- March 16, 2018

-

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Between yet another high-profile personnel shakeup at the White House and a nail-biter special election in Pennsylvania’s 18th Congressional District, not to mention Russia’s alleged nerve agent attack on a former double-agent spy and a tragic bridge collapse in Miami, this week has had no shortage of big splashy headline stories.

You can be forgiven, then, for missing what I believe is the most significant development of the past few days. On Wednesday, the Senate, in a bipartisan vote, quietly approved plans to roll back key banking rules in 2010’s Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank).

If the House also approves the bill, President Donald Trump is expected to sign it into law, thereby providing much-needed relief to smaller lenders and community banks that millions of rural Americans and small businesses depend on. Aside from tax reform, I think the relaxation of Dodd-Frank will be seen as Trump’s crowning fiscal achievement so far, as it has the potential to contribute greatly toward his goal of at least 3 percent economic growth.

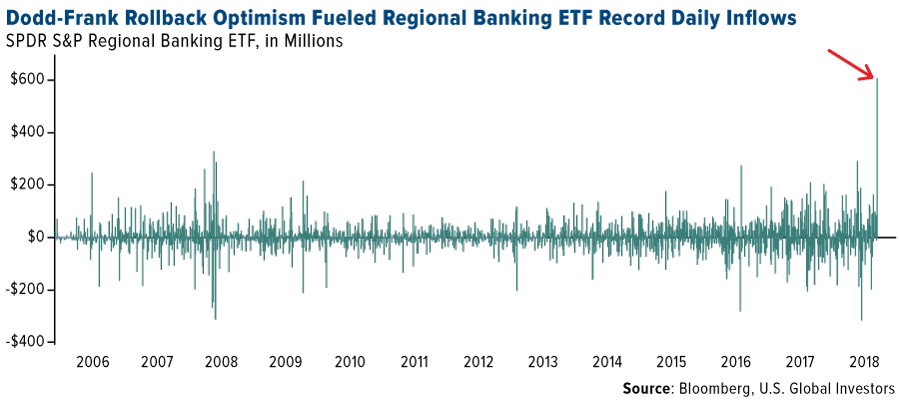

Investors piled into an ETF that holds small to midsize banks following the news this week. The SPDR S&P Regional Banking ETF attracted $606 million in daily inflows, a record for the fund, according to Bloomberg.

The most sweeping and complex financial reform package since the Great Depression, Dodd-Frank was drafted in response to the financial crisis—yet few believe it would do much in the way of preventing another such crisis. Last year, the Treasury Department declared that the law, despite its ambitious scale and scope, has “failed to address many drivers of the financial crisis, while adding new regulatory burdens.” As such, the agency recommended a number of changes, including improving efficiency and decreasing unnecessary complexity.

Among the likely changes to Dodd-Frank: raising the threshold for tougher oversight from the current $50 billion in assets to $250 billion; exempting small banks from the so-called Volcker rule, which currently bars them from speculative trading; reducing the amount of financial reporting, particularly racial and income data on mortgage holders; lowering the frequency of regulatory exams; and easing the conditions of stress tests.

Community Banks Are Vital to the U.S. Economy

The cumulative effect of the rollback will be to lower compliance costs and allow banks to better service clients and shareholders alike. I can’t stress enough how important this is. Small community banks—those with under $10 billion in assets—are tremendously vital to the U.S. economy. According to the American Enterprise Institute (AEI), they provide a substantial percentage of lending to U.S. farms—about 44 percent. Nearly half of all small business loans in the U.S., and more than 15 percent of all residential mortgages, are issued by small banks.

Last year, I included Dodd-Frank in a list of the five costliest financial regulations of the past 20 years. Since 2010, the legislation has undeniably had a negative effect on the banking industry, driving dozens of institutions to ruin and giving borrowers far fewer options. Between the year of its signing and 2014, the U.S. lost more than 14 percent of its small community banks, while the number of large banks rose 6.3 percent, according to the Mercatus Center at George Mason University.

Dodd-Frank Falling out of Favor

Support for Dodd-Frank is waning more and more. Both former Federal Reserve chair Alan Greenspan and billionaire investor Warren Buffett have come out strongly against it, with Greenspan saying he’d love to see the 2010 law “disappear.” For his part, Buffett believes that, as a result of the law, the U.S. is less well equipped to handle another financial crisis, as Dodd-Frank stripped the Fed of its ability to act.

