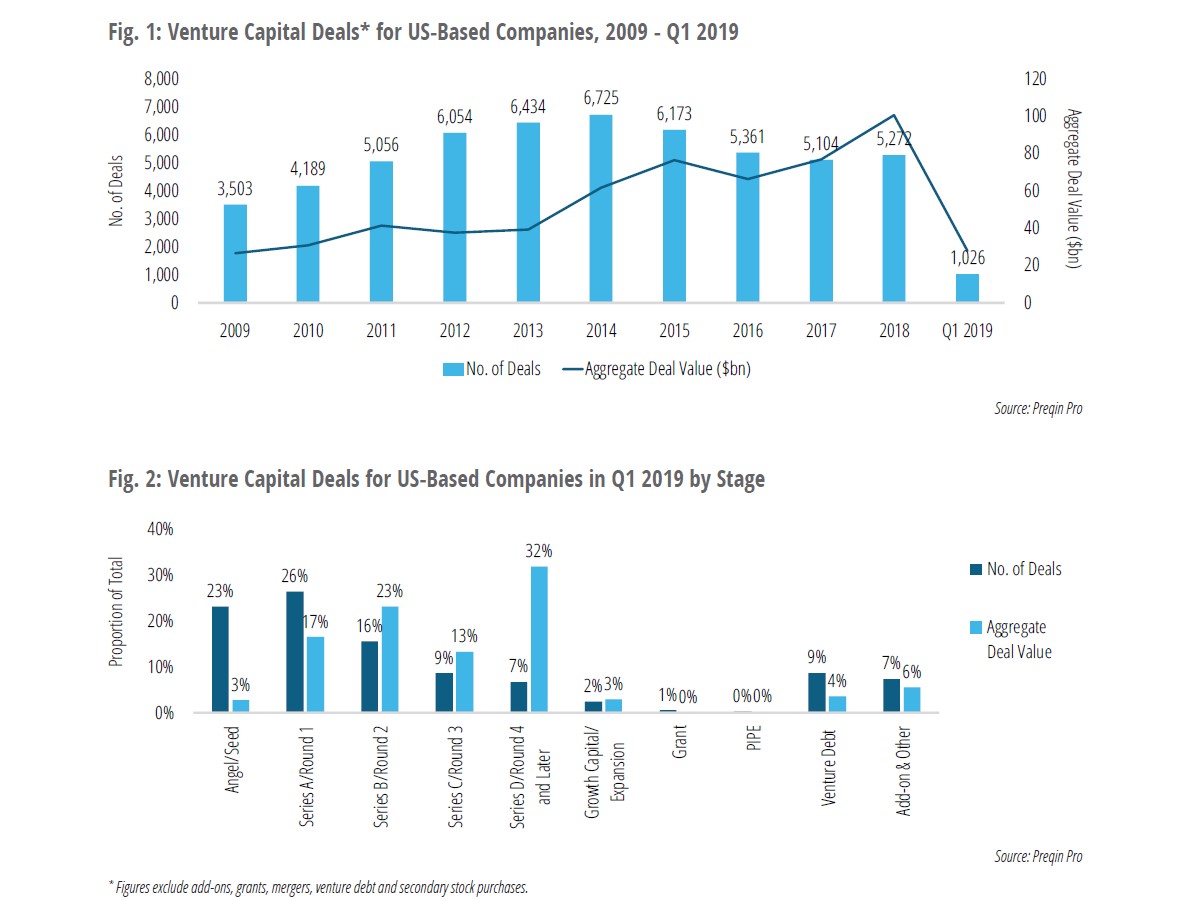

Following a record 2018, venture capital activity in the US is off to a robust start. In the first quarter of 2019, 1,026 venture capital deals were completed for an aggregate $28bn, up from $19bn in Q1 2018. This report, produced by Preqin in partnership with First Republic Bank, explores the booming venture capital industry in the US, and how we can use activity in Q1 to envisage where the rest of 2019 may lead us. Using the latest data from Preqin Pro, we look at the biggest deals and exits of the quarter, as well as the largest venture capital funds closed, to identify the key players in the industry and the ones to watch.

Q1 hedge fund letters, conference, scoops etc

Foreword

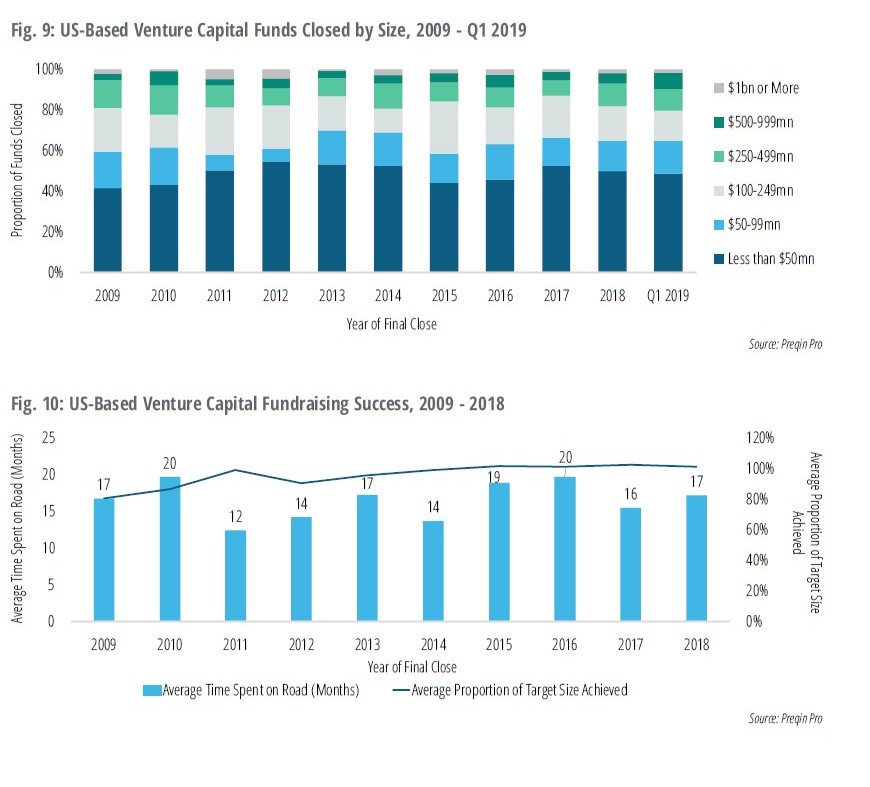

Following a record 2018, venture capital activity in the US is off to a robust start: in the first quarter of 2019, 1,026 deals were completed for an aggregate $28bn, up from $19bn in Q1 2018. Continuing the trend of mega-rounds, the top five deals of the quarter accounted for $6.2bn, or 22% of the total amount of venture capital invested.

