. Dividend Aristocrats are elite companies that satisfy the following:

- Are in the S&P 500 Index

- Have 25+ consecutive years of dividend increases

- Meet certain minimum size & liquidity requirements

You can view a downloadable spreadsheet of all Dividend Aristocrats by clicking on the link below:

Think about the powerful combination of DRIPs and Dividend Aristocrats…

You are reinvesting dividends into a company that pays higher dividends every year. This means that every year you get more shares – and each share is paying you more dividend income than the previous year.

This makes a powerful (and cost-effective) compounding machine.

This article takes a look at the top 15 Dividend Aristocrats that offer no-fee DRIPs, ranked in order of expected total returns from lowest to highest.

We have also included a video discussing the previous edition of the top 15 no-fee DRIP stocks.

Vvv

We will have a new video update for the 2019 list soon.

The updated list for 2019 includes our top 15 Dividend Aristocrats, ranked by expected returns according to the Sure Analysis Research Database, that offer no-fee DRIPs to shareholders. You can skip to analysis of any individual Dividend Aristocrat below:

- #15: Cincinnati Financial (CINF)

- #14: Hormel Foods Corporation (HRL)

- #13: Abbott Laboratories (ABT)

- #12: Ecolab Inc. (ECL)

- #11: The Sherwin-Williams Company (SHW)

- #10: Nucor Corporation (NUE)

- #9: Aflac Inc. (AFL)

- #8: 3M Company (MMM)

- #7: Emerson Electric (EMR)

- #6: Johnson & Johnson (JNJ)

- #5: Exxon Mobil (XOM)

- #4: Federal Realty Investment Trust (FRT)

- #3: Illinois Tool Works (ITW)

- #2: A. O. Smith (AOS)

- #1: AbbVie Inc. (ABBV)

- No-Fee DRIP Dividend Aristocrat #15: Cincinnati Financial (CINF)

- No-Fee DRIP Dividend Aristocrat #14: Hormel Foods (HRL)

- No-Fee DRIP Dividend Aristocrat #13: Abbott Laboratories (ABT)

- No-Fee DRIP Dividend Aristocrat #12: Ecolab (ECL)

- No-Fee DRIP Dividend Aristocrat #11: Sherwin-Williams (SHW)

- No-Fee DRIP Dividend Aristocrat #10: Nucor (NUE)

- No-Fee DRIP Dividend Aristocrat #9: Aflac (AFL)

- No-Fee DRIP Dividend Aristocrat #8: 3M (MMM)

- No-Fee DRIP Dividend Aristocrat #7: Emerson Electric (EMR)

- No-Fee DRIP Dividend Aristocrat #6: Johnson & Johnson (JNJ)

- No-Fee DRIP Dividend Aristocrat #5: Exxon Mobil (XOM)

- No-Fee DRIP Dividend Aristocrat #4: Federal Realty Investment Trust (FRT)

- No-Fee DRIP Dividend Aristocrat #3: Illinois Tool Works (ITW)

- No-Fee DRIP Dividend Aristocrat #2: A.O. Smith (AOS)

- No-Fee DRIP Dividend Aristocrat #1: AbbVie (ABBV)

- Final Thoughts and Additional Resources

No-Fee DRIP Dividend Aristocrat #15: Cincinnati Financial (CINF)

Cincinnati Financial is an insurance company founded in 1950. It offers a wide range of insurance products including life, business, home & auto, and property & casualty insurance, as well as financial products including annuities.

Source: Investor Presentation

The company is highly profitable. As an insurance company, Cincinnati Financial makes money in two ways. It earns income from premiums on policies written, and also by investing its float, or the large sum of premium income not paid out in claims.

In early February (2/6/19) Cincinnati Financial reported fourth-quarter and full-year financial results. Total revenue declined roughly 50% in GAAP terms, but this was due entirely to a recent change in FASB accounting standards related to securities investments.

The core metrics for Cincinnati Financial continue to look strong. For example, earned premiums increased 5%, while investment income rose 3% for the fourth quarter. Adjusted earnings-per-share of $0.98 increased 5% for the period.

For the full-year, adjusted earnings-per-share increased 22% to $3.35. Higher premium income, higher investment income, share repurchases, and tax reform contributed to Cincinnati Financial’s strong performance last year.

Cincinnati Financial’s strong business model has led to steady growth over many years, and there should be room for continued growth up ahead.

Growth should continue to come from new policies written. The company has a successful history of growing profits through increased policies written.

Price increases helped the company grow revenue from premiums over the past year. Rising interest rates will also give the company a boost. Interest rates have risen over the past year, which will help Cincinnati Financial earn higher income from its investment portfolio.

The one downside to Cincinnati Financial is that the stock appears to be overvalued. With a 2019 price-to-earnings ratio above 25, the stock is valued at a significant premium to other insurance stocks in the same peer group.

Cincinnati Financial’s expected earnings growth rate of 5% and its nearly 3% dividend yield will help support shareholder returns. But the significant overvaluation could reduce annual returns to the low-single digits.

Cincinnati Financial is a dividend growth company, but investors should wait for a better price before buying the stock.

No-Fee DRIP Dividend Aristocrat #14: Hormel Foods (HRL)

Hormel’s history dates all the way back to 1891. The company has continued to grow in the 100+ years since, and now generates more than $10 billion in annual revenue.

Today, it has a diverse portfolio of food brands. Some of its major brands include Skippy, Jennie-O, Spam, Hormel, and Dinty Moore.

In recent years, it has added more natural products to compliment its processed offerings, such as Justin’s and Applegate.

Source: Investor Presentation

This is a challenging time for Hormel, because the company’s large Jennie-O turkey segment is under pressure from falling prices, due to record production of turkeys in the U.S.

After a very weak 2017 and 2018, Jennie-O saw its revenue, volume and segment profit all flat year-over-year in the company’s Q1 earnings report, which was released on 2/21/19.

While total volume and sales were flat, improved results in foodservice and commodity sales were offset by declines in retail.

