As part of Merk’s in-house research we regularly evaluate a consistent set of charts covering the economy, equities, fixed income, commodities and currencies. The aim is to keep our eyes open and to look through the noise of the headlines, avoiding the distractions of sensationalized click-bait. In sharing this content, we offer a cross-check to your own thinking and aim to add value to your own process.

Q2 hedge fund letters, conference, scoops etc

Today’s topic: The U.S. Business Cycle

Is the Economic Expansion Over?

U.S. Business Cycle Report

August 2019

Nick Reece, CFA – Senior Analyst & Portfolio Manager, Merk Investments LLC

Why is the Business Cycle Important?

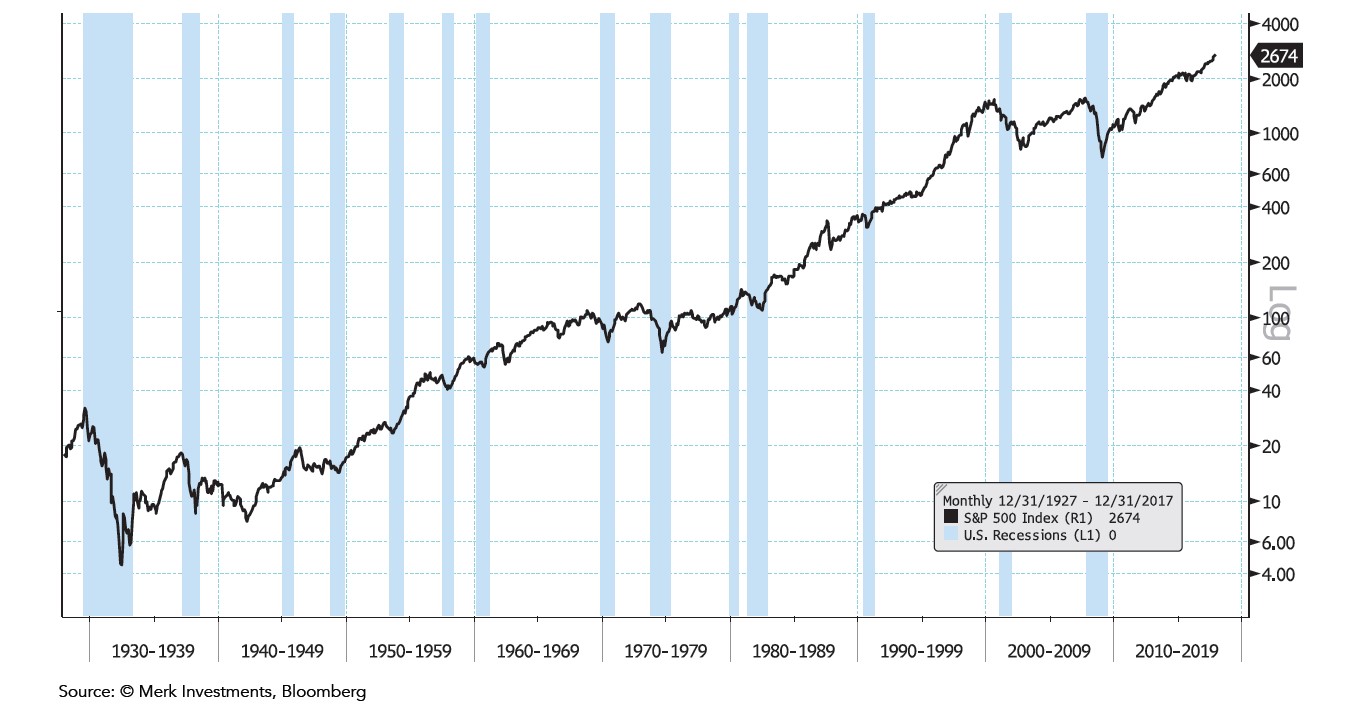

S&P 500 (log scale) and official National Bureau of Economic Research (NBER) U.S. Recessions

Analysis: Over the 90 years between 1927 and 2017, the average S&P 500 monthly return during expansions was +0.89% (889 months), compared to an average S&P 500 monthly return during recessions of -0.71% (191 months). In terms of proportions of time: expansion months account for about 80% and recession months about 20%. The business cycle also has important implications for Fed policy. *Note that recessions are not announced by the NBER until well after their start dates*