Some of this quarter’s highlights include:

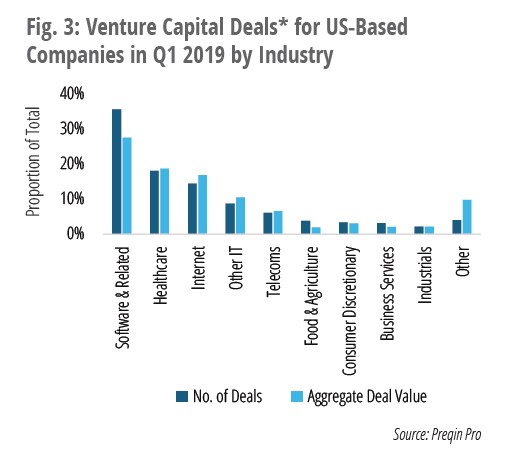

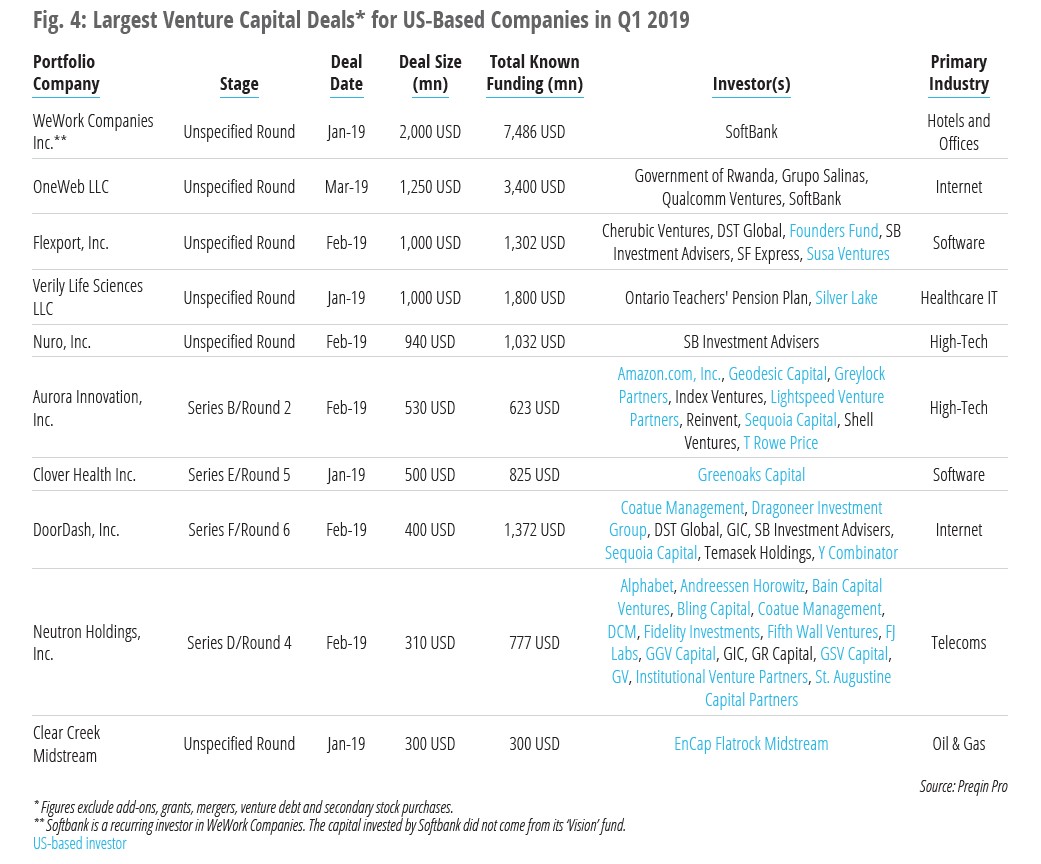

- Early-stage investments (Series A and earlier) accounted for 49% of venture capital deals and secured 20% of the aggregate capital invested in Q1 2019, and Series B investments constituted 23% of capital invested. Software represented 36% of deals and 28% of deal value, making it the most active industry for US-based venture capital investment in the quarter.

- As of the end of Q1 2019, there were 129 exits valued at an aggregate $18bn, led by exits for Lyft, Auris Health and SendGrid. Ten venture capital-backed companies went public in Q1 2019 – and with the IPO window opening, many more companies are expected to file in 2019.

- A record 405 US-based venture capital funds closed in 2018, raising $46bn. Based on Q1 2019’s fundraising statistics, 2019 is expected to be an equally strong year, and 96 funds have brought in an aggregate $12bn so far.

- Marking a 22% increase from a year ago, there are a record 952 US-based venture capital funds in market at the start of Q2 2019, seeking an aggregate $89bn. Thirty-six percent of these funds are being raised by first-time managers and target $22bn.

- The first quarter of 2019 alone recorded more micro venture capital fund closures than in 2009 (63 vs. 64 respectively), and four of the top seven performing US-based venture capital funds are micro vehicles. In 2018, 63% of the micro funds closed had managers with prior institutional investing experience, and in Q1 2019 that figure was up to 72% – though, it is worth noting that this number includes managers that raised a prior fund under the same brand (Fund II or later).

- The 10 largest US-based venture capital fund managers have raised $73bn over the past 10 years. Although the top 10 US fund managers cover a range of investment stages, only Sequoia Capital and Bessemer Venture Partners have seed-stage-focused funds.

- Six of the most active investors in US venture capital are pension funds, led by San Francisco Employees’ Retirement System which has 65 known commitments to vintage 2009-2019 venture capital funds. The largest proportion of investors active in US-based micro venture capital funds, however, are fund of funds managers and family offices.

Deals & Exits

Following a record 2018, venture capital activity in the US got off to a positive start in 2019: 1,026 deals were completed for an aggregate $28bn in Q1 2019 (Fig. 1), up from $19bn in Q1 2018, and the top five deals of the quarter accounted for 22% ($6.2bn) of the total amount of venture capital invested in US-based portfolio companies.

Early-stage investments (Series A and earlier) accounted for 49% of venture capital deals in the US in Q1 2019 and 20% of capital invested, and Series B investments constituted 23% of capital invested (Fig. 2). Software was the most active industry for US-based venture capital investment in the quarter, representing 36% of deals and 28% of deal value.