Fortunately, the good news is that other categories have helped offset weak performance in turkey products. The refrigerated foods segment grew volume by 1%, and segment profits rose 3% during Q1.

Sales growth was led by the company’s Hormel Deli Solutions business, as well as strength from other deli meat and retail brands.

The grocery products segment generated 3% volume growth, while operating profit fell 2%.

Despite the recent issues, Hormel’s long-term growth potential remains intact. Management reiterated guidance for fiscal 2019 after the first-quarter report. The reaffirmed range of $1.77 to $1.91 in earnings-per-share results in $1.84 per share at the midpoint of guidance.

Hormel also announced on 2/19/19 it was selling the CytoSport business to PepsiCo for $465 million. The deal will cause Hormel to cede $300 million in annual revenue, but Hormel can use the proceeds to buy back stock, acquire future growth or pay down debt.

Hormel has an extremely impressive history of generating consistent growth from year to year.

Source: Investor Presentation

We expect Hormel to generate earnings growth of 5% per year over the next five years, driven by sales growth.

The stock is currently valued at 23.4 times this year’s average earnings-per-share estimate. With a fair value estimate at 18 times earnings, the stock is slightly overvalued.

A declining price-to-earnings ratio could negatively impact total returns by 5% per year through 2024. Still, earnings growth of 5% annually will offset the negative returns from overvaluation. The current dividend yield of 2% will likely represent the vast majority of total returns over the next five years.

No-Fee DRIP Dividend Aristocrat #13: Abbott Laboratories (ABT)

Abbott Laboratories is a diversified healthcare corporation with a market capitalization of $140 billion. The company was founded in 1888 and is headquartered in Lake Bluff, Illinois.

The company operates four main segments:

- Nutritional Products

- Branded Generic Pharmaceuticals

- Diagnostics

- Medical Devices

The company’s Nutrition Products segment is characterized by market leadership. It is the #1 pediatric nutrition provider in the United States and some other geographies. Moreover, the segment’s performance has improved considerably in recent years as operating margin has improved in each and every year since 2011.

The company’s Branded Generic Pharmaceuticals segment is focused on emerging markets, with an emphasis on BRIC countries (Brazil, Russia, India, and China).

The company’s Diagnostics segment is geographically more diverse than the Branded Generic Pharmaceuticals segment. Similar to the Nutrition segment, the Diagnostics segment has seen significant operating margin improvements over the last several years.

Abbott Laboratories’ last segment is the Medical Devices unit. This segment was significantly bolstered in recent times by the St. Jude Medical acquisition.

The company’s high-quality product portfolio and the acquisition of St. Jude should fuel strong growth for the next several years. Abbott Laboratories has two major growth prospects that will help its business to become increasingly more profitable over the years to come.

The first is the aging population, both domestically and within the United States. In 2017, the percent of the global population that exceeded age 65 was 8.7%. This proportion is expected to reach 16.7% in 2050.

Source: Investor Presentation

The second broad tailwind that will benefit Abbott Laboratories is the company’s focus on the emerging markets. This is particularly true for its Branded Generic Pharmaceuticals segment.

Many of the countries that this segment is focused on spend a very small proportion of their overall GDP on healthcare, a rate that is expected to increase in the future.

The aging domestic population combined with the rather low focus on healthcare spending in emerging market countries should leave Abbott Laboratories plenty of room to grow for the foreseeable future.

Abbott Laboratories’ competitive advantage is two-fold. The first component is its remarkable brand recognition among its consumer medical products, particularly in its Nutrition segment.

Led by noteworthy products like the Ensure meal replacement supplement, Abbott Laboratories brands allow its sales to stand strong through even the worst economic recessions.

Another appealing quality of Abbott’s diversification is that it is an extraordinarily recession-resistant company. It actually managed to increase its adjusted earnings-per-share during each year of the 2007-2009 financial crisis.

- 2007 earnings-per-share of $2.84

- 2008 earnings-per-share of $3.03

- 2009 earnings-per-share of $3.72

- 2010 earnings-per-share of $4.17

Abbott Laboratories remarkably managed to grow its earnings-per-share each year during one of the most economically difficult time periods on record.

Abbott Laboratories stock trades for a price-to-earnings ratio of 24.9, based on earnings-per-share estimates of $3.20 for 2019. Fair value is estimated to be a price-to-earnings ratio of 19, which is significantly below the current valuation.

Abbott shares appear to be overvalued. If shares revert to our fair value estimate of 19, this would reduce total returns by 5.3% per year. While right now may not be the best time to purchase shares of this high-quality business, total return may still be satisfactory, particularly when adjusted for the low-risk nature of Abbott’s business model.

The other major component of Abbott Laboratories’ future total returns will be the company’s earnings-per-share growth. Investors can reasonably expect 6.5% in annual adjusted earnings-per-share growth moving forward.

And Abbott has a 1.6% dividend yield, leading to total expected returns of nearly 3% per year.

No-Fee DRIP Dividend Aristocrat #12: Ecolab (ECL)

Ecolab was created in 1923, when its founder Merritt J. Osborn invented a new cleaning product called “Absorbit”. This product cleaned carpets without the need for businesses to shut down operations to conduct carpet cleaning.

Osborn created a company revolving around the product, called Economics Laboratory, or Ecolab. Today, Ecolab is the industry leader and generates annual sales in excess of $14 billion.

Ecolab operates three major business segments: Global Industrial, Global Institutional, and Global Energy, each of roughly equal size. The business is diversified in terms of operating segments, and also geography. Over 40% of the company’s sales took place outside North America last year.

Source: Investor Presentation, page 4

The Global Industrial group provides water treatment, cleaning, and sanitation. Customers in this segment are primarily large firms in the food and beverage, manufacturing, chemical, and mining industries.

The Global Institutional business provides specialized cleaning and sanitation services, such as on-premise laundry, housekeeping, and food safety. Customers are primarily in the foodservice, hospitality, lodging, healthcare, and retail industries.

