This is a slightly technical post but highly relevant if you for certain types of businesses where leasing is prevalent.

Q3 hedge fund letters, conference, scoops etc

Come 2019, new accounting standards (specifically IFRS 16) will come into effect which will drive up the leverage ratios of businesses which have significant leases liabilities.

The new leases standard – IFRS 16 – will require companies to bring most leases on-balance sheet from 2019.

Explaining it in layman terms

Let us think about this in terms of you buying a car.

The normal route to buying a car would be for you to take a car loan.

You would take ownership of the asset in your name, and the corresponding debt to pay for it too.

The alternative way to do it is to lease it.

A lease is simply a contractual arrangement that allows the lessee (user) to pay the lessor (owner) for use of an asset.

You can think about it in terms of a renting a property.

You have certain ownership rights during the duration of your rental period, but the ultimate ownership (and risk that comes with owning it if money is borrowed to buy it) still lies in the landlord.

You have certain payment obligations during the duration of the lease. In the event you decide to terminate your contract early, there are still minimum payments that you have to make.

The key thing is that you are able to enjoy certain rights to the property for the duration of the lease without having to take on the risk of buying the property itself (and incurring the debt and corresponding asset).

What IFRS 16 does to leases

In the past, leases were “off balance sheet liabilities” and did not appear in the balance sheet itself. Information regarding lease commitments were found in the footnotes.

Off balance sheet liabilities have received much criticism over the years leading to new accounting rules to better reflect the true liabilities of a company.

The new change in accounting standard means that these lease commitments will now be moved onto the balance sheet and be recognized as liabilities.