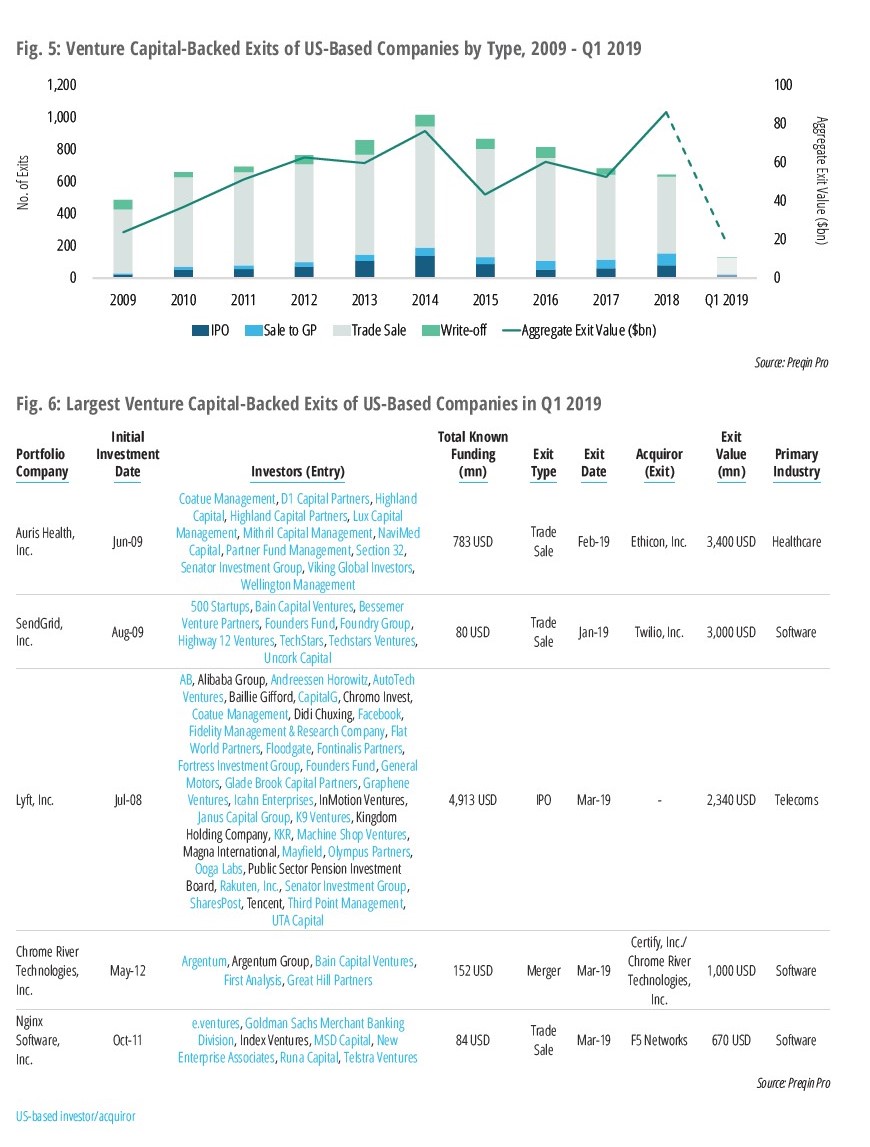

In Q1 2019, there were 129 venture capital-backed exits for US-based companies, valued at an aggregate $18bn (Fig. 5). The number of exits in Q1 2019 has declined compared to the same period last year (146); however, the aggregate exit value has increased compared to the exit value seen in Q1 2018 ($12bn).

As seen in previous periods, trade sales were the most common exit type in Q1 2019: they accounted for 81% of all venture capital-backed exits of US-based portfolio companies, as well as eight of the 10 largest exits for an aggregate $9.8bn, which was led by the $3.4bn trade sale of Auris Health, Inc. to Ethicon, Inc.

Ten venture capital IPOs took place in Q1 2019; headlining these was the much-anticipated IPO for

Lyft, Inc. for $2.34bn, the third largest exit of the quarter (Fig. 6).

Fundraising

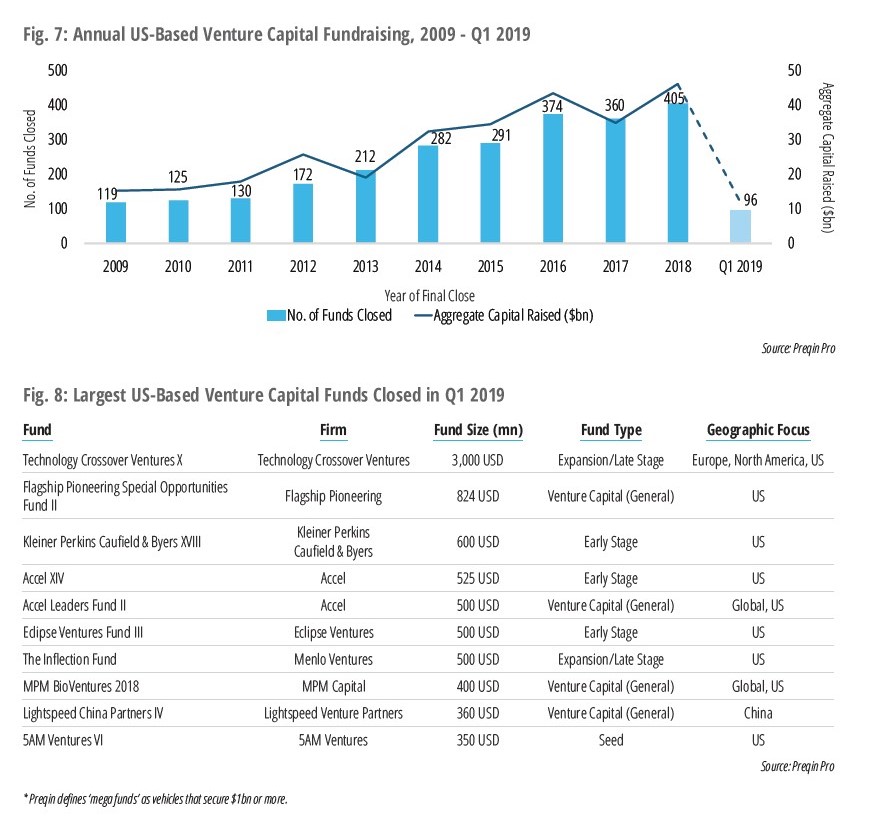

A record 405 US-based venture capital funds closed in 2018, raising an aggregate $46bn. Based on Q1 2019’s fundraising statistics, 2019 is poised to be an equally strong year, with 96 funds bringing in an aggregate $12bn in the first quarter (Fig. 7).

Technology Crossover Ventures was the only US-based venture capital firm to close a mega fund* in

Q1 2019 (Fig. 8). Despite this, the 10 largest funds closed were all raised by experienced managers, many of which raise multiple funds concurrently instead of one large, flagship vehicle. For example, Accel closed Accel Growth Fund V in Q1 2019 in addition to its two venture capital funds, Accel XIV and Accel Leaders Fund II, securing a total $2.5bn.