Lastly, the Global Energy segment includes the Nalco brand. Nalco provides chemical and water treatment services to the petroleum and petrochemical industries, specifically to oilfield services and refineries.

Ecolab has many positive growth catalysts. One of the company’s most important growth catalysts is acquisitions.

In 2017, Ecolab announced the acquisition of Georgia Pacific’s paper chemicals business. The purchase will help boost Ecolab’s growing paper business, which helps paper manufactures improve their efficiency, product quality, and profitability.

More recently, Ecolab announced that it would be purchasing U.K. based Holchem Group Limited for US$56 million. Holchem Group Limited is a supplier of hygiene and cleaning products and services for the foodservice and hospitality industries.

Acquisitions such as these, along with organic investment, have fueled steady earnings growth for decades.

In mid-February, Ecolab reported (2/19/19) financial results for the fourth quarter of fiscal 2018. In the quarter, the company grew its reported sales by 3% and its currency-adjusted sales by 6%.

Its adjusted earnings-per-share rose 12% thanks to price hikes, cost savings and a lower tax rate, which more than offset the increased delivered product costs and unfavorable currency effects.

For the year, Ecolab remained in its solid growth trajectory, with 6% revenue growth and 12% adjusted earnings-per-share growth. Management stated that the company has entered this year with strong sales momentum, good pricing and attractive growth opportunities.

The company provided upbeat guidance for this year. More precisely, it expects adjusted earnings-per-share of $5.80-$6.00, implying 12% growth at the mid-point.

Ecolab stock has a current dividend yield of just 1%, which makes the stock fairly unattractive for income investors. However, it makes up for this with high dividend growth. In December 2018, the company raised its dividend by 12%.

Earnings-per-share are expected to grow by 9% per year over the next five years. The stock trades for almost 31x this year’s earnings estimate, meaning Ecolab is significantly overvalued.

Total returns are estimated to be in the ~3% range over the next five years, due largely to the impact of overvaluation.

No-Fee DRIP Dividend Aristocrat #11: Sherwin-Williams (SHW)

Sherwin-Williams is the world’s second-largest manufacturer of paints and coatings. The company distributes its products through wholesalers as well as retail stores. Sherwin-Williams was founded in 1866, and has grown to be a market leader with annual sales of $15 billion.

The company distributes its products through wholesalers as well as retail stores that bear the Sherwin-Williams name. Its only competitor of comparable size is fellow Dividend Aristocrat PPG Industries.

Investor Presentation, page 3

Sherwin-Williams is certainly a market leader. The company has become significantly larger since its relatively recent acquisition of Valspar.

The Valspar merger was transformative for Sherwin-Williams. Post-merger, Sherwin-Williams is now divided into three segments: Americas, Consumer Brands, and Performance Coatings.

Sherwin-Williams reported its fourth quarter and full year earnings results on January 31. The company generated revenue of $4.06 billion during the fourth quarter, which represents a revenue growth rate of 2.0% versus the prior year’s quarter.

Sherwin-Williams grew its same-store sales by 5.1% during fiscal 2018, which was a very strong performance. Sherwin-Williams earned $3.54 on a per-share basis during the fourth quarter, up 12% from the same quarter last year.

Looking ahead, Sherwin-Williams stands to benefit from international growth. Demand for Sherwin-Williams’ products is expected to grow most rapidly in the Asia-Pacific region.

In addition, the company has scale unlike any of its competitors in Latin America and North America. The Valspar acquisition helped to accelerate expansion into Asia-Pacific.

These factors should boost revenue growth in the near-term. Sherwin-Williams expects sales growth of 4%-6% per year through the end of fiscal 2020.

Sherwin-Williams has an impressive growth profile. Earnings-per-share are expected to grow by 9% per year over the next five years.

In addition, the stock has a dividend yield of 1%. However, with a price-to-earnings ratio of 21, shares appear to be fairly valued.

As a result, earnings growth and dividends will represent the vast majority of future shareholder returns. Still, the stock could be a rewarding investment with projected annual returns of 9% per year.

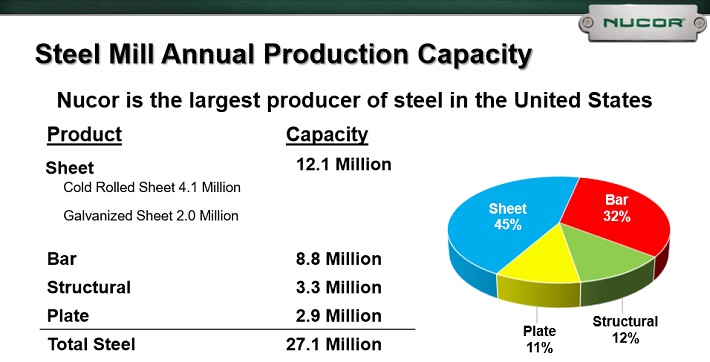

No-Fee DRIP Dividend Aristocrat #10: Nucor (NUE)

Nucor is the largest publicly traded U.S.-based steel corporation based on its market cap of $18.5 billion.

The steel industry is notoriously cyclical which makes Nucor’s streak of 46 consecutive years of dividend increases more remarkable. Nucor is a member of the Dividend Aristocrats Index due to its dividend history.

The company currently operates in three segments: Steel Mills (the largest segment by revenue), Steel Products, and Raw Materials.

Source: Investor Presentation

Nucor manufactures a wide variety of material types, including sheet steel, steel bars, structural formations, steel plates, downstream products, and raw materials. The majority of the company’s production comes from a combination of sheet and bar steel, as has been the case for many years.

Nucor faces challenges from international competitors. Some countries (including China) subsidize their steel industry, making steel exported to the United States artificially cheap.

President Trump signed a bill in March of 2018 placing a 25% tariff on imported steel for all countries except Canada and Mexico. This was certainly positive news for Nucor, as reflected in the company’s recent earnings reports.

