Commodity trader Trafigura has accumulated a massive debt of $33b and has recorded a negative operating cash flow of $7.3b since 2016. When they finance Trafigura, banks and bondholders probably derive comfort from the valuation of Trafigura’s assets, more than its cash flows. We found that Trafigura ignores economic reality to aggressively overvalue hundreds of millions in debt securities issued by an associate. In our opinion, the group has fabricated profit via an accounting loophole.

Q1 hedge fund letters, conference, scoops etc

Trafigura owns a stake of 49.5% in Porto Sudeste, an iron ore port in southeast Brazil with the capacity of 50 million tonnes. As an associate, the carrying value is a modest $42m on the balance sheet as of September 2018. Trafigura also holds debt securities of Porto Sudeste with a much more substantial carrying value of $490m. The securities are junior debt repaid through royalties derived from volumes shipped by the port. From Trafigura’s annual report: “The holders of the instrument are entitled to a fixed royalty payment per metric tonne processed by the port and therefore have direct exposure to the business risks of Porto Sudeste.”

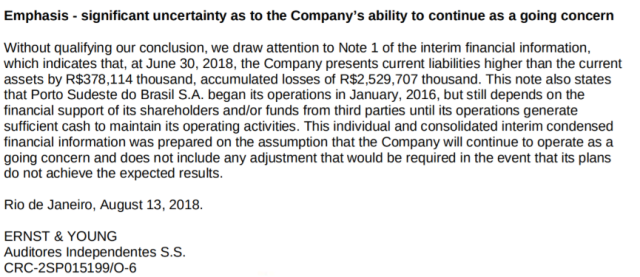

Trafigura is substantially at risk on Porto Sudeste but there is one big issue: the auditor of Porto Sudeste (E&Y) has underlined the significant uncertainty of Porto Sudeste’s ability to continue as a going concern. Below the warning issued by the auditor:

The port has clearly not met expectations. Clients have been missing. The port shipped only 9.5 million tonnes in 2018, i.e. 20% of its capacity. No royalties have been paid as not enough cash was available.

The debt securities are traded and their tickers are FPOR11 and PSVM11, depending on whether the investors are qualified to hold such funds under Brazil’s regulations. Amid the port’s trouble, the price of both debt securities has collapsed since they started trading in 2015. FPOR11 fell by 90% since inception while PSVM11 dropped by 85%.

FPOR11

PSVM11

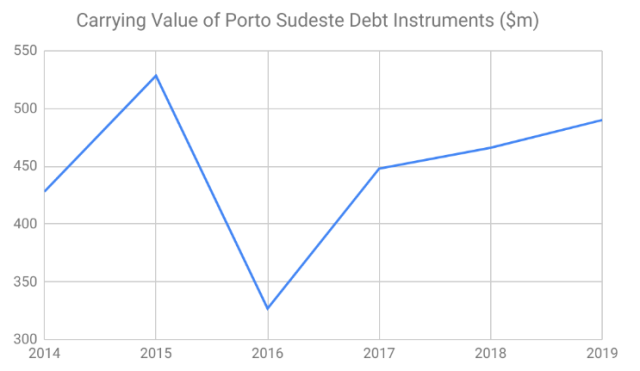

However, you would not see this drop on Trafigura’s balance sheet. In fact, the carrying value of the debt securities has increased from $428m to $490m in four years and a half.

One might assume that Trafigura acquired more securities, which would explain the increase. On the contrary, Trafigura offloaded $91.7mm FPOR11 securities in 2016.

Trafigura does not disclose how many debt securities the company holds and the ratio of PSVM11/FPOR11. If we assume that Trafigura holds FPOR11 debt securities (the most likely assumption as it is a qualified investor and most of the issued securities are FPOR11), we estimate the market value of Trafigura’s securities at $49m. That means a gap between carrying value and market value of $441m. In our calculation, we conservatively ignored the sale of $91.7m FPOR11 securities in the 2016 fiscal year because Trafigura did not disclose the exact timing of this sale and the price dropped quickly in that period. The valuation gap is very large and we strongly believe that Trafigura should disclose the market value of these securities.