US-based venture capital funds spent around 17 months in market in 2018, which is generally average for venture capital fundraising over the past decade (Fig. 10). Managers have successfully planned their fundraising strategies: the average fund achieved 101% of its targeted amount in 2018, and 99-102% of its target each year since 2014.

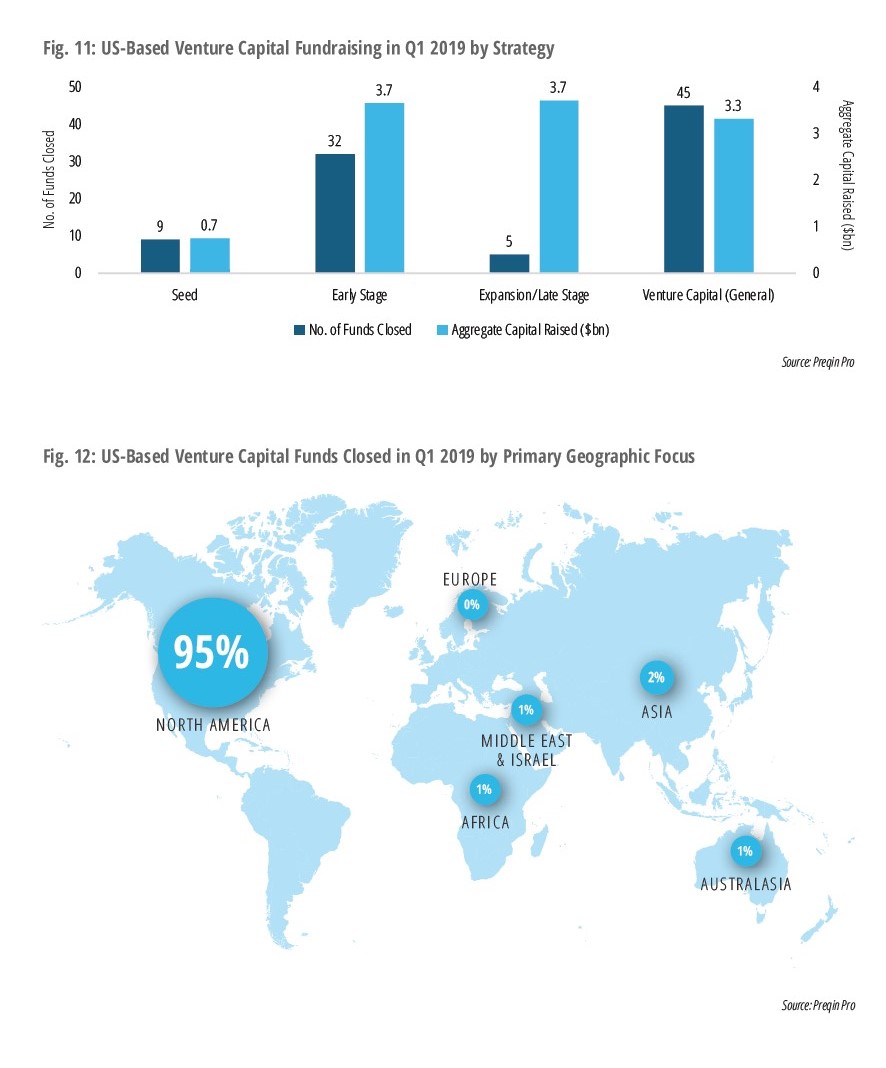

Venture capital funds focused on seed investments are the least common, with only 10% of funds closed in Q1 2019 dedicated to this investment stage (Fig. 11). Meanwhile, only five expansion-stage funds managed to secure a third of all capital raised in the first quarter, thanks to the closure of Technology Crossover Ventures X ($3.0bn) and The Inflection Fund ($500mn), two of the largest funds closed in the quarter.

Almost all (95% of) US-based venture capital funds closed in the past three months are focused on domestic investments (Fig. 12); however, veteran manager Lightspeed Venture Partners closed a set of China-focused funds bringing in $560mn, representing a significant portion of the capital raised to invest abroad.