On 1/29/19 Nucor reported fourth quarter and full-year 2018 earnings. Revenue of $6.3 billion rose 24% year-over-year, and was in-line with analyst estimates. Earnings-per-share of $2.07 beat analyst expectations by $0.14 per share, and increased 73% for the quarter.

Sales growth was due to a combination of higher volumes and significantly higher prices compared with the same quarter in 2017. Earnings growth also benefited from tax reform. Full-year EPS hit a record $7.42, compared with EPS of $4.10 for 2017.

Nucor is firing on all cylinders right now. But investors should be aware of the impact a global recession would have on the company. Nucor’s previous all time EPS high came in 2008 which coincided with the all-time high price of steel in the United States.

But the Great Recession wiped out Nucor’s profitability, and the company reported a net loss in 2009.

Absent a global recession, Nucor has a positive growth outlook. The company expects 2019 to be one of the best years in its history. We are only willing to estimate 3% annual earnings growth through 2024, given the historical earnings volatility of the company.

In addition to 3% expected earnings growth, Nucor pays a dividend which currently yields 2.6%. The stock appears to be modestly overvalued using historical dividend yield, as Nucor’s earnings volatility makes a price-to-earnings ratio a less valuable metric.

Nucor’s average dividend yield of 3.2% over the past 10 years is higher than its current yield. If the stock price declined to push up the dividend yield, annual returns would be reduced by 2%-3% each year.

Overall, Nucor has total expected returns in the low-single digit range over the next five years.

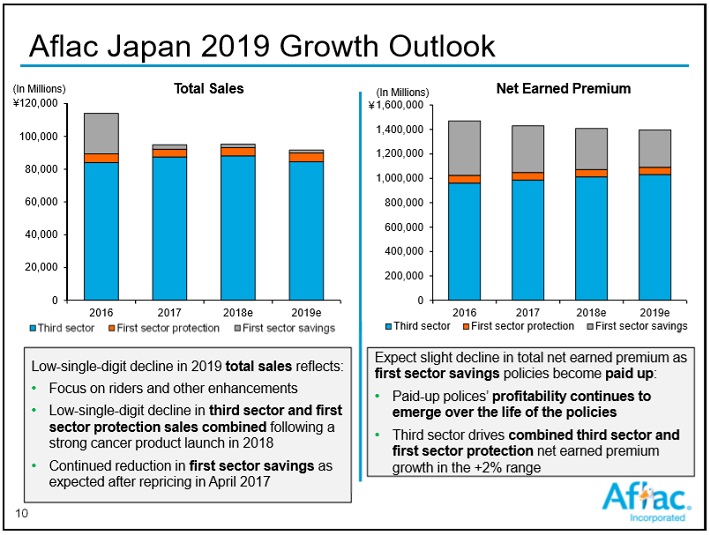

No-Fee DRIP Dividend Aristocrat #9: Aflac (AFL)

Aflac is the global leader in the supplemental health insurance industry. The company has humble roots in Columbus (Aflac stands for American Family Life Assurance Company of Columbus), where the company was founded by the Amos brothers (John, Paul, & Bill) in 1955.

In the 60+ years since, the company has grown at a rapid rate. Aflac generates annual revenue of nearly $22 billion, and is the world’s largest underwriter of supplemental cancer insurance. The company also provides accident, short-term disability, critical illness, dental, vision, and life insurance.

Roughly 70% of the company’s pretax earnings are derived from Japan, with the remaining 30% coming from the United States.

On January 31st, 2019 Aflac released fourth-quarter and full year 2019 financial results. For the quarter the company reported $5.13 billion in revenue, down 5.5% from $5.42 billion in the 2017 fourth quarter. Adjusted earnings-per-share totaled $1.02, up 27.5% from $0.80 year-over-year.

For the full year Aflac reported $21.76 billion in revenue, a 0.4% increase as compared to 2017. Aflac also reported $4.16 in adjusted earnings-per-share, a 22.4% increase compared to $3.40 in 2017. Earnings growth was driven by a lower tax rate, strong investment income and favorable benefit ratios.

For 2019, Aflac expects $4.10 to $4.30 in adjusted earnings-per-share.

With such significant operations in Japan, the company is heavily impacted by foreign exchange rate fluctuations. The recent strength of the U.S. dollar versus a variety of global currencies has been a headwind for this stock.

Fortunately, Aflac’s operations are highly profitable, with considerable growth potential.

In the company’s core market, Japan, Aflac is expanding its offerings of “third-sector” products. These include non-traditional products such as cancer insurance, as well as medical and income support.

Growth in these products is expected to continue, although Aflac expects overall sales in Japan to decline slightly in 2019.

Source: Investor Presentation

Aflac has enjoyed strong demand in Japan for third-sector products, due to the country’s aging population, and declining birthrate. Moving forward, Aflac expects 4%-6% annual growth in third-sector product sales in Japan.

Overall, investors can reasonably expect Aflac to grow earnings-per-share by 6% annually over the next five years.

Over the last decade shares of Aflac have traded hands with an average P/E ratio of roughly 10 times earnings. We believe this is more or less fair for the security, considering that many insurers trade at a comparable multiple.

With a price-to-earnings ratio of 11 based on expected 2019 earnings, the valuation could contract to fair value. This would reduce annual returns by just over 2% per year.

Fortunately, Aflac’s 2.2% dividend yield will offset this. Total expected returns are in the range of future earnings growth, estimated to be roughly 6% per year.

No-Fee DRIP Dividend Aristocrat #8: 3M (MMM)

3M has a very impressive track record. It has paid dividends for over 100 years, and it has raised its dividend for 60 years in a row.

This makes 3M a Dividend King, an even smaller group of companies with 50+ consecutive years of dividend increases. There are fewer than 25 Dividend Kings, including 3M.

3M sells more than 60,000 products that are used every day in homes, hospitals, office buildings and schools around the world. 3M has more than 90,000 employees and serves customers in more than 200 countries.