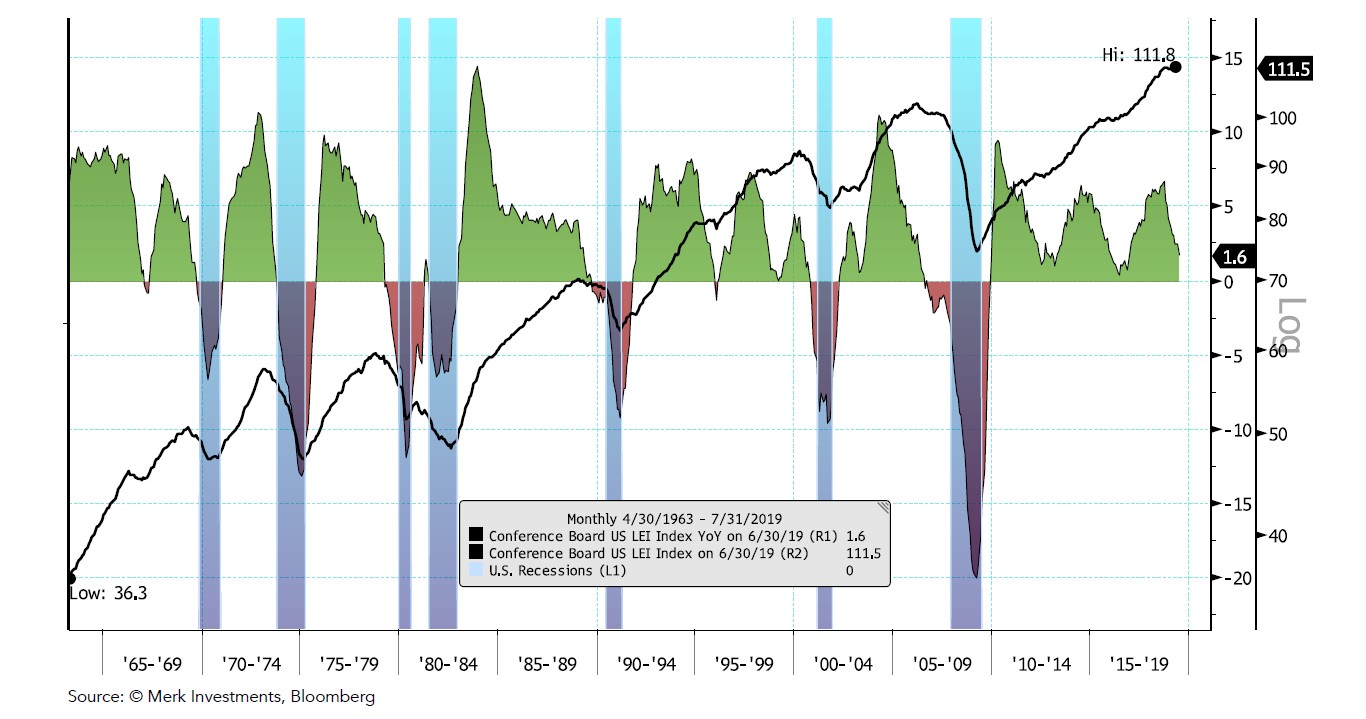

U.S. Leading Economic Indicators (LEIs) Index

Conference Board’s LEI Index and YoY Rate of Change

Analysis: Since last month’s report the LEI YoY rate of change decreased: from +2.5% to +1.6%. Over the past several months momentum has slowed, but given that the YoY rate of change remains positive, history suggests a recession is unlikely to start within the next six months. However, the index level is below its prior cycle highs. This picture keeps me generally positive on the outlook for the U.S. economy. Chart Framework: I’d get incrementally negative on the business cycle outlook if the LEI YoY went negative.

