Will China and Russia create SWIFT equivalent?

SWIFT is an international settlement system, controlled by the United States. It is a kind of economic weapon that allows Americans to blackmail most countries. If cutting off from the system may force country to, for example, trade based on commodities.

Q1 hedge fund letters, conference, scoops etc

A few months ago, this U.S. dependence began to overwhelm European Union countries (Americans were imposing sanctions on Iran on that time). We wrote then that EU countries are considering creating system equivalent to SWIFT.

Now similar declarations were made after Russia’s and China’s leaders meeting. According to the note published after the meeting of Xi Jinping and Vladimir Putin, both countries focus on development of national payment systems which are to be compatible with each other and facilitate exchanges in rubles and yuan. One of examples of improvements would be introduction of UnionPay card payments in Russia and Mir in China (this change has been also mentioned in November by Dimitriy Medvedev).

As an explanation: Chinese UnionPay and Russian Mir are equivalents of Visa or Mastercard in these countries.

Compatibility of Russian and Chinese systems would mean minimizing the dollar role in trade between the two leading economies.

In his November speech, Medvedev also said that some of U.S. sanctions imposed on Russia mobilize his country to act “which should have been started 10 years ago”. He obviously meant working on his own payment system.

In fact, once again we write about countries working on their own payment systems, and at the same time it applies to countries that in some way have been affected by U.S. sanctions. In case of Europe, it was a ban on importing Iranian oil, while in case of Russia – direct sanctions burden by the U.S. maintained up to today. Will work on independent payment systems proceed? In case of Russia and China – we have no doubts about it. Situation of EU countries, which are much more dependent on the United States, looks a little worse.

Bonds are expensive, but …

Recent weeks have been fantastic in terms of U.S. bonds performance. Since the beginning of March, ETF giving exposure to long-term U.S. bonds has increased by over 10%. And this is an asset considered as relatively low volatile!

source: stockcharts.com

On the other hand, May was not that good for stocks. It could be concluded that in the following weeks shares should outperform expensive short-term bonds.

However, situation is not so simple. First of all, despite seemingly good situation (low unemployment, decent economic growth, shares close to their all time highs), almost whole market expects the Fed to lower interest rates. Where did such expectations come from? Economic downturn, which we have previously described on the example of Germany or China, is starting to overwhelm also United States. There are many indications that the last phase of the cycle is coming in which overheated economy sharply slows down, enterprises have worse results and scared investors choose safe bonds instead of risky stocks. Of course, trade war is also harmful, but it is only one part of the bigger picture.

If that was not enough, Fed decision may not change much. On the one hand, if the Fed cuts rates quickly enough, it may strengthen stock market for a while. Remember, however, that in case of the last two cycles, declines in stock market began at about the time when central bank cut interest rates for the first time in a long time. Simply, such a Fed decision can be treated as message saying: economy is not in the best condition.

On the other hand, if the Fed does not lower interest rates (it does not reduce credit cos), it will mean declines in the stock market, and some of panicked investors will shift to bonds.

Conclusions? Bonds are, in fact, short-term expensive and there may be correction in this market fairly soon, but there are many indications that it will be relatively small. The only scenario in which bonds will drop significantly, assumes following events:

- Fed lowers interest rates,

- markets react very optimistically, dollar begins to weaken,

- currencies of developing countries are gaining, stock markets and commodities rise,

- inflation is strongly increasing, which hits bonds.

What makes such scenario seem to be doubtful at the moment? This is the aforementioned economic downturn, which makes capital flow to the dollar instead of running away from it.

In our view, strong declines in the bond market will come, but only when the central banks announce large-scale monetary policy easing programs. We mean, among others, bringing interest rates below zero and money printing on huge scale.

ECB like a child in the fog

At the beginning, brief comparison between the European Central Bank and the Federal Reserve (i.e. U.S. Central Bank).

First of all, interest rates in the U.S. are 2.5%, while in Eurozone they are at 0%.

Secondly, ECB was purchasing government and corporate bonds till last December, artificially raising their prices. After the end of this program, another low-interest loans to enterprises were quickly announced. At that time, the Fed was doing the opposite – it has limited its balance sheet by getting rid of previously purchased assets.