3M is composed of five separate divisions: Industrial; Safety & Graphics; Healthcare; Electronics & Energy; and Consumer products.

3M released financial results for the fourth quarter and full year 2018 on January 29th. The company’s adjusted earnings-per-share (EPS) were $2.31 for the quarter, up 10% from the previous year.

Revenue declined 0.5% to $8 billion, but currency was a headwind. 3M had solid organic local-currency growth of 3%.

In 2018, organic revenue increased 3.2% for the year while earnings-per-share increased 14%, thanks to organic growth, a lower tax rate and share repurchases.

2019 is likely to be another year of growth for the company. 3M expects earnings-per-share in a range of $10.45-$10.90. At the midpoint, this would represent 2.1% growth from the prior year.

3M maintains a highly promising outlook over the next few years. The company expects to generate returns on invested capital above 20% each year through 2023, thanks in large part to a lean cost structure.

Source: Investor Presentation

It also aims for 3%-5% organic revenue growth in constant currency, along with 8%-11% annual earnings-per-share growth.

3M’s portfolio optimization, characterized by various acquisitions and divestitures, has made the company leaner and more efficient.

The company also repurchased almost $5 billion worth of its own stock in 2018 and expects to buy back another $2 to $4 billion in 2019.

To raise dividends for over 50 years, requires multiple durable competitive advantages. For 3M, technology and intellectual property are its biggest competitive advantages.

3M has 46 technology platforms and a team of scientists dedicated to fueling innovation. Innovation has provided 3M with over 100,000 patents obtained throughout its history, which helps fend off competitive threats.

The problem for 3M is that the stock is slightly overvalued today. For example, 3M expects full-year earnings-per-share of $10.68, at the midpoint of 2019 guidance.

At its current share price, the stock is trading at a forward price-to-earnings ratio of 20. This is higher than its average valuation. 3M has held an average price-to-earnings ratio of 17.2 over the past 10 years.

This makes 3M stock slightly overvalued. Shareholders would see total annual returns reduced by 3.0% per year if the stock reverted to its average valuation by 2024.

3M has experienced earnings-per-share growth of 6.4% over the last decade, a good baseline for future growth. A combination of organic growth and share repurchases should allow the company to see this level of growth in future years.

A breakdown of expected returns through 2024 is as follows:

- 6.4% organic EPS growth

- 3.0% multiple reversion

- 2.7% dividend yield

Through earnings growth and dividends, partially offset by a declining valuation multiple, we estimate that 3M can generate a total annual return of 6.1% through 2024.

No-Fee DRIP Dividend Aristocrat #7: Emerson Electric (EMR)

Emerson Electric is an ideal candidate for a no-fee DRIP program, as the company has increased its dividend for over 60 years in a row.

Emerson Electric was founded in Missouri in 1890 and since that time, it has evolved to become an industrial giant with $19 billion in annual revenue.

Emerson is organized into two major reporting segments called Automation Solutions and Commercial & Residential Solutions.

Source: Investor Presentation

Automation Solutions helps manufacturers minimize energy usage, waste, and other costs in their processes. The Commercial & Residential Solutions segment makes products that protect food quality and safety, as well as boost efficiency in the production process.

Emerson recently announced strong fiscal 2019 first-quarter results.

Total sales were up 9% during the quarter as organic growth accounted for 4.5%, while acquisitions added 6%, but was partially offset by a 1.5% loss thanks to currency translation. Sales strength came from broad demand in its global industrial markets, professional tools markets, as well as North American air conditioning markets.

Earnings-per-share rose 21% to $0.74 in total. Emerson repurchased $800 million worth of stock in the first quarter, which helped management boost its forecasts for 2019.

Net sales growth is now expected to be 7% to 10% with the bulk of it coming from underlying sales growth and the balance from acquisitions. Earnings-per-share are now expected in a range of $3.60 to $3.75; we’ve updated our estimate accordingly to $3.68 per share.

Emerson continues to acquire and divest companies in its portfolio to optimize the amount of revenue risk it is taking and focus on longer-term growth opportunities. Recently, Emerson has acquired Advanced Engineering Valves, a manufacturer of innovative valve technology that helps LNG customers operate more efficiently.

In addition, it has acquired the intelligence platforms business from General Electric, affording it the ability to expand its capabilities in machine learning and discrete applications. Acquisitions and divestitures are a way of life for Emerson and the ever-shifting mix of business has been beneficial in recent years.

Emerson is expected to generate earnings growth of 5% per year. The stock appears to be fairly valued at the moment. Adding in the 2.8% dividend yield, total returns could exceed 7% per year.

No-Fee DRIP Dividend Aristocrat #6: Johnson & Johnson (JNJ)

There are few dividend growth stocks that can match Johnson & Johnson’s tremendous track record. J&J is another Dividend King, with over 50 consecutive years of dividend growth.

J&J is a global healthcare giant. It has a market capitalization of $365 billion, and generates annual revenue of more than $81 billion. It is a massive company, with more than 250 subsidiary companies.

In all, it manufactures and sells health care products through three main segments:

- Pharmaceuticals (50% of sales)

- Medical Devices (33% of sales)

- Consumer Health Products (17% of sales)

It has a diversified business model, with strong brands across its three core operating segments.

Source: Earnings Presentation

J&J is one of the largest companies in the world. Its pharmaceutical segment is its strongest area of growth. This segment has recently generated much higher growth rates than medical devices or consumer products.

For example, J&J had adjusted earnings-per-share of $8.18 in 2018, which represented 12.1% growth from the previous year. Organic revenue increased 5.5% for 2018.

The pharmaceutical segment led the way, growing revenue 12.4% for the year. Revenue for medical devices and consumer products grew by just 1.5% and 1.8%, respectively.