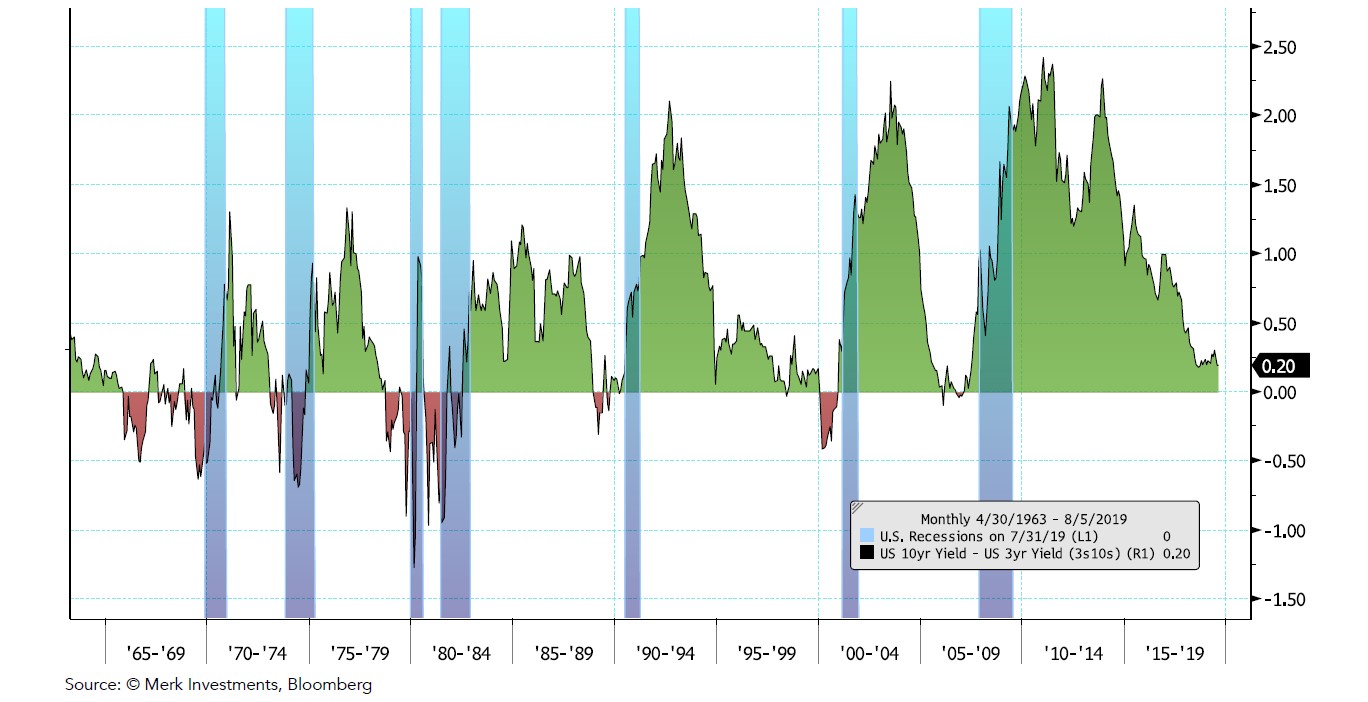

U.S. Yield Curve Steepness

(10yr yield – 3yr yield)

Analysis: The 10yr-3yr yield curve is still positively sloped, meaning the 10yr yield is higher than the 3yr yield. The yield curve steepness is slightly flatter since last month’s report, and the bigger picture flattening trend appears to continue. The 10yr-3yr curve may invert in the coming quarters. Chart Framework: I’d get incrementally negative on the medium term business cycle outlook if the yield curve inverted (i.e., 3yr yield > 10yr yield).