Case in point: When now-defunct investment bank Bear Stearns was headed for failure 10 years ago this week, the Fed arranged an emergency loan of nearly $13 billion routed through JPMorgan. It also agreed to purchase $30 billion in Bear assets. But now, because of Dodd-Frank, such assistance is illegal since the law stipulates Fed lending must be broad-based and not directed toward a single institution.

Possibly the most telling sign that the 2010 law is losing favor among proponents is that Barney Frank himself, the former chairman of the House Financial Services Committee and one of Dodd-Frank’s chief architects, recently acknowledged he “sees areas where the law could be eased,” according to the Financial Times.

Speaking at this month’s annual Futures Industry Association meeting in Boca Raton, Florida, Frank said he “supports regulating banks differently based on their size” and sees the need to make it “easier for smaller banks to make loans such as mortgages.”

If you recall, lending procedures became so restrictive following Dodd-Frank that Ben Bernanke himself, Fed chair from 2006 to 2014, had trouble refinancing his home.

“I think it’s entirely possible [lenders] may have gone a little bit too far on mortgage credit conditions,” Bernanke said during a 2014 conference on housing.

More recently, President Trump claimed he had friends with “nice businesses” who couldn’t borrow money because of Dodd-Frank.

The easing of banking restrictions is just the latest in Trump’s ongoing effort to cut red tape that has stymied economic growth and disrupted the creation of capital. For many voters, his pledge to push for deregulation tops the list of reasons why he was elected, and I’m happy to see that he’s making good on this promise.

10 Years Since the Demise of Bear Stearns

The Senate’s approval to weaken Dodd-Frank comes, appropriately enough, on the 10-year anniversary of Bear Stearns’ stunning collapse. The once-powerful institution—in 2007 it was the fifth largest U.S. bank, with $400 billion in assets—was among the earliest warning signs of a broad economic meltdown that would ultimately result in the stock market losing nearly half its value. Below is just a sampling of headlines from 10 years ago this week:

As you’re no doubt aware, Bear Stearns’ demise was fueled primarily by excessive leveraging and overweight exposure to junk mortgage-backed securities. In an attempt to prevent the pathogen from spreading further, the Fed, as I mentioned earlier, brokered a deal for financial giant JPMorgan to buy Bear for as little as $2 a share.

We now know that the bailout provided only temporary relief. Six months later, Lehman Brothers, then valued at $691 billion, also fell victim to the subprime mortgage crisis. Today Lehman’s remains the largest bankruptcy filing in U.S. history.So what lessons can we take away from Bear? Countless articles and thought pieces have been written on this topic over the years, including an excellent one by Justin Baer and Ryan Tracy that appears this week in the Wall Street Journal.

Two lessons in particular stand out to me.

One, Bear showed us the painful consequences of failing to diversify. The bank had historically been known for its aggressive and risky investment strategies, but it was finally done in by its heavily concentrated position in bad mortgages. According to an analysis by former Lehman CFO Erin Callan, mortgage-backed securities accounted for a whopping 71 percent of Bear’s Level 3 assets—defined as those that are hard to value.

“Our liquidity position in the last 24 hours had significantly deteriorated,” announced Bear Stearns CEO Alan Schwartz, explaining to shareholders why he had no other choice than to accept an emergency bailout.

This is one of the many reasons why I recommend a 10 percent weighting in gold, one of the most liquid assets in the world. With 5 percent in gold bullion and 5 percent in gold mining stocks, along with an annual rebalancing, investors could potentially offset their losses in other holdings.

The second takeaway I’d like to point out is to focus on well-managed companies with healthy balance sheets. Near the end of its life, Bear Stearns was leveraged about 36-to-1, according to some estimates. For most firms, this is unsustainable.

Gold and the Global Ticking Debt Bomb

Unfortunately, corporate debt relative to U.S. GDP has now returned to prerecession levels, a risk made even riskier by rising interest rates. U.S. household debt, meanwhile, hit a new high of $13.15 trillion in the final quarter of 2017.

It’s for this reason that, when evaluating gold mining firms, we prefer those that do not rely primarily on debt to finance their operations. This recipe doesn’t always guarantee success, but should another financial meltdown occur, such companies will be in a much better position, financially, to weather the storm.