Source: Earnings Presentation

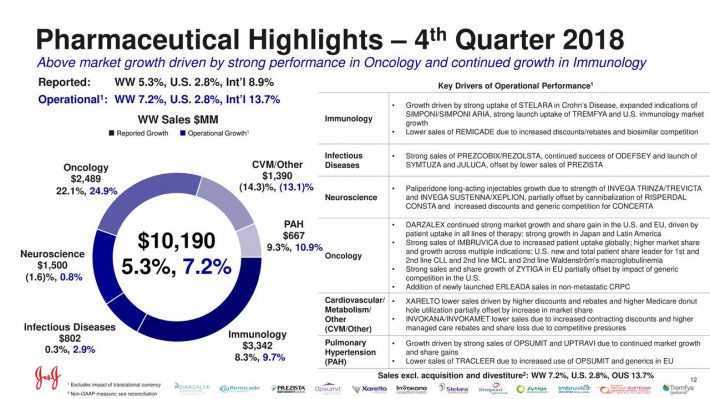

Within the pharmaceutical segment, two of the company’s best-performing areas continue to be oncology and immunology. Oncology sales rose by nearly 25% in constant currency last year, while the immunology segment grew by 9.7% in 2018.

In oncology, Darzalek experienced revenue growth of 63% on a year-over-year basis. Darzalek treats multiple myeloma. International sales more than doubled for this drug during 2018.

Imbruvica, which treats certain types of lymphoma, grew revenues by more than 38%. J&J shares Imbruvica royalties with fellow Dividend Aristocrat AbbVie.

Stelara, which treats immune-mediated inflammatory diseases, had worldwide revenue growth of 29% during the year. Revenues for Simponia / Simpona Aria, which treats rheumatoid arthritis, increased 13.7% in 2018, with 17.5% growth in international markets.

J&J’s pharmaceutical pipeline is a positive growth catalyst. The company has a robust pipeline of new products.

Source: Earnings Presentation

By 2021, J&J expects to file at least 10 new products, each with annual sales potential of $1 billion or more.

It also sees the potential for 40 line extensions to existing products by then. Of these 40 extensions, 10 have potential for more than $500 million in annual revenue.

J&J’s most important competitive advantage is innovation, which has fueled its historical growth.

J&J’s strong cash flow allows it to spend heavily on research and development. R&D is critical for a health care company, because it provides product innovation. J&J’s R&D spending exceeds $10 billion per year.

The company is expected to grow earnings by 6% per year through 2024. The stock appears to be fairly valued, meaning earnings growth and the 2.6% dividend yield are likely to make up nearly all of J&J’s expected returns over the next five years.

No-Fee DRIP Dividend Aristocrat #5: Exxon Mobil (XOM)

Exxon Mobil is the largest publicly-traded energy company in the world. It is an integrated energy giant, with large business segments across the upstream, downstream, and chemicals segments.

Exxon Mobil is an energy giant with a market capitalization of ~$340 billion. The company currently generates $290 billion in revenue with net profits of over $21 billion on an annual basis.

Not only is the business massive, it is also diversified. In 2018, the oil major generated 60% of its earnings from its upstream segment, 26% from its downstream (mostly refining) segment and the remaining 14% from its chemicals segment.

Exxon Mobil has seen its profitability expand significantly since the oil and gas downturn of 2014-2016. Last year was another year of recovery. In the 2018 fourth quarter Exxon reported $71.9 billion in revenue, up 8.1% as compared to Q4 2017.

On an adjusted basis, Exxon earned $6.41 billion in Q4 2018 against $3.73 billion in Q4 2017. For the year, the company recorded revenue of $290.2 billion, an 18.8% increase compared to 2017.

On an adjusted basis full year earnings totaled $21.04 billion compared to $15.29 billion in 2017.

Source: Investor Presentation

Upstream earnings totaled $14.25 billion ($7.74 billion in 2017), downstream earnings equaled $6.05 billion ($5.0 billion in 2017) and the chemical segment earned $3.36 billion ($4.18 billion in 2017). Earnings-per-share came in at $4.88 for the year.

Going forward, future earnings growth would be accelerated with higher oil and gas prices. But growth will also come organically from the company’s long list of new projects. The Permian Basin is one of the strongest oil fields in the U.S., and is an area of high investment for Exxon Mobil.

Exxon Mobil has a massive project pipeline, consisting of more than 100 new projects. In addition to the Permian Basin, Exxon Mobil has significant international projects located in offshore Guyana, and Angola.

Exxon Mobil is expected to generate earnings-per-share of $5.25 in 2019. Based on this, the stock is currently valued at 15.4 times earnings. Fair value is estimated to be a price-to-earnings ratio of 13.

A declining valuation multiple could decrease annual returns by 3.3% per year over the next five years, but expected earnings growth of 8% per year will offset the impact.

In addition, Exxon Mobil’s 4.1% dividend yield should result in annual returns in the high-single digits over the next five years.

No-Fee DRIP Dividend Aristocrat #4: Federal Realty Investment Trust (FRT)

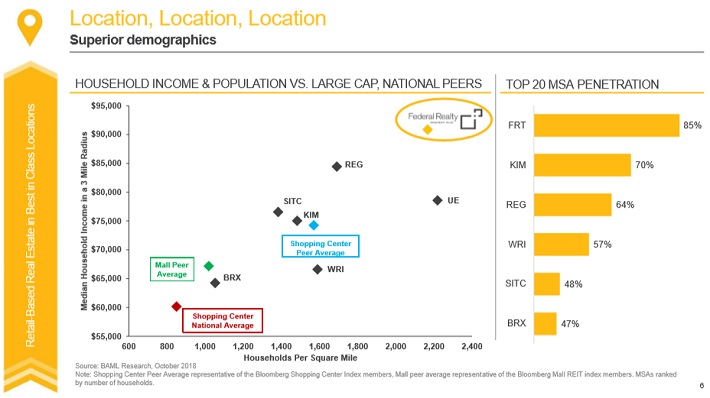

Federal Realty is one of the larger real estate investment trusts (REITs) in the United States. The trust was founded in 1962 and concentrates in high-income, densely-populated coastal markets in the U.S., allowing it to charge more per square foot than its competition.