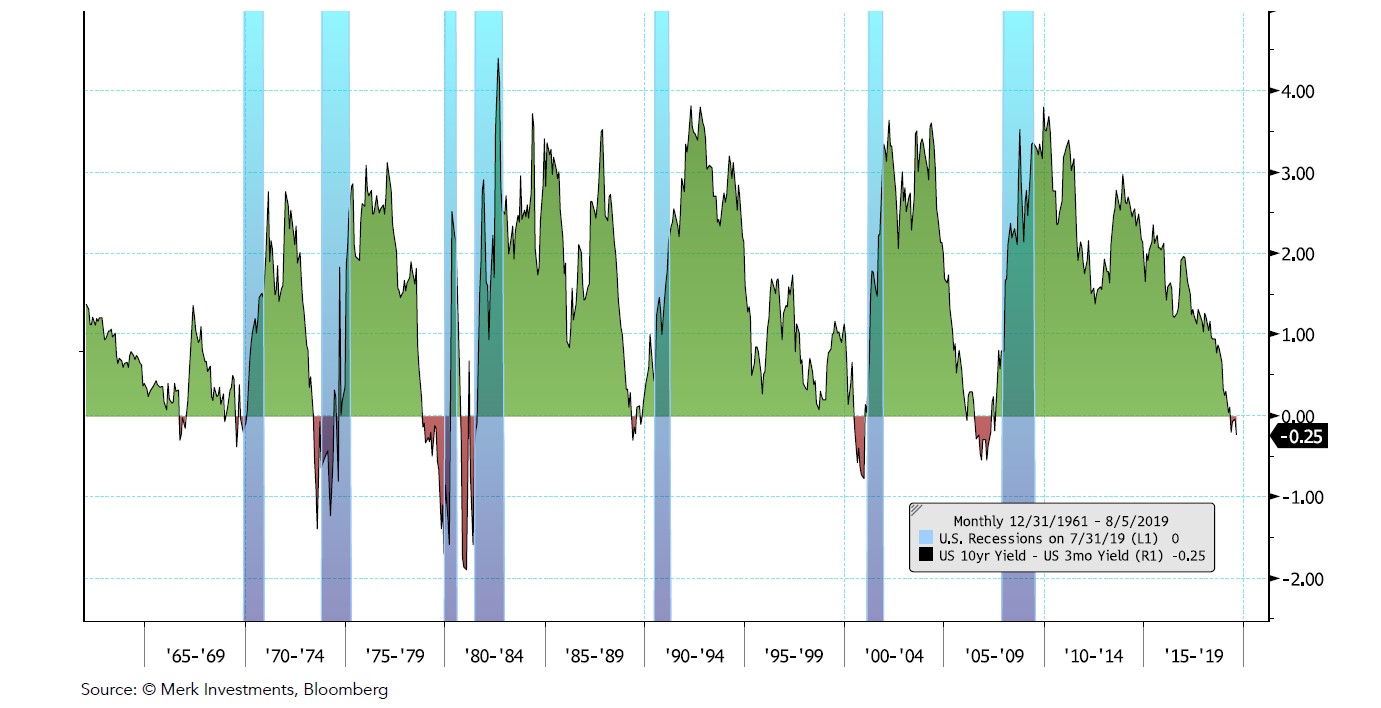

U.S. Yield Curve Steepness

(10yr yield – 3mo yield)

Analysis: A cross reference to the 10yr-3m yield curve shows a more concerning picture, inverted at -25bps. As with the 10yr-3yr, 10yr-3m inversion has been a strong recession warning signal— however, it is worth noting that the 10yr-3yr (shown on the previous page) has always inverted prior to recessions and still has not (yet) inverted.