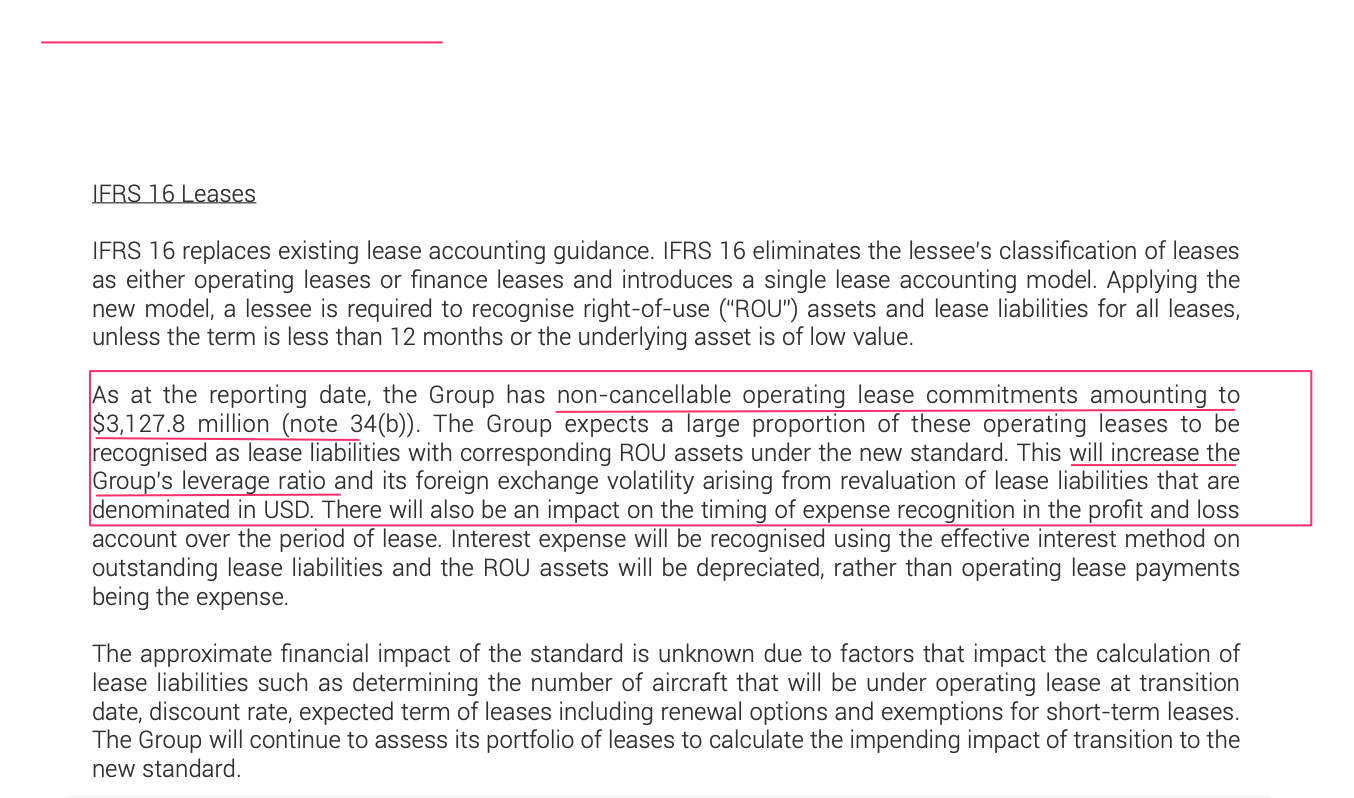

Singapore Airlines Annual Report FY 2017/2018

Of course, there will also be a corresponding increase in the asset column too (right of use of the asset – the aircraft).

The net result however is still that a lot of operating metrics will change because of the asset/liability changes.

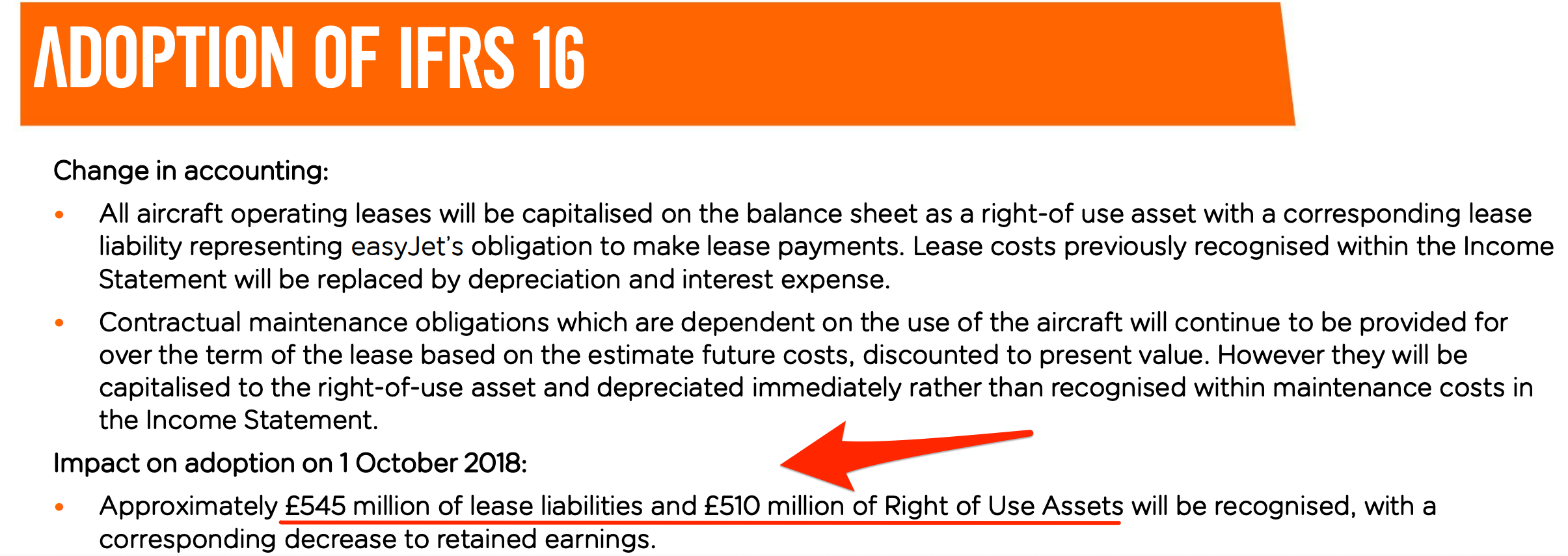

Easyjet (a budget airline in the UK) explained it pretty clearly and its good for comparative reasons.

Potential Fears

From a report by Deloitte, :

IFRS 16’s impact on gearing ratios could be particularly problematic.

While the new accounting will alter a host of key performance metrics, 63% of the wider aviation finance industry and, in particular, 69% of airlines are most concerned by changes to leverage ratios.

Airlines worry this might breach debt covenants, or increase borrowing costs. Almost half of survey respondents, including 61% of lessors, think that IFRS 16 raises the risk of covenant violations by airlines.

My suspicion

The subject of accounting standards and IFRS 16 are not something that gets a lot of attention (unsurprisingly), and a lot of investors are going to be quite surprised when these new accounting standards take effect.

Article by Jun Hao, The Asia Report