Federal Realty uses a significant portion of its rental income, as well as external financing, to acquire new properties. This helps create a “snow-ball” effect of rising income over time.

Federal Realty primarily owns shopping centers. However, it also operates in redevelopment of multi-purpose properties including retail, apartments, and condominiums.

The portfolio is highly diversified in terms of tenant base. No individual industry represents more than 9% of the portfolio, and no single tenant accounts for more than 3%. Federal Realty has a high-quality tenant portfolio.

Source: Investor Presentation, page 6

Federal Realty’s retail portfolio is second to none in the industry in terms of average base rent, and consists of over 100 properties.

Federal Realty reported strong results for the 2018 fourth-quarter and full year. Fourth quarter comparable property net operating income rose 2%. Thanks to new properties and other revenue, the trust’s total revenue grew 5.1% for the fourth quarter.

Funds from operation, or FFO, rose 21% thanks the trust’s strong revenue gain and lower operating expenses. For the full-year, FFO rose 8.5% to $6.23.

Federal Realty offered up guidance for 2019 of $6.30 to $6.46 in FFO-per-share. Federal Realty’s growth will be comprised of a continuation of higher rent rates on new leases and its impressive development pipeline fueling asset base expansion.

Federal Realty’s competitive advantages include its superior development pipeline, its focus on high-income, high-density areas, and its decades of experience in running a world-class REIT. These qualities allow it to perform admirably and even grow through recessions, when many lower-quality REITs struggle.

We are forecasting total annual returns of 9% going forward comprised of 5.5% funds-from-operations growth, the current 3% yield and a modest valuation tailwind of 0.5%.

Federal Realty is a unique stock, in the sense that it is the only REIT on the list of Dividend Aristocrat. This makes it an appealing stock for investors interested in a no-fee DRIP and exposure to the real estate industry.

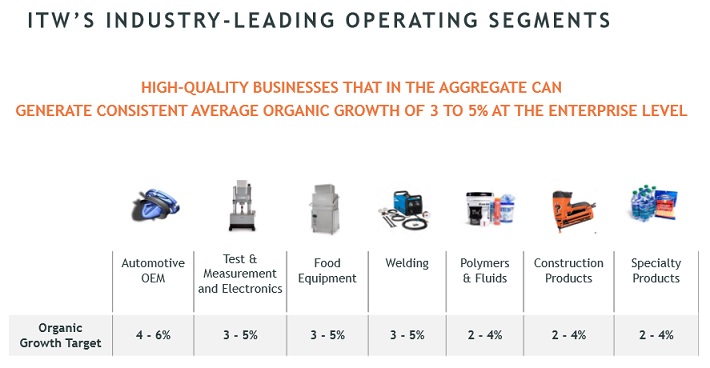

No-Fee DRIP Dividend Aristocrat #3: Illinois Tool Works (ITW)

Illinois Tool Works started out all the way back in 1902. Today, Illinois Tool Works has a market capitalization of $46 billion, and generates annual revenue of more than $14 billion.

Illinois Tool Works is a diversified industrial manufacturer, with a large product portfolio that includes exposure to multiple growth categories.

Source: Investor Day Presentation

Illinois Tool Works’ portfolio is concentrated in product segments that each hold growth potential of 2%+ above the average in their respective markets.

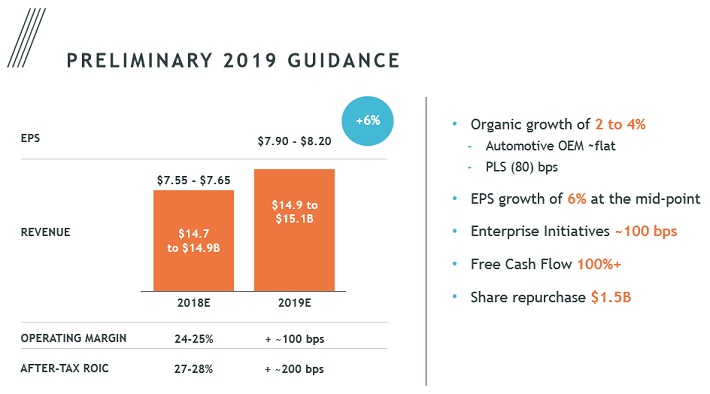

Illinois Tool Works reported its fourth quarter and full year earnings results on February 1st. For the fourth quarter, the company generated revenue of $3.58 billion, which was 1.4% less than the company’s revenues during the previous year’s quarter.

Despite the revenue decline, the company still grew earnings-per-share by 15% compared to the prior year’s quarter. This was due to margin expansion, a lower tax rate, and the positive impact of share buybacks.

Adjusted earnings-per-share increased 10% for the fourth quarter, and 15% for 2018. The upcoming year is expected to be another good one for the company.

Source: Investor Day Presentation

Illinois Tool Works guides for earnings-per-share in a range of $7.90 to $8.20 during fiscal 2019, a projected increase of 6% at the midpoint of guidance.

Illinois Tool Works stock trades for a price-to-earnings ratio of 18.7, using the midpoint of 2019 earnings guidance. This is slightly above our fair value estimate of 17, meaning a contracting price-to-earnings ratio could reduce shareholder returns by 1.9% per year.

That said, expected five-year earnings growth of 8% per year, combined with the 2.7% dividend yield, result in total expected returns of 9% per year. This makes Illinois Tool Works a quality long-term holding for dividend growth investors.

No-Fee DRIP Dividend Aristocrat #2: A.O. Smith (AOS)

A.O. Smith is a global leader applying energy-efficient products and solutions. It manufactures a variety of residential and commercial water heaters, as well as water treatment and air purification products.

A.O. Smith has performed very well over the past decade, thanks largely to the steady global economic recovery coming out of the Great Recession of 2007-2009. The company’s sales have grown at a double-digit annual rate, on average, in the past 10 years.