To learn more about what we look for in mining firms, click here!

![[thumb]](data:image/svg+xml,%3Csvg%20xmlns='http://www.w3.org/2000/svg'%20viewBox='0%200%2049%2049'%3E%3C/svg%3E)

March 14, 2018

The Many Uses of Gold

March 14, 2018

The Historic Bull Market Versus Steel Tariffs

March 12, 2018

The Historic Bull Market Faces Off Against Steel Tariffs

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.54 percent. The S&P 500 Stock Index fell 1.24 percent, while the Nasdaq Composite fell 1.04 percent. The Russell 2000 small capitalization index lost 0.69 percent this week.

- The Hang Seng Composite gained 1.68 percent this week; while Taiwan was up 1.50 percent and the KOSPI rose 1.40 percent.

- The 10-year Treasury bond yield fell 5 basis points to 2.84 percent.

Domestic Equity Market

Strengths

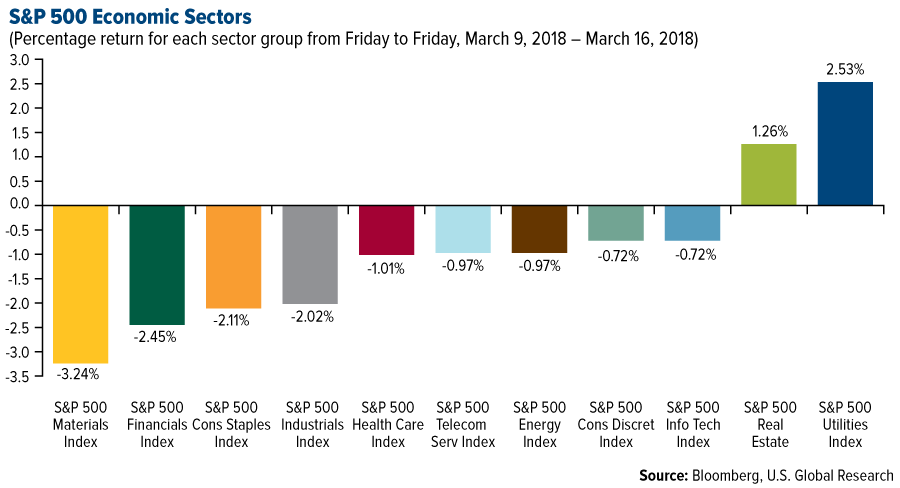

- Utilities was the best performing sector of the week, increasing by 2.53 percent versus an overall decrease of 1.10 percent for the S&P 500.

- Micron Technology was the best performing stock for the week, increasing 10.97 percent.

- Amazon’s TV shows brought 5 million people to its Prime subscription service in early 2017. This is the first indication to date of how successful the company’s TV offering has been at driving subscribers.

Weaknesses

- Materials was the worst performing sector for the week, decreasing 3.24 percent versus an overall decrease of 1.10 percent for the S&P 500.

- Signet Jewelers was the worst performing stock for the week, falling 20.86 percent.

- Signet Jewelers’ stock plunged on Wednesday after the company announced same-store sales fell again in fiscal year 2018, accelerating its decline from the prior year. Same-store sales across Signet’s chains dropped 5.3 percent for the year, after falling 1.9 percent in the prior year.

Opportunities

- The narrowing spread between short- and long-dated U.S. Treasuries has resumed this month after inflationary fears triggered a steepening of the yield curve in the February market rout. This bodes well for stock valuations and a continued risk rally, according to Evercore ISI’s Dennis DeBusschere. A flatter curve signals subdued economic volatility and muted premiums for price risk over the long haul, he wrote in a Wednesday note.

- Shares of Blue Apron spiked as much as 9.7 percent Thursday after CEO Brad Dickerson told The Wall Street Journal he planned to have meal kits in grocery stores this year.

- Paul Jacobs, the former chairman of Qualcomm, is looking to buy the company just days after President Donald Trump blocked Broadcom’s attempt to acquire it, according to the Financial Times.

Threats

- Treasury yields are reaching a point at which “bonds can challenge stock returns,” according to David Templeton, a money manager and principal at Horan Capital Advisors LLC. Templeton cited the gap between the yield on 10-year notes and the dividend yield on the S&P 500 Index, which topped one percentage point last month for the first time since January 2014. The potential for the spread to widen further “will serve as a headwind for stocks,” he wrote.