Funds In Market

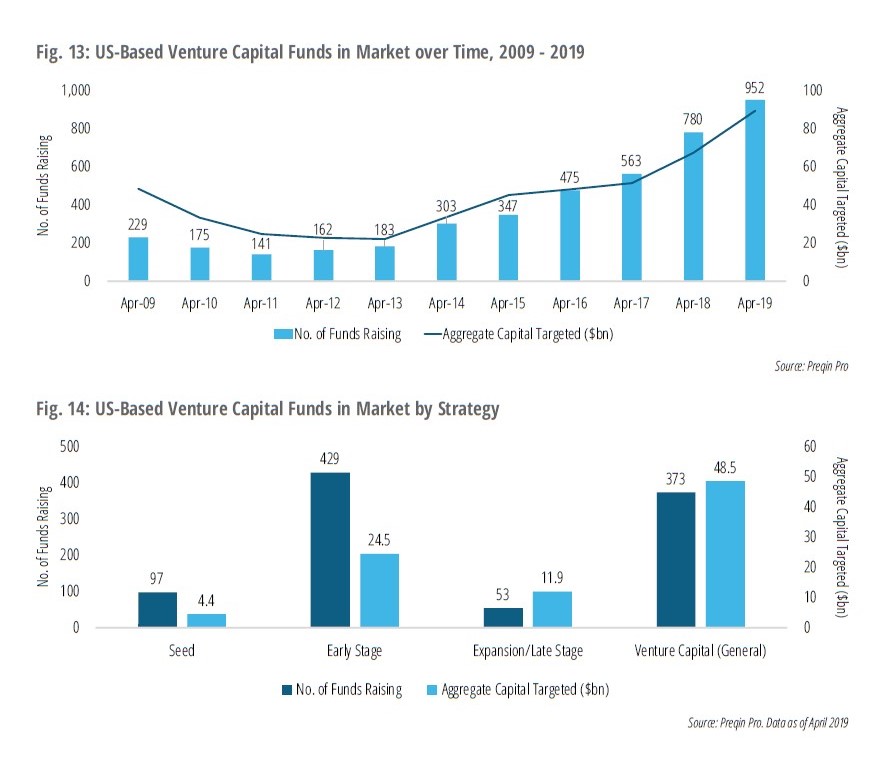

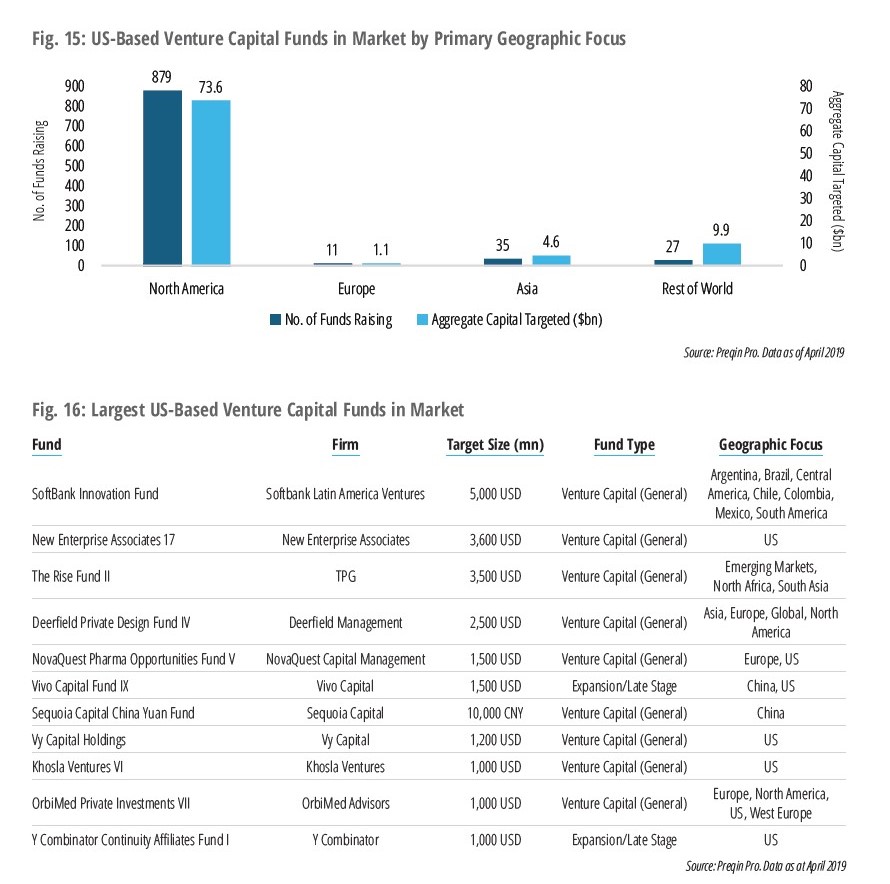

Marking a 22% increase from this time last year, there are a record 952 US-based venture capital funds in market in April 2019 seeking an aggregate $89bn (Fig. 13). Thirty-six percent of these funds are being raised by first-time managers and are targeting a total of $22bn, a slight decrease from the proportion of first-time funds one year ago when 39% of all US-based venture capital funds sought $17bn.

Eleven funds in market are mega funds targeting $1bn or more, comprising 26% of the total capital sought by all US-based venture capital funds on the road. At the head of these mega funds is the newly announced SoftBank Innovation Fund, which is poised to break the record for the largest US-headquartered venture capital fund ever raised with a target of $5bn (Fig. 16). If SoftBank reaches its target, it would dethrone Tiger Global Private Investment Partners XI which raised $3.8bn in Q4 2018.

Funds taking a stage-agnostic investment approach are dominating the fundraising market: 373 vehicles are targeting an aggregate $49bn, 54% of the total capital sought (Fig. 14). The current pool of funds in market has an average fund size of $115mn – a 12% increase from April 2018 ($103mn).

While US-based venture capital funds continue to primarily focus on domestic investments, large funds such as SoftBank Innovation Fund and The Rise Fund II, which concentrate on opportunities in Latin America and emerging markets respectively, are raising the profile of emerging markets investment in the venture capital industry.

Micro Venture Capital

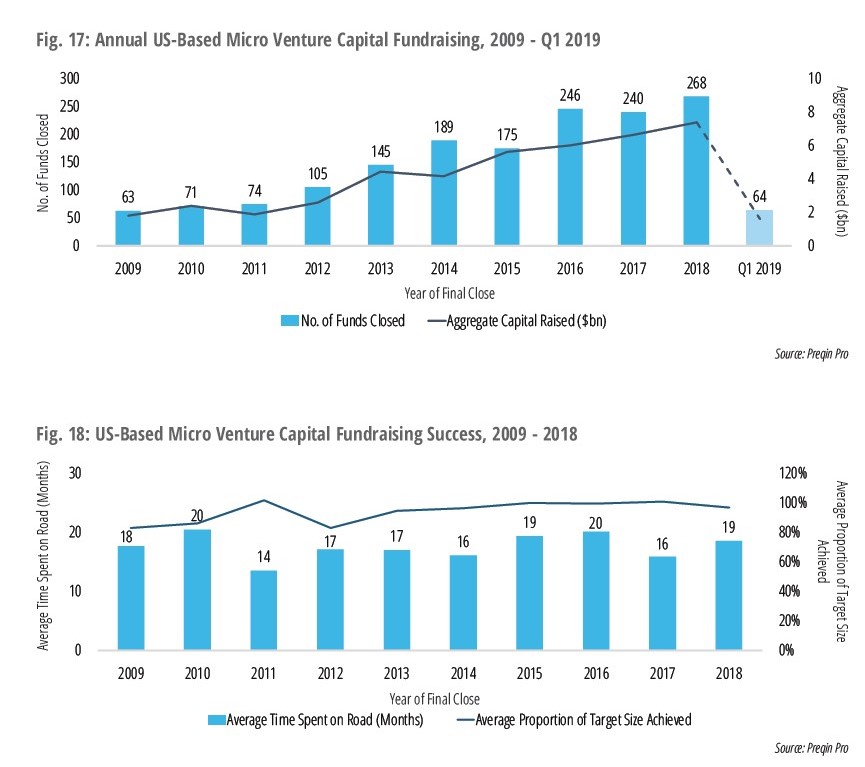

Over the past decade, US-based micro venture capital funds (those worth less than $100mn) have gained traction in the market. In addition to the increasing number of micro venture capital funds reaching a final close, the aggregate capital secured by these funds has steadily risen each year, reaching a record $7.4bn across 268 vehicles in 2018 (Fig. 17). In the first quarter of 2019 alone, 64 micro venture capital funds closed, neatly surpassing the 63 micro venture funds closed during the entirety of 2009.

A trend is visible among the micro venture capital funds closing each year, whereby experienced managers are raising these vehicles more often than first-time managers looking to make a name for themselves. Among funds closed in 2011, the split between micro funds that were raised by experienced and first-time managers was an even 50% – but in 2018, 63% of micro funds closed were managed by experienced firms, and in Q1 2019 that figure was up to 72%. This shows that there is a clear place for smaller funds within the offerings of larger venture capital fund managers.