In the same 10-year period, adjusted earnings-per-share increased 25% per year.

A.O. Smith has continued its growth in recent periods. On January 29th, A.O. Smith released fourth-quarter earnings, which were very strong.

The company generated earnings-per-share of $0.74, which topped estimates and were an improvement of 23.3% from the previous year. Quarterly revenue grew 5.7% to $812.5 million.

For the full year, revenue increased 6.4% to $3.2 billion, while adjusted earnings-per-share increased 19%, to $2.61.

A.O. Smith’s growth catalysts in the U.S. include continued economic growth and increasing housing prices.

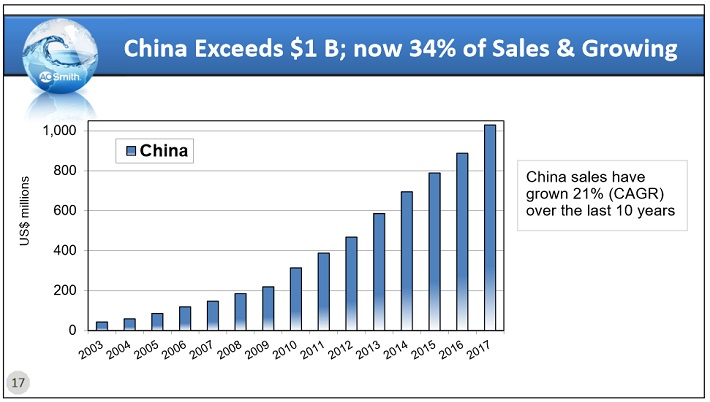

Outside the U.S., the company’s main growth prospects are in China, where it already has a large operation. China is arguably the most attractive economy in the world. Not only does it have a population of 1 billion, and a growing middle class, but the country has been growing its economy at a high rate.

Source: Investor Presentation

China represents a major long-term opportunity for A.O. Smith. China now contributes over $1 billion in annual sales for the company, representing over 30% of total sales.

And, sales in China have grown at a high rate. Sales in China rose more 20% each year in the ten year-period through 2017.

There are reasons to be optimistic about A.O. Smith’s China business. Besides China’s large population, the air quality in the country is quite poor. This has caused demand for A.O. Smith’s air purifiers to be quite strong.

We expect A.O. Smith to grow earnings-per-share at a rate of 9% per year through 2024, which is half of the company’s growth rate over the last decade. The stock currently trades for a price-to-earnings ratio of 20, exactly equal to our fair value estimate.

Future returns will be comprised mainly of earnings growth and dividends. With expected EPS growth of 9% per year and a current dividend yield of 1.6%, A.O. Smith could generate total returns in the low-double digits through 2024.

No-Fee DRIP Dividend Aristocrat #1: AbbVie (ABBV)

Taking the top spot on the list of no-fee DRIP Dividend Aristocrats is AbbVie. This is because AbbVie has the most attractive mix of expected earnings growth, a low stock valuation, and a high dividend yield above 5%.

AbbVie is a pharmaceutical company focused on three core therapeutic areas: Immunology, Oncology, and Virology. AbbVie was spun off by Abbott Laboratories in 2013.

Currently, AbbVie generates annual sales in excess of $30 billion. AbbVie stock has a market capitalization of approximately $123 billion.

AbbVie was spun off from Abbott so that it could grow on its own as a pharmaceutical pure-play, with its own dedicated management team.

This was clearly the right decision, as AbbVie has grown at an impressive rate since the spin-off.

Source: Investor Presentation

In late January (1/25/19) AbbVie reported its fourth-quarter and full-year earnings results. Revenue of $8.3 billion for the fourth quarter increased 7%, due primarily to 42% growth for Imbruvica.

Humira, AbbVie’s most important drug by far, grew sales just 0.5%.

AbbVie earned $1.90 per share during the fourth quarter, which was 28% more than the company’s earnings-per-share during the fourth quarter of the previous year.

For 2018, AbbVie generated earnings-per-share of $7.91, up 41% from 2017. AbbVie management expects adjusted earnings-per-share in a range of $8.65 to $8.75 for 2019.

AbbVie’s challenge is to prepare for biosimilar competition for its flagship product Humira, the world’s top selling drug.

Price discounting in Europe has already weighed on AbbVie. Humira sales in Europe fell by 15% last quarter. Biosimilar competition is expected in the U.S. in 2023.

Fortunately, AbbVie has adequately invested in research and development to build a strong pipeline of new products. AbbVie spent more than $10 billion on R&D investments last year.

Two of its most compelling areas of future growth are hematologic oncology, and next-generation immunology.

Source: Investor Presentation

AbbVie expects non-Humira product sales to exceed $16 billion by 2020, and more than $35 billion by 2025.

Based on expected earnings-per-share of $8.70, AbbVie stock trades for a price-to-earnings ratio of 9.5. Our fair value estimate for AbbVie is a price-to-earnings ratio of 13.0, indicating the stock is significantly undervalued.

An expanding valuation multiple could boost shareholder returns by approximately 6.5% per year over the next five years. In addition, we expect annual earnings growth of 9%-10% through 2024.

Lastly, the stock has a current dividend yield of 5.2%. In total, we expect annual returns exceeding 20% per year over the next five years for AbbVie.

Final Thoughts and Additional Resources

Enrolling in DRIPs can be a great way to compound your portfolio income over time. That being said, I prefer to selectively reinvest my dividends into my current best investment idea. This ensures that DRIPs don’t automatically purchase stocks that I view as overvalued.

Additional resources are listed below for investors interested in further research for DRIP plans.

For dividend growth investors interested in DRIPs, the 15 companies mentioned in this article are a great place to start. Each business is very shareholder friendly, as evidenced by their long dividend histories and their willingness to offer investors no-fee DRIP plans.

Thanks for reading this article. Please send any feedback, corrections, or questions to support@suredividend.com.

Article by Bob Ciura, Sure Dividend

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.