With the bull market running for over nine years now, not a day goes by where someone doesn’t claim the end is near. Nonetheless, the economy continues to strengthen, and no one knows for sure when the next bear will arrive. However, we do know that not all stocks move in lockstep with the broad market indexes, and opportunities constantly arise to cater your investment portfolio to meet your own specific needs. This article reviews our top 10 high-yield contrarian opportunities, from across 10 different investment categories, all for you to consider as you build and manage your own investment portfolio.

[klarman]

Q2 hedge fund letters, conference, scoops etc

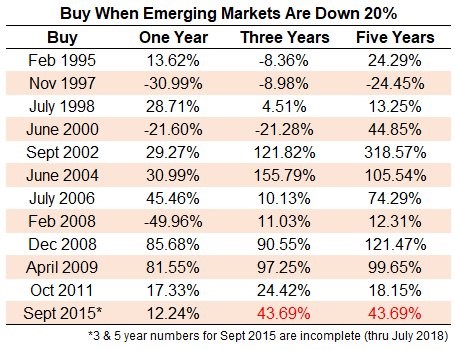

Before getting into the specific names on the list, it’s worth considering some contrarian perspective from different sources. First, here is an interesting chart from A Wealth of Common Sense about contrarian opportunities in emerging markets (if you don’t know, emerging markets are significantly underperforming the US lately).

It seems being a contrarian with regards to emerging markets has historically paid off, but of course past performance is not indicative of future results.

For more perspective, according to Bank of America’s Chief Investment Strategist, Michael Hartnett:

“The ‘Great Bull’ market is over as economic growth becomes less certain, interest rates rise and debt becomes an overhang.”

Hartnett explains that “Interest rate hikes from the Fed and other central banks will have a significant impact on growth that may not be anticipated in the markets.” And he advises investors to focus on inequality, innovation, and immortality; and that these would benefit pharma companies, technology disruptors, and inflation plays. These will all three be key point later in this report as we get into the top 10 list.

And of course there are myriad false positives, when investors are searching for a reason to believe the bull market should end, perhaps such as the Hindenburg Omen, as is intelligently dissected in Jeff Miller’s recent article: Hindenburg Omen Flashing Red, Is It Reliable?

The Top 10 List…

Regarding the construction of our top 10 list (below), we have taken into consideration that the bull market may NOT be ending anytime soon, and therefore our diversified list of multi-category high-yield opportunities includes high-yield investments that can perform very well if the bull keeps running, as well as those that can perform very well if a bear market arrives. All of the high-yield ideas are contrarian in nature. And without further ado, here is the list…

The Energy Sector:

10. PermRock Royalty Trust (PRT), Yield: 12.1%

If you are concerned about the negative impacts of inflation, especially with the Fed expected to keep increasing interest rates, then you might want to consider the energy sector. For example, according to this US News & World Report:

“Energy is the best-performing sector in the S&P 500 during periods when inflation rises by 3 percent or higher.”

Also, according to Market Realist:

“Investors looking for an alternative to gold can consider investing in the energy sector to shield themselves from the wealth-eroding effects of inflation.

One way to get exposure to the sector is PermRock Royalty Trust (PRT), which just started trading earlier this year. Not only does PermRock pay a big monthly yield of 12.1% (albeit a variable), but the price has recently sold-off.

We first highlighted PermRock for our members last month. Specifically, we reviewed the valuation and risks in this article:

And although we have not yet taken a position, PRT’s big monthly yield is increasingly tempting, especially after the recent sell-off.

Emerging Market Dog of The Dow:

9. Procter & Gamble (PG), Yield: 3.4%

If PermRock is a little too esoteric for you, you might be interested in more blue chip opportunities, such as “Dogs of the Dow,” which is a contrarian strategy by nature whereby an investor invests annually in the Dow Jones stocks with the highest yields (the assumption being, that Dow Jones companies don’t alter their dividend to reflect trading conditions and, therefore, the dividend is a measure of the average worth of the company).

One attractive Dog of the Dow, in our opinion, is Procter & Gamble. Not only is P&G worth considering because it is a Dog of the Dow, but it also has a large exposure to non-US operations (emerging markets, in particular), which have been underperforming lately, and may be due for a rebound, as we described earlier in this report. We also recently did a more detailed write-up on P&G for our members, and it is now available here.

Big-Yield REITs:

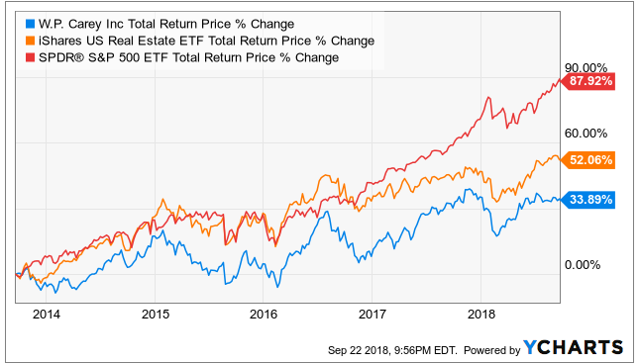

8. WP Carey REIT (WPC), Yield: 6.2%

Considering REITs rely heavily on borrowing to grow their businesses, you might not think they’re the most attractive investment sector right now, considering the current rising interest rate environment. However, there remain some attractive opportunities, on a case-by-case basis, such as WP Carey REIT.