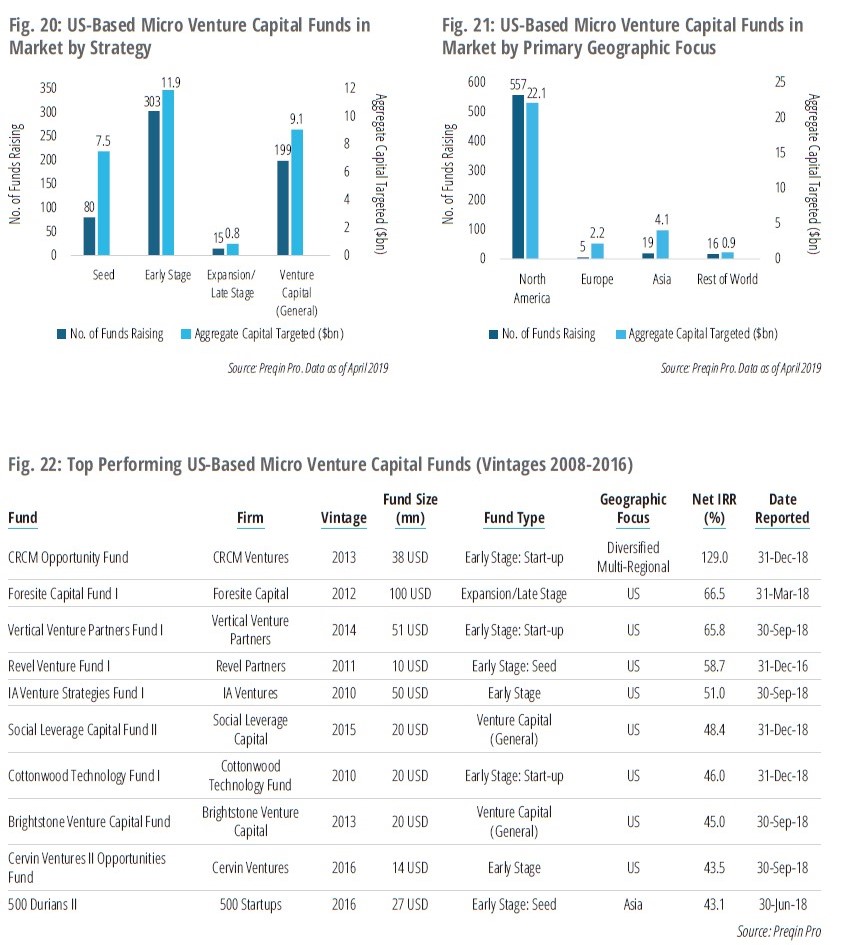

Early-stage funds, including seed funds, account for 64% of US-based micro venture capital funds in market and 66% of targeted capital. General venture capital investing follows, with 199 vehicles in the market target an aggregate $9.1bn (Fig. 20). North America is the targeted destination for the majority (76%) of US-based micro venture capital funds on the road, followed by Asia (14%, Fig. 21).

With a net IRR of 129.0%, CRCM Opportunity Fund is the current top performing US-based micro venture capital fund over the 2008-2016 vintage range (Fig. 22). Managed by CRCM Ventures, the fund implements a diversified approach and, like seven of the top 10 performing US-based micro venture capital funds, targets early-stage investments.

Performance

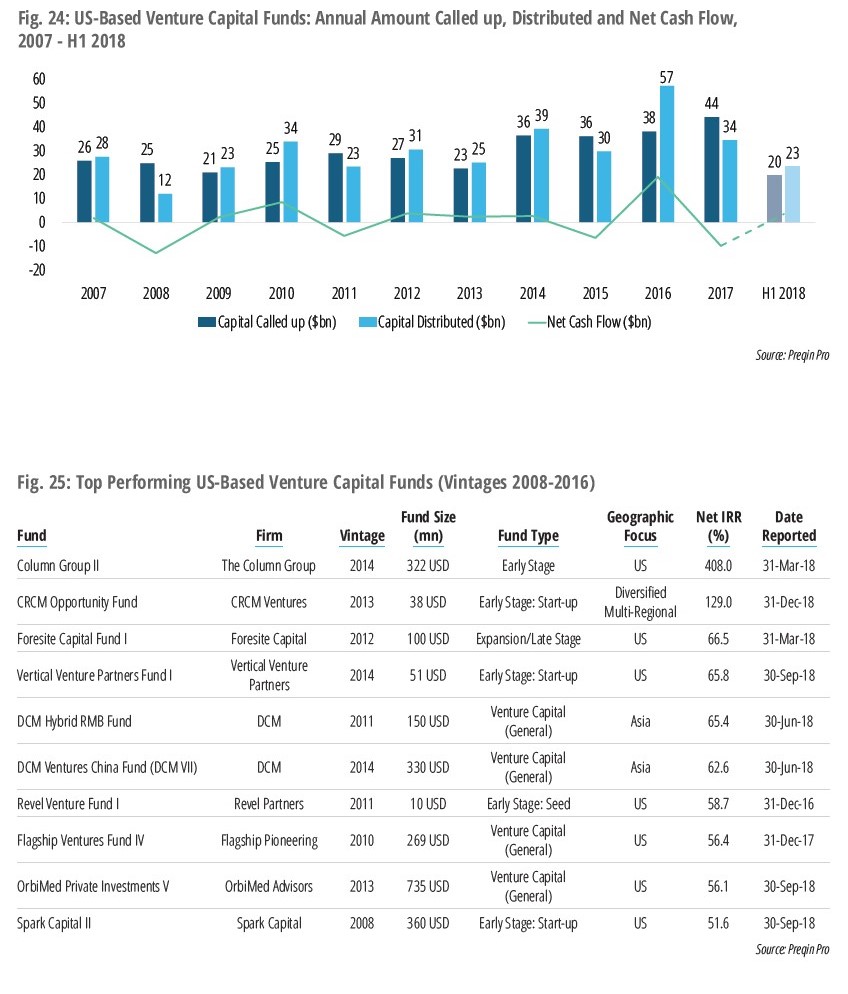

It has been a very strong decade of performance for US venture capital funds, and the home-runhitting nature of the asset class means that strong performance is clear at the very top. Column Group II leads the way for vintage 2008-2016 US-based venture capital funds, with a substantial net IRR of 408.0% (Fig. 25). The early-stage fund targets investments in the biotechnology industry and received commitments from Hartford HealthCare Pension and Endowment Fund, Regents of the University of California and Texas County & District Retirement System.

