David Nadel discusses holdings in Japan, Australia, and the U.K. while offering his long-term perspectives for international small-caps and our Quality at a Reasonable Price (‘QARP’) approach.

Q3 hedge fund letters, conference, scoops etc

If you’re looking for value stocks, and exclusive access to value-focused hedge fund managers, check out ValueWalk’s exclusive value newsletter, Hidden Value Stocks.

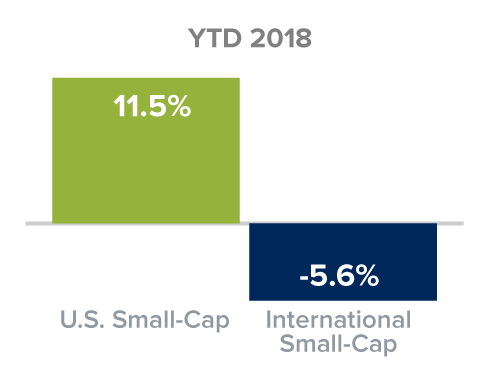

Why do you think 2018 has not been as strong as 2017 for international small-cap stocks?

I see three drivers of that. The first is U.S. dollar strength. The dollar’s been much stronger in 2018 than it was in 2017. Another is emerging market trends, which have been quite negative in 2018, both in terms of currency and in terms of their equities. A lot of negative volatility. And then a third I think is the rate cycle because the U.S. has gone ahead with tightening, and in the international markets, that’s probably still to come. So there is probably some concern, anticipatory concern, about a transition from a loosening cycle, quantitative easing, to a period where eventually rates will have to climb.

Shift in Relative Returns for International Small-Cap

Returns as of 9/30/18

“U.S. Small-Cap” is represented by the Russell 2000 Index and “International Small-Cap” by the Russell Global ex U.S. Small-Cap Index.

What’s your longer-term perspective on opportunities for non-U.S. equities?

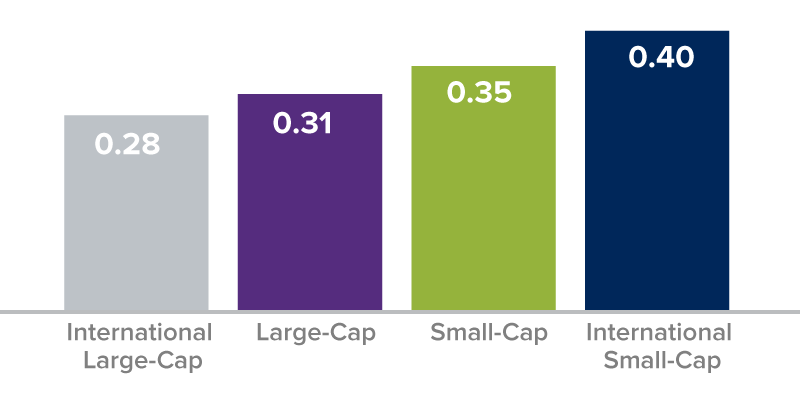

I think the longer-term outlook for international equities is much more positive. From a structural standpoint international small-cap, our research shows, offers the best Sharpe ratios, and the best absolute returns of any major equity asset class over rolling periods.

Averages of Monthly Rolling Annualized 10-Year Sharpe Ratio

From Russell Global Indexes First Full Month (Ended 7/31/96) through 9/30/18

“International Large-Cap” is represented by the Russell Global ex U.S. Large-Cap Index, “Large-Cap” by the Russell 1000 Index, “Small-Cap” by the Russell 2000 Index, and “International Small-Cap” by the Russell Global ex U.S. Small-Cap Index.

The Sharpe Ratio is calculated for a specified period by dividing a fund’s annualized excess returns by its annualized standard deviation. The higher the Sharpe ratio, the better the fund’s historical risk-adjusted performance.

So there’s a strong structural case for being exposed to international, and particularly international small-caps. Even that rate-tightening cycle could be quite positive for our type of companies because we focus on the higher-quality businesses, and as rates climb, a lot of those companies will most likely lose some of their competitors that are just hanging on by their fingernails due to these kind of artificially low rates in these markets.

What’s your outlook for Australia?

Australia’s an interesting example of finding an inefficiency in the marketplace, sort of a dislocation to get high quality companies at a reasonable price. And this is where the opportunities are being created for us, because the perception of Australia is it’s a natural resources-driven market, and also largely a play on China. Neither of those has been particularly positive in 2018, or really for even the last 18 months or so. So I think that has led to about a 10% reduction in the Australian dollar relative to the U.S. dollar. The opportunity that we get is we’re not really interested in natural resources-driven equities in Australia. We’re more interested in B-to-B service providers.

Australia Weighting Over the Last Four Quarters

% of Net Assets in International Premier

Securities are categorized by the country of their headquarters.

How are you addressing your U.K. holdings?

At the end of the quarter, we are actually showing the lowest U.K. weighting we’ve had in a long time. That is not really a function of top-down considerations. We have the same concerns about Brexit and the political environment there that anyone else would have. But those were really company-specific decisions to exit by the end of the first quarter. We had two companies that did somewhat dilutive share raises, followed on by some fairly, aggressive M&A that we didn’t really like, so we exited those positions. And so we find ourselves at a relatively low weight. But all of the companies that we invest in in the U.K. are multi-country revenue exposure. A few of them, at least, are global number ones in what they do. So this is, again, not a decision driven by a view on the U.K. economy.

U.K. Weighting Over the Last Four Quarters

% of Net Assets in International Premier

Securities are categorized by the country of their headquarters.

How do you see the Japanese markets currently?

Small-cap equities in Japan as a group are trading at four times net cash, so this is one of the best valuation opportunities out there. More importantly for us, though, the companies are producing very high returns on invested capital in sectors where we feel those returns are sustainable. So we have been adding positions in Japan, which directly mirror some European holdings. For example, Mark Rayner and I were in Japan last month; this was the second trip we took there this calendar year, we typically go a couple of times a year. And we added a position in the kind of asset-light warehouse automation space, which is very similar to a holding that we already had from Switzerland in the same business. Not uncommon for this strategy to invest in two companies in different geographies with a very similar business model. And it’s just refreshing to see that there are these high quality compounders in Japan; again, at valuations that are among the best in the world.

Japan Weighting Over the Last Four Quarters

% of Net Assets in International Premier

Securities are categorized by the country of their headquarters.

Article by Royce Funds