WPC invests in high-quality single-tenant industrial, warehouse, office and retail properties subject to long-term leases, and the company is well-diversified by tenant, property type, geography and industry. It also trades at an attractive valuation, in our view. You can read our recent write-up (previously available to members-only) here…

Equity Closed-End Funds (CEFs):

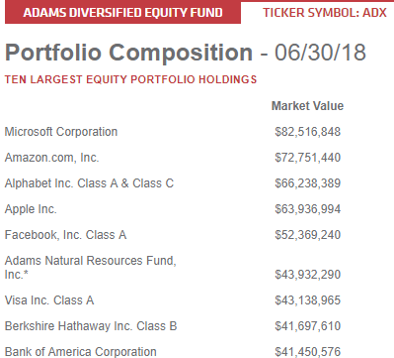

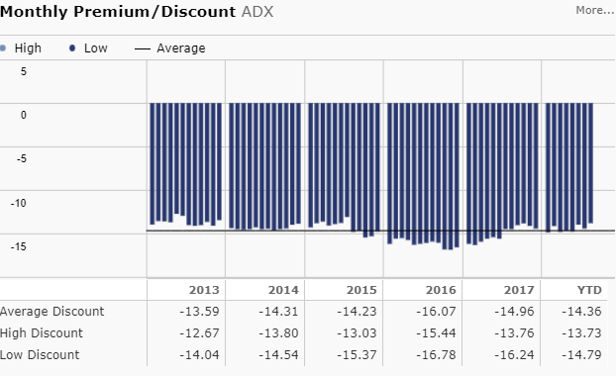

7. Adam’s Diversified Equity Fund (ADX), Yield: 9.8%

One of the common misconceptions among many cash-flow and income-focused investors, is that they should only buy securities that offer bid dividends. The problem with this is that they often end up overly concentrated in only the few highest yielding sectors of the market (i.e. they’re risks are too concentrated). One way to address this is through attractive equity closed-end funds, or CEFs.

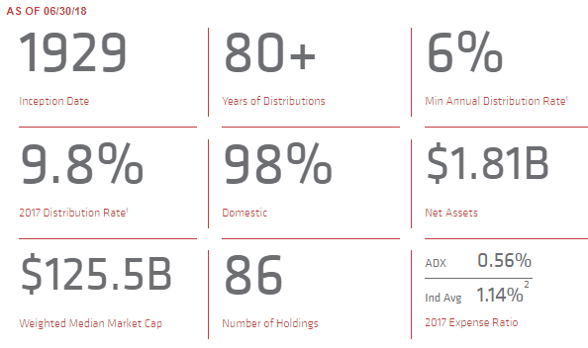

For example, the Adams Diversified Equity Fund (ADX) has been paying a high yield for over 80 years, and it does so by carefully managing a portfolio of investments diversified across many market sectors. The fund relies on a combination of dividends and capital gains to generate the high yield it pays to its investors, and this can be an attractive high income diversifier within an income-focused investment portfolio. Here is a look at the recent top holdings, and it’s not what you’d expect from such a high-yielder, but it is a good way to get some high-yield diversification into your portfolio.

And here are a few more noteworthy ADX stats for you to consider:

A few of the things that make ADX particularly attractive are its relatively low management fee, the fact that it trades at a worthwhile discount to its net asset value (you’re basically buying the underlying securities at a discount to their market price), and its big year-end distribution is right around the quarter (ADX pays smaller distributions in the first three quarters of the year, followed by a large one in the fourth quarter).

We own ADX, and we’ve written in more detail about it, as well as several additional equity CEFs we currently own, in this members-only report.

Preferred Stocks:

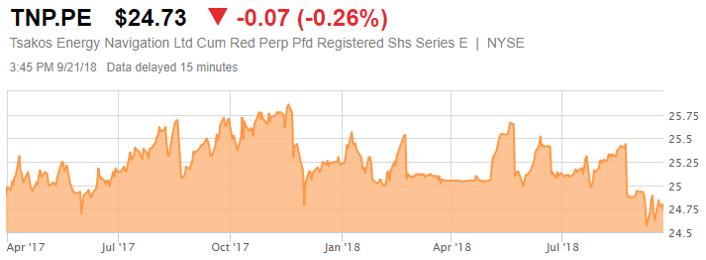

6. Tsakos Energy Navigation (TNP-E), Yield: 9.4%

If you can’t handle the volatility of common stocks, you might want to instead consider preferred shares; they generally don’t offer the same price appreciation potential as common shares, but they’re usually considerably less volatile and often offer considerably higher yields.

One group of high-yield preferred stocks that are worth considering are those offered by Tsakos Energy Navigation (TNP)—a Greek company that trades in the US, and provides seaborne crude oil and petroleum product transportation services worldwide. The company has a variety of high-yield preferred shares that are available to investors (see our article link below). Tsakos’ entire industry has faced challenges in recent years (that’s why this is a contrarian opportunity), but we believe the preferred shares are attractive. You can read our full write-up on Tsakos shares, which was previously available to members-only, here:

Article by Blue Harbinger