A lot of focus, talk, and frankly noise has emanated around a widely expected Fed rate cut at the end of this month. But the discerning observer will note that the Powell Pivot is actually part of a wider global monetary policy pivot. This has been a key theme for us and, in our view, is a key reason to remain bullish on risk assets and the global growth outlook.

Q2 hedge fund letters, conference, scoops etc

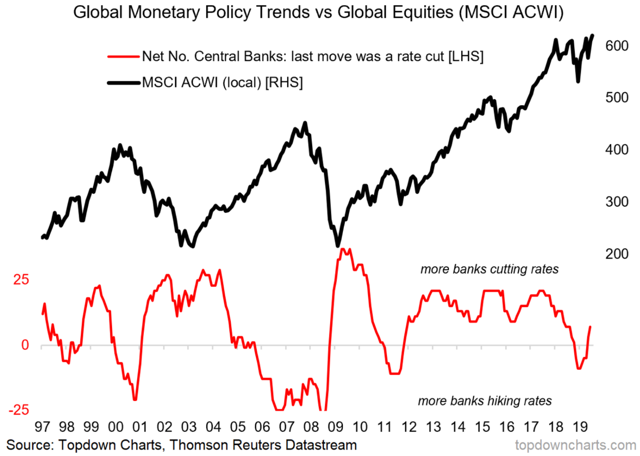

The chart in focus today comes from a report that outlined and explored further the global monetary policy pivot that appears to be underway.

The chart shows the net number of central banks whose last interest rate move was a cut. On first impression, there is a fairly clear and fairly logical relationship between this indicator and the global equities benchmark.

Specifically, we track 37 central banks across emerging and developed economies and use a simple formula to check and sum the net number of central banks hiking vs. cutting interest rates. The global equities benchmark we are using is the MSCI All Countries World Index, which is displayed in local currency terms.

As noted, there appears to be a relatively clear link between the indicator and global equities performance, in that when more banks are hiking rates, global equities tend to do worse and when more banks are cutting rates, global equities tend to do well.

It makes economic sense in that tighter monetary policy acts as a headwind to both risk taking and the economic/earnings cycle. Through 2018, we saw substantial monetary policy tightening both in terms of interest rates and central bank balance sheets.

Around the turn of the year, central banks across the globe began to quickly reconsider their previous tightening measures, and in aggregate, we saw a clear shift to easing. Most visibly and most talked about was the Fed.

We anticipate there is further room to run on this theme as more central banks join the global policy pivot and as central banks ease further.

Along with some promising early signs on the global economic outlook, and generally fair/cheap valuations across global equities (perhaps with the exception of the US), this adds up to a constructive outlook for global equities.

Hence, as mentioned at the start, given the progress of the policy pivot, we retain a preference to overweight risk assets and remain optimistic on the global growth outlook.

Article by Top Down Charts