Earlier this year, Jeremy Siegel said that, “75/25 is the new 60/40,” a recommendation to raise stock allocations to make up for lower bond yields. However, what matters for investors saving for retirement is not the asset class performance, but how those returns translate into retirement consumption.

Q2 2020 hedge fund letters, conferences and more

To examine the impact of increasing stock allocations, I’ll focus on retirement planning and show impacts on both the average and variability of retirement withdrawals.

Spoiler alert – as the title hints, 75/25 versus 60/40 doesn’t matter that much.

Background

The importance of asset allocation received a boost from the 1980s from a paper by Brinson, Hood, and Beebower (BBH), which many interpreted as “proving” that the key differentiator of pension plan performance was the stock/bond mix, and manager selection didn’t have much influence.1 In fact, BBH demonstrated that asset allocation explained the variability of the performance in the sample they studied, not the performance itself. More recently, with increased focus on index funds and passive investing, asset allocation has become a more prominent consideration as attention has shifted away from selecting active funds or individual stocks. Over the past few years, I have received questions from DIY investors trying to decide on the best allocation to target. Typically, they are trying to decide between relatively high stock allocations such as 60/40 versus 75/25, not 20/80 versus 30/70, and not wide differences like 30% stocks versus 100% stocks.

Example

I’ll use an example of a retirement-age couple with a 30-year planning horizon and $1 million in savings, trying to decide between 60/40 and 75/25. I assume that they have sufficient sources of sustainable lifetime income such as Social Security, pensions, or annuities so that they can comfortably take market risk, and I’ll focus the analysis on the savings portfolio.

A key assumption for modeling retirement outcomes is future average stock returns. The size of the assumed equity return premium (ERP) of stocks over bonds will directly impact the sensitivity of retirement outcomes to different asset allocations.

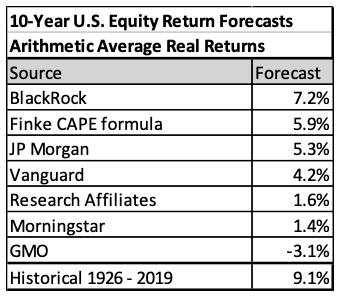

In January of this year, Christine Benz of Morningstar provided a summary of predictions for the next 10 years from various investment firms and research organizations. I show those in the table below expressed as real arithmetic average returns, which is the return definition I will use for Monte Carlo modeling. Besides the forecasts provided by Benz, I also include a CAPE-based forecast derived from Michael Finke’s recent Advisor Perspectives article, and I also show the historical average (1926 – 2019) for large capitalization U.S. stocks from Ibbotson/Morningstar.

These forecasts all assume lower than historical-average stock returns. These are forecasts for the U.S., and some of the forecasters also assume that higher equity returns may be found internationally and/or returns after 10 years may be somewhat higher.

The wide variation in forecasts reflects double uncertainty about the average equity premium to expect plus year-to-year return variability as I discussed in this 2015 Advisor Perspectives article. Bill Sharpe, in chapter 7 of his RISMAT book on retirement income, also discussed the uncertainty in future equity-return forecasting. He offered the insight that, based purely on a statistical view, estimation errors are smaller for second moments (standard deviations) than for first moments (means). He cautioned that, “When estimating future return distributions, humility is very much in order.”

Read the full article here by Joe Tomlinson, Advisor Perspectives