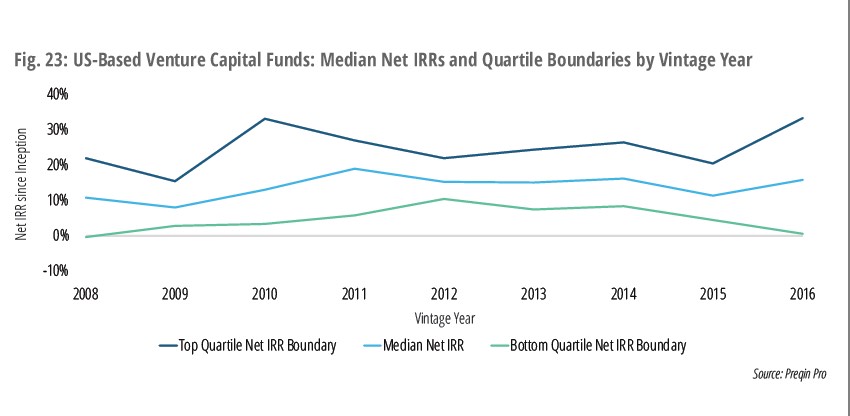

Returns in the venture capital industry typically range far across the size spectrum. Among the top seven performing US-based venture capital funds, four are micro venture capital, three are early-stage vehicles and one targets late-stage investments. US-based venture capital funds have performed well over the vintage range displayed in Fig. 23, consistently posting double-digit median net IRRs from vintage 2010 through 2016. This is a strong bounceback for the asset class since the Global Financial Crisis, with five of the available seven vintage years from 2010 onwards posting median IRRs upwards of 15%.

As a result of strong performance, venture capital managers have rewarded their investors with great liquidity over the past few years. In fact, US-based managers distributed a record $57bn in 2016, having called up only $38bn over the same period (Fig. 24). This marks one of seven years since 2007 in which venture capital has returned a positive cash flow to its investors, with average distributions of $34bn to LPs each year since 2010.

Fund Managers

The 10 largest US-based venture capital fund managers have collectively raised $73bn over the past 10 years (Fig. 24); eight of these fund managers are based in California and two are headquartered in New York. A new entry to this elite list is Technology Crossover Ventures, which leapt into seventh position thanks to its $3bn close on Technology Crossover Ventures X in January 2019.

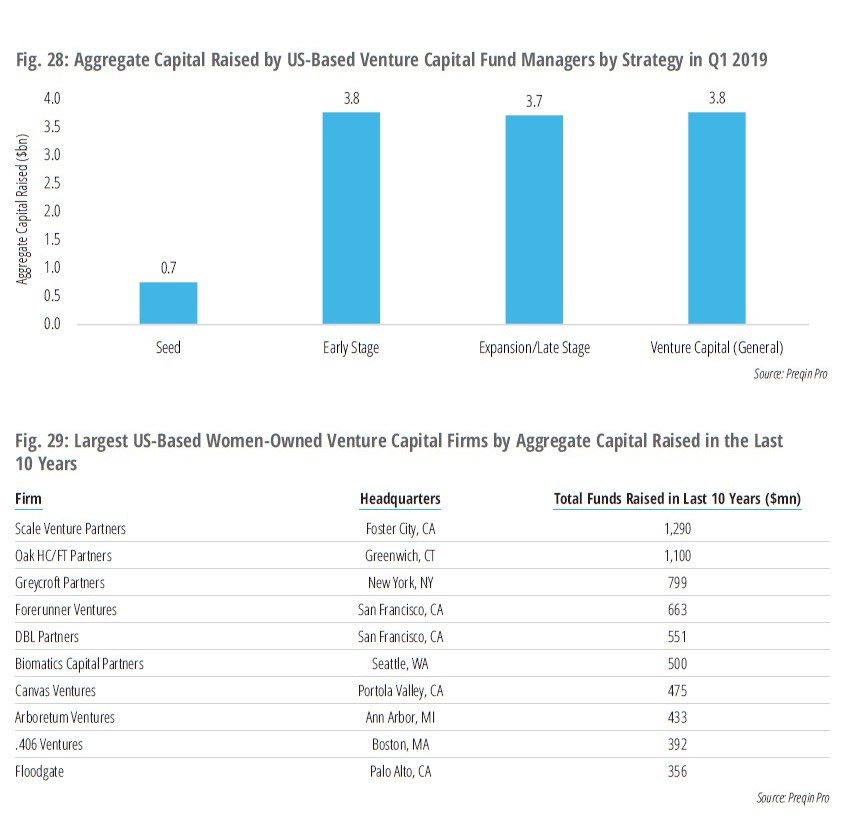

Although the top 10 US fund managers cover a range of investment stages, only Sequoia Capital and Bessemer Venture Partners have seed-stage-focused funds. This disparity is reflected in the aggregate capital raised in Q1 2019: just 6% of the $12bn raised is for seed investments, while the remaining 93% of capital is divided nearly equally among fundraising for early stage ($3.8bn), expansion ($3.7bn) and general venture capital ($3.8bn, Fig. 28). The $0.7bn raised for seed funds in Q1 2019 marks the largest proportion of quarterly funding these funds have ever received, four percentage points greater than the 2% recorded in 2014. US-based seed fundraising, the smallest capital market share, has raised $10bn over the past 10 years – a fraction of the $148bn that general venture capital funds have amassed since 2009.

New York-based Tiger Global Management is estimated to hold the largest amount of dry powder ($4.3bn) of all US-based venture capital firms (Fig. 27). The firm invests in both public and private markets across the globe, with its venture capital exploits focused on early-stage and growth investments across a range of sectors. In total, the top 10 firms account for over $28bn of venture capital dry powder as of April 2019.

US-based venture capital firms owned by women have raised $10bn over the past decade, $637mn of which is seed-stage capital. The top 10 US-based, women-owned firms have raised $6.6bn of the $10bn raised by such firms (Fig. 29), primarily through multistage and early stage strategies.

Expansion/late-stage funding reveals a gap not seen in the overall market. Although there is one expansion-stage fund currently on the road managed by a women-owned firm, Pear VC’s Pear Ventures I Expansion, no women-owned firm has closed an expansion-stage fund since StarVest Partners II’s $244mn close in 2009.of which is seed-stage capital. The top 10 US-based, women-owned firms have raised $6.6bn of the $10bn raised by such firms (Fig. 29), primarily through multistage and early stage strategies.

Expansion/late-stage funding reveals a gap not seen in the overall market. Although there is one expansion-stage fund currently on the road managed by a women-owned firm, Pear VC’s Pear Ventures I Expansion, no women-owned firm has closed an expansion-stage fund since StarVest Partners II’s $244mn close in 2009.