- Losses among U.S. stocks favored for their income are poised to widen as import tariffs spur inflation, according to Richard Bernstein, the founder and leader of Richard Bernstein Advisors LLC. He cited the S&P 500 Index’s real estate, telephone and utility stocks in a report Wednesday. “Income-oriented investors should be much more concerned about inflation than they are currently,” Bernstein wrote.

- The correlation between global equities and bonds is rising and recently hit its highest level in over a year. That trend can continue as economic growth peaks and central banks withdraw liquidity from the market, according to Societe Generale SA strategists. With the increase in lock-step moves, diversification will be harder to come by for fund managers and total portfolio returns could be harmed, they wrote in a recent report.

The Economy and Bond Market

Strengths

- Consumer sentiment in March unexpectedly jumped to a 14-year high after tax cuts boosted disposable incomes, while new tariffs boosted inflation expectations and dimmed the outlook, a University of Michigan survey showed. The sentiment index rose to 102 (estimated 99.3) from 99.7 in February.

- Home prices in the U.S. surged 8.8 percent in February, the biggest monthly gain in four years, as buyers battled for increasingly scarce homes. It was the seventy-second straight month of year-over-year increases since the market bottomed in 2012.

- The New York Empire State Manufacturing Survey headline index jumped to 22.5 (estimated 15) from 13.1 prior.

Weaknesses

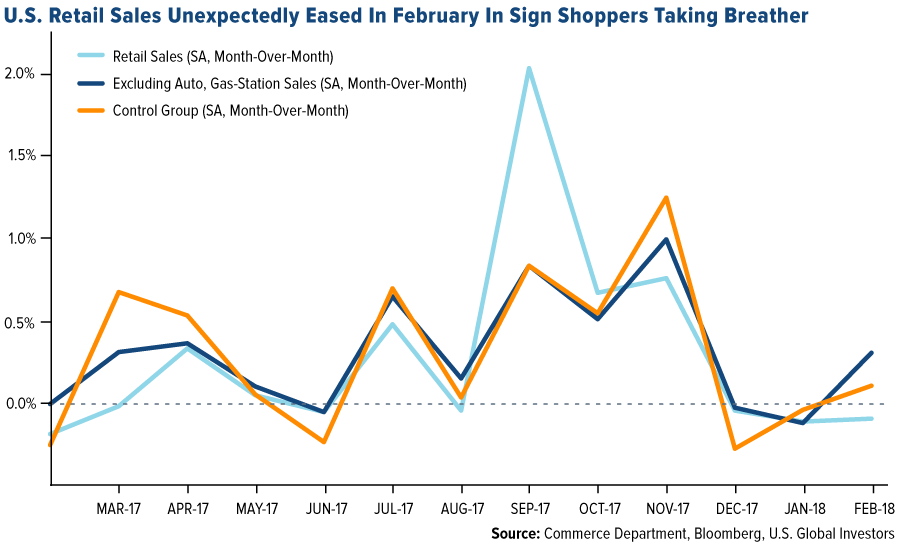

- U.S. retail sales unexpectedly fell in February for a third month, adding to signs that consumer spending is easing after strong gains in the fourth quarter. Overall sales fell 0.1 percent after a revised 0.1 percent decrease in January, and missed the median economist forecast for a 0.3 percent gain. Stripping out purchases at automobile dealers and gasoline stations, sales were up 0.3 percent, in line with estimates. So-called, retail-control group sales, used to calculate gross domestic product and which exclude food services, gasoline, building materials and motor vehicles, rose 0.1 percent, missing estimates for a 0.4 percent gain.

- U.S. new home construction cooled by more than expected in February on a reversal in the volatile multi-family category, government figures showed. Residential starts fell 7 percent to a 1.24 million annualized rate (estimated 1.29 million) after a 1.33 million pace previously. Single-family home starts rose 2.9 percent, while multi-family starts fell 26.1 percent. Building permits, a proxy for future home construction, fell 5.7 percent to a 1.3 million rate (estimated 1.32 million) from 1.38 million pace.

- The New York Fed’s GDP Nowcast model now sees U.S. first quarter GDP at 2.73 percent compared to 2.83 percent in the prior week. The Atlanta Fed’s model held at 1.8 percent. Further, the Philadelphia Fed Business Outlook Survey headline index fell to 22.3 (estimated 23) from 25.8 prior.