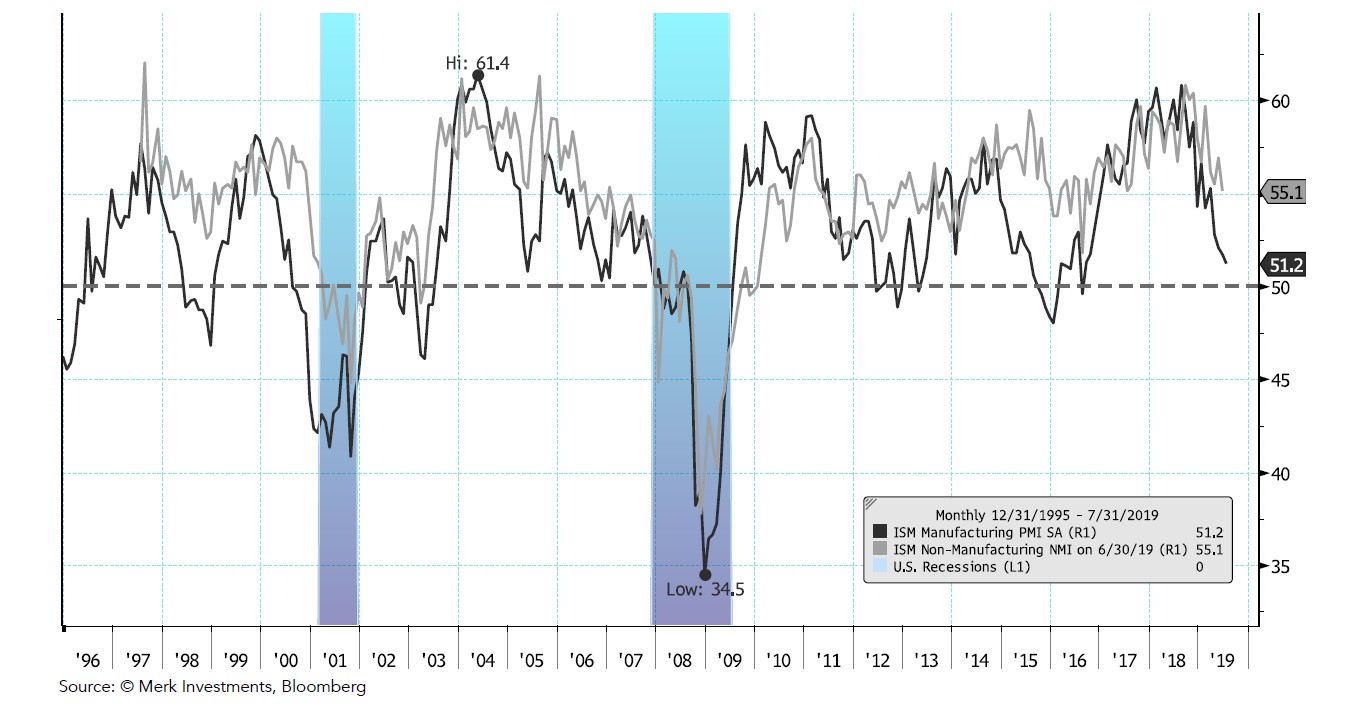

U.S. PMIs

Manufacturing and Non-manufacturing (aka Services) PMIs (Purchasing Managers Index)

Analysis: Manufacturing PMI ticked down over the past month, from 51.7 to 51.2, but is still generally at a level consistent with a growing economy. Chart Framework: I’d get incrementally negative on the business cycle outlook if the manufacturing PMI fell below 50.

We invite you to download a copy of the chart book (PDF).

When you become a premium subscriber, the remainder of the month is free with full access to all premium reports that also include select premium chart books and other benefits; then, the price is only $10 a month.You can cancel any time.

Please also view our premium charts:

The investing audience should view this content in the context of their individual investment process, time-horizon, and goals.

| Publication Date | Chart Book Category | Video | Additional | |

| August 7, 2019 | U.S. Business Cycle | |||

| July 31, 2019 | Fed Chart Book | |||

| July 17, 2019 | U.S. Equity Market | |||

| July 10, 2019 | U.S. Business Cycle | |||

| June 26, 2019 | U.S. Equity Market | |||

| June 19, 2019 | Fed Chart Book | |||

| June 12, 2019 | U.S. Business Cycle | |||

| May 15, 2019 | U.S. Equity Market | |||

| May 8, 2019 | U.S. Business Cycle | |||

| May 1, 2019 | Fed Chart Book | |||

| April 17, 2019 | U.S. Equity Market | |||

| April 10, 2019 | U.S. Business Cycle | |||

| March 20, 2019 | U.S. Equity Market | |||

| March 13, 2019 | U.S. Business Cycle | |||

| February 27, 2019 | Currencies (G10) | |||

| February 13, 2019 | U.S. Equity Market | |||

| February 6, 2019 | U.S. Business Cycle | |||

| January 30, 2019 | Fed Chart Book | |||

| January 16, 2019 | U.S. Equity Market | |||

| January 9, 2019 | U.S. Business Cycle | |||

| December 20, 2018 | U.S. Equity Market | |||

| December 19, 2018 | Fed Chart Book | |||

| December 12, 2018 | Business Cycle | |||

| November 14, 2018 | U.S. Equity Market | |||

| November 08, 2018 | Fed Chart Book | |||

| November 07, 2018 | Business Cycle | |||

| October 17, 2018 | U.S. Equity Market | |||

| October 10, 2018 | Business Cycle | |||

| September 26, 2018 | Fed Chart Book | |||

| September 19, 2018 | U.S. Equity Market | |||

| September 12, 2018 | Business Cycle | |||

| August 29, 2018 | U.S. Interest Rates | |||

| August 22, 2018 | U.S. Inflation | |||

| August 15, 2018 | U.S. Equity Market | |||

| August 08, 2018 | Business Cycle | |||

| August 1, 2018 | Fed Chart Book | |||

| July 18, 2018 | U.S. Equity Market | |||

| July 12, 2018 | Business Cycle | |||

| June 14, 2018 | U.S. Equity Market | |||

| June 13, 2018 | Fed Chart Book | |||

| June 6, 2018 | Business Cycle | |||

| May 23, 2018 | U.S. Inflation | |||

| May 16, 2018 | U.S. Equity Market | |||

| May 9, 2018 | Business Cycle | |||

| May 2, 2018 | Fed Chart Book | |||

| April 19, 2018 | U.S. Equity Market | |||

| April 10, 2018 | Business Cycle | |||

| March 21, 2018 | U.S. Equity Market | |||

| March 14, 2018 | Business Cycle | |||

| February 14, 2018 | U.S. Equity Market | |||

| February 7, 2018 | Business Cycle | |||

| January 17, 2018 | U.S. Equity Market | |||

| January 10, 2018 | Business Cycle | |||

| December 12, 2017 | Business Cycle |

Article by Axel Merk, Merk Investments