Investors

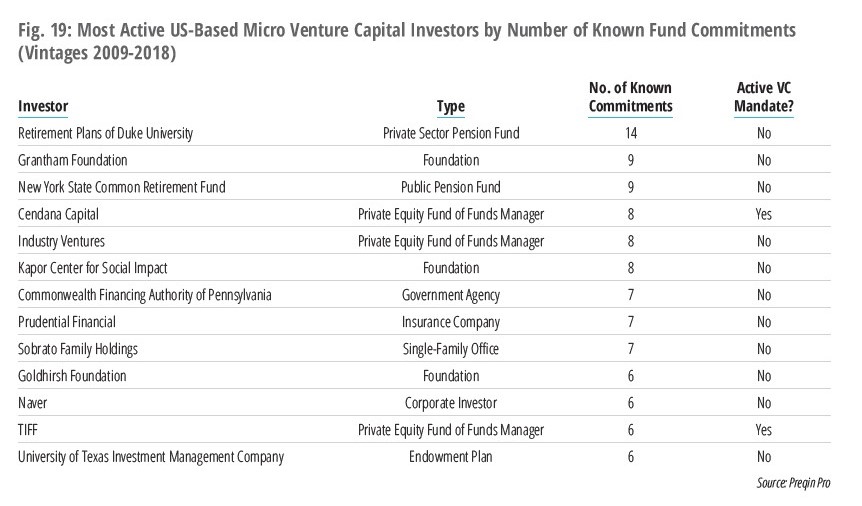

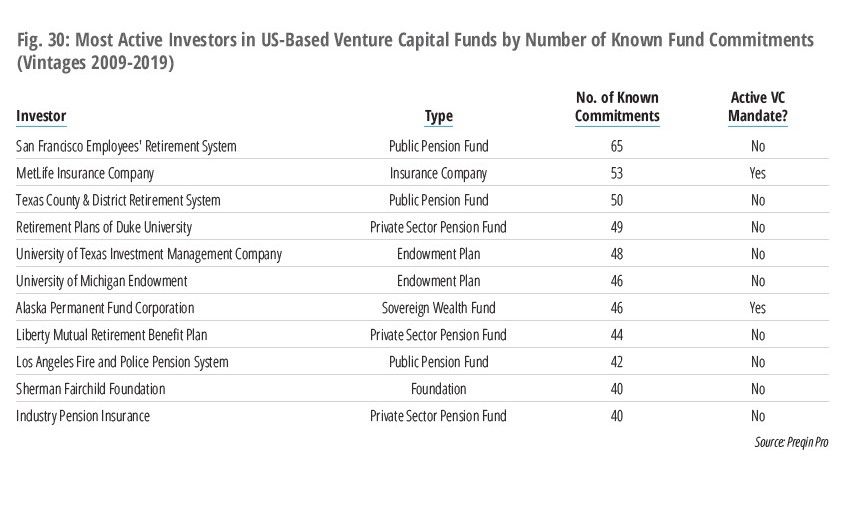

Six of the most active investors in US venture capital are pension funds, led by San Francisco Employees’ Retirement System which has 65 known commitments to vintage 2009-2019 venture capital funds (Fig. 30). The largest proportion of investors active in US-based micro venture capital funds, however, are

private equity fund of funds managers – tied with eight known commitments, Cendana Capital and Industry Ventures are the largest. Of all investor types with known commitments to US venture capital, foundations make up 19% of all investors and fund of funds managers just 8%.

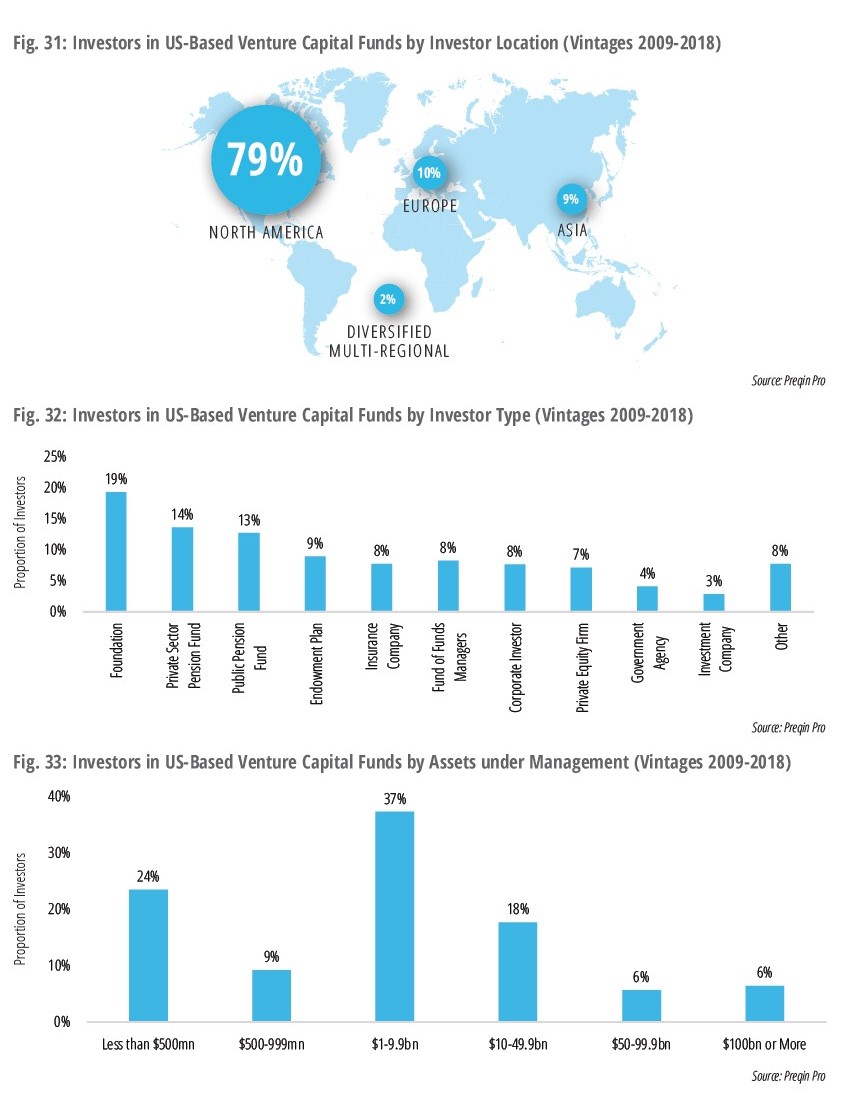

Over 15 different LP types commit to US-based venture capital funds of vintages 2009-2019; foundations account for the largest proportion (19%), followed by private sector (14%) and public pension funds (13%, Fig. 32).

As in Q4 2018, the majority (79%) of investors in US-based venture capital funds are located in North America (Fig. 31), which is no surprise given the historical preference for domestic venture capital managers among investors based in the region. This is followed by Europe (10%), Asia (9%) and Rest of World (2%). The majority (70%) of investors in US-based venture capital have less than $10bn in assets under management, with only 6% managing $100bn or more (Fig. 33). US-based venture capital firms continue to attract larger and more sophisticated investors compared to managers in other regions, reinforcing the strong preference for the market in North America.

Article by Preqin