Opportunities

- U.S. housing data on Wednesday and Friday, and durable goods (Friday), will provide a read on how much the housing and capital spending sectors will add to growth this year.

- The nascent turn higher for Treasury bond futures is getting another leg of support from Bloomberg’s Fear/Greed indicator, a gauge of momentum and market sentiment. For the first time in about four months, it’s flashing a buy signal, a flip that follows similar guidance from the MACD indicator three weeks ago and as the 14-day relative strength index rebounds from its most oversold level in 14 months.

- The White House said Trump will campaign to pass legislation this year to upgrade roads, bridges and other public works, as members of Congress from both parties say it will only happen with funding and a push from the president. Trump plans to travel around the country to promote his proposal ahead of the congressional election in November, White House Legislative Affairs Director Marc Short said.

Threats

- Next week in the U.S. the focus will be on the FOMC meeting that will include a new projection for the economy and the policy rate. Investors will want to know how the FOMC’s forecast has changed post-tax cuts, and whether the slightly more hawkish tone by several policymakers will translate into a steeper ‘dot plot.’ A dot plot that is forecasting four rate hikes instead of the current three would catch the market by surprise.

- Political tension and conflict are a growing issue for investors, according to an index created by two Federal Reserve staff members. The Geopolitical Risk Index climbed this month to its highest since March 2003, when the U.S. invaded Iraq. The index is based on an analysis of news stories in the New York Times, Washington Post and Chicago Tribune.

- The German IFO (Thursday) and the Global ZEW indicator (Tuesday) are important bellwethers for global growth. There have been a scattering of indications recently that global growth may be coming off the boil, and both the Global ZEW and IFO dipped in their previous readings.

Gold Market

This week spot gold closed at $1,314.35 down $8.95 per ounce, or 0.68 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.77 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index closed up 0.58 percent. The U.S. Trade-Weighted Dollar Index moved higher by just 0.11 percent.

Date Event Survey Actual Prior Mar-13 CPI YoY 2.2% 2.2% 2.1% Mar-14 Germany CPI YoY 1.4% 1.4% 1.4% Mar-14 PPI Final Demand YoY 2.8% 2.8% 2.7% Mar-15 Initial Jobless Claims 228k 226k 230k Mar-16 Eurozone CPI Core YoY 1.0% 1.0% 1.0% Mar-16 Housing Starts 1290k 1236k 1329k Mar-20 Germany ZEW Survey Current Situation 90.0 — 92.3 Mar-20 Germany ZEW Survey Expectations 12.6 — 17.8 Mar-21 FOMC Rate Decision (Upper Band) 1.75% — 1.50% Mar-22 Initial Jobless Claims 225k — 226k Mar-23 Durable Goods Orders 1.6% — -3.6% Mar-23 New Home Sales 620k — 593k Strengths

- The best performing metal this week was palladium, down just 0.41 percent. Holdings in ETFs backed by palladium have fallen by two-thirds in the last three years and are back to 2010 levels. However, this is not the sign of a depressed market. Hedge funds have been taking delivery of the metal and then loan the metal to the market at lease rates of 6 percent for just one week, twice the yield they can earn from 10-year Treasury bonds. Money continued to pour into gold bullion ETFs this week, with $242 million of gains, compared with $35.2 million the previous week. Bloomberg reports inflation is gradually picking up, with U.S. consumer prices continuing firm in February. This could lead to a faster pace of interest rate hikes. Over the past three months, core inflation has increased at a rate of 3.1 percent. This is boosted by core goods, which is up 2.5 percent, after deflating for a majority of the past five years.

- Another indication of inflation rising is that TIPS, Treasury Inflation-Protected Securities, saw record inflows in February, a sign of anxiety in the bond market with large tax cuts signed into law in January. Inflation has historically benefitted the price of gold, with investors using it as a hedge against uncertainty. According to Bloomberg, U.S. retail sales fell in February for a third month in a row, raising some concerns on economic growth.

- Trader sentiment rose slightly this week after the dollar weakened following the news of U.S. Secretary of State Rex Tillerson’s sudden dismissal. A Russian cargo plane carrying precious metals accidentally spilled 3.4 tons of gold onto the runway when the hatch flew open during takeoff. Luckily, authorities were able to recover all