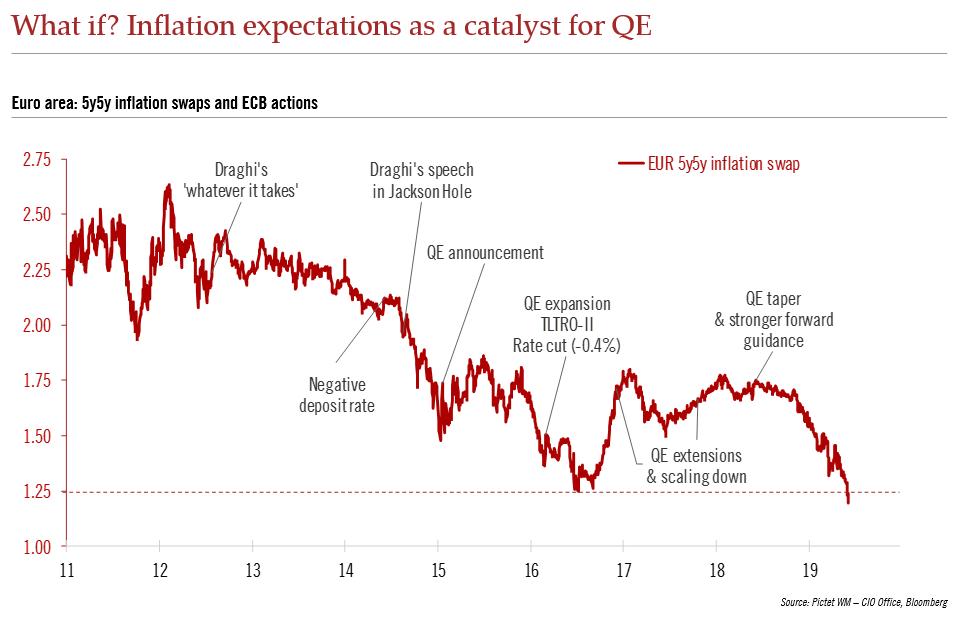

It would seem that in this situation the ECB’s policy is more conducive to high inflation. Meanwhile, it is completely the opposite. Both central banks set inflation at the level of 2% as the official target, but the ECB is significantly away from this goal. Indicator below reflects inflation expectations for euro area. As you can see, it is the lowest in history.

Today, it is 1.2%.

Over recent days, ECB members have tried to influence events with their statements. ECB President Mario Draghi mentioned that he intends to use all possible tools to achieve central bank’s goals. It has been announced that interest rates will not be raised for at least another year. Several ECB members even mentioned that there is a room for cuts.

Market reaction was negligible. Meanwhile, 8 years ago, similar words from Draghi caused a very rapid improvement of debt market (bankruptcy threat of several EU countries was calmed then).

What does this prove? Regardless of what central bankers tell in interviews, their tools are not able to stop natural cycles. The ECB can operate in various ways, but when facing recession it is powerless. What’s next? Most likely, deflationary trend will dominate for some time. What will happen later will depend on the tools used – if you will see programs based on “helicopter money” (currency given straight to citizens), deflation can turn into high inflation.

Either way, past weeks show ECB’s powerlessness. It is not a problem for Draghi, because his term is coming to an end in autumn. In turn, effects of its policy will be echoing in Europe for a very long time.

Italy: Will government tax wealth be kept in deposit boxes?

Italian government intends to tax cash and other valuable items kept in deposit boxes in banks. Idea was announced by Deputy Prime Minister Matteo Salvini. He admitted at the same time that government analyzes show that assets worth hundreds of billions of euros lie in these boxes.

Salvini also added that for people who disclose their assets themselves, lower tax rate will be applied. It would be 15 percent.

Present eurosceptic coalition ruling Italy is often portrayed (also by us) as a group of politically unstoppable rebels who are fighting for greater independence of the country. On the other hand, we have always emphasized that these people are populists who seriously consider ideas related to introduction of universal basic income. Such solutions obviously increase budget deficit. In case of Italy, problem is extremely serious, because the EU recently threatened to impose a fine due to excessive deficit. The fine would amount to 3 billion euros! Perhaps, this was one of the reasons why the Italian government began to think about where to get extra money.

The more countries with high deficits will be affected, the more often we will hear ideas about wealth tax. It is enough to mention that this type of tribute is promoted by, for example, the International Monetary Fund, which proposed introduction of 10% tax on assets.

It seems like in this way world wants to fight with the debt problem. Unfortunately, most forget that this problem was caused by conscious actions of central bankers (lowering interest rates) and politicians (borrowing at expense of the society in order to gain power).

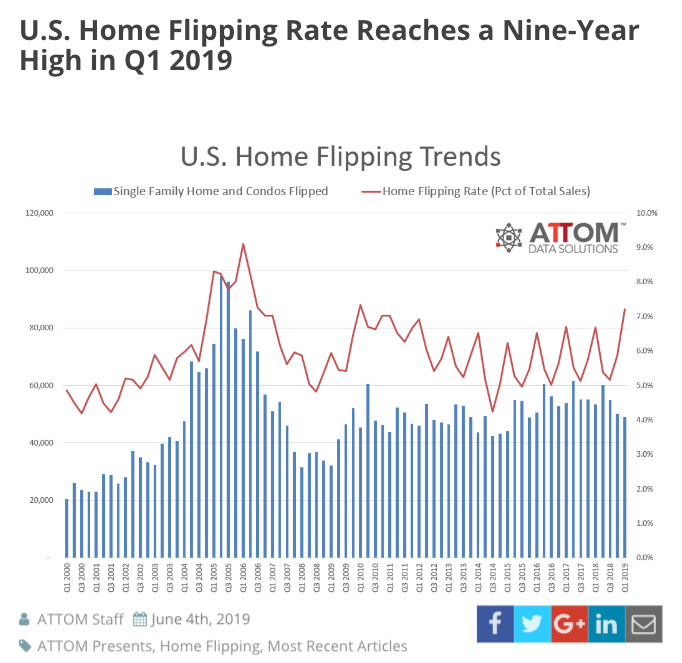

Peak on American flips?

Flips are the purchases of real estate, then making some changes (renovation, changing room configuration, etc.) and ultimately reselling at profit.

In the U.S. this type of activity is carried out on huge scale. Only over the first quarter of 2019, 49 thousand flips have been done, which correspond to 7.2% of total house sales. In this respect, market has reached highest level since the beginning of 2010.

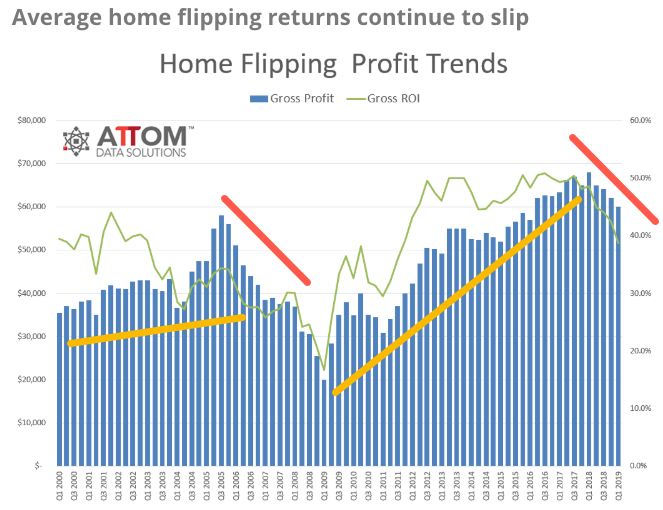

Remember, however, that a lot of interest in a given type of investment does not necessarily mean high profitability. American real estate market is the great confirmation of it.

Average gross profit from one flip in early 2019 (blue bars on chart below) dropped to 60,000 USD, which is the weakest result for 3 years. In percentages, the average rate of return from one flip in first quarter of 2019 amounted to 38.7%, while a quarter earlier it was 42.5%.

It seems that flips on the U.S. market are becoming less profitable. At the moment return on invested capital (green line above) is the lowest in many years. We are very curious about the next data release. On the one hand, real estate market may be favored by Fed interest rate cuts, and on the other hand weakening macroeconomic data definitely do not bode well for house prices.

Article by Independent Trader