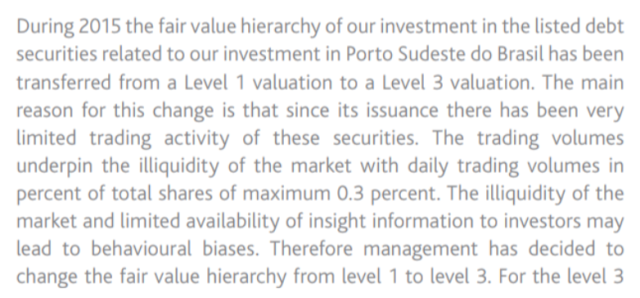

How can Trafigura maintain such a high carrying value for these securities, given the price of these securities has collapsed? Listed debt securities should be marked-to-market, and gains/losses should flow through the income statement. This is what Trafigura used to do until 2015. That year, Trafigura disclosed in the annual report that it had switched from marking-to-market to a level 3 cash flow model to value them. This change in policy happened when prices were falling. The justification for the change in policy at that time is puzzling to the say the least.

The company claims the market is not liquid enough and has “limited insight”, making it vulnerable to “behavioural biases”. It seems Trafigura thinks they are smarter than the market when valuing securities. The lack of liquidity was the infamous excuse used by Noble Group, another commodity trader, to justify its 48-times overvaluation of its associate Yancoal.

If Trafigura sold all these debt securities, it would have to write them down in full. As a result, Trafigura is likely stuck with securities that are continuing to fall with no improvement in sight.

After Trafigura adopted the level 3 methodology, the group booked a revaluation gain of $78.5m in 2015 when securities were plunging. In 2016, Trafigura was more conservative: the company recognized an impairment loss of $125.9m after it sold $91.7m debt securities. However, the company quickly reversed course. It recorded a $135.7m gain in 2017 because of “improved projections of the throughput of the port and a decrease in the discount factor relating to lack of marketability”. An additional gain of US$18.7m was recorded in 2018 as well, and once again $24m in the first half of 2019. The various gains boosted the company’s net profit. We view this profit as fabricated as it ignores the economic reality of the port and the declining market value of the securities. The auditor’s warning for Porto Sudeste also reflects the financial deterioration.

The discount factor for lack of market liquidity was initially 38% in 2015. It was lowered to 26% in 2016, and then to 10% in 2017. If the discount for liquidity is reduced annually, we can assume that the market is increasingly liquid. So why aren’t these securities marked-to-market, as they should be?

In Trafigura’s cash flow model, the port’s revenues are calculated over a period up to 2064. Trafigura’s output assumptions have been incorrect in the past. In 2016, it expected to “ramp-up exports through Porto Sudeste to 15 million tonnes in 2017 and 20 million the following year.” As mentioned, in 2018, the volume of Porto Sudeste was only 9.5 million tonnes.

The fortunes of Porto Sudeste are not improving. Brazil’s Vale has entered an agreement to buy another Brazilian iron ore miner, Ferrous Resources, which is an existing client of Porto Sudeste. In the future, Ferrous is expected to use Vale’s infrastructure rather than that of Port Sudeste. Trafigura lodged a complaint to the competition watchdog in Brazil as it feared that “any move by Vale to shift these shipments to its own infrastructure could hurt the port.” However, Brazil’s antitrust watchdog has just approved Vale’s acquisition of Ferrous Resources. Porto Sudeste is likely to lose an important client.

Trafigura values at $490m the junior debt securities of a company with significant uncertainty as a going concern. In our experience, companies that ignore market prices to value listed securities and prefer their own cash flow model inevitably have to face reality.

Trafigura is not listed so it has no incentive to boost its share price, but it has a massive $33b debt, very large operating cash outflow, and covenants that would probably be affected by the impairment of these assets.

We will cover other issues on Trafigura’s financial statements. We are short Trafigura’s debt.

Article by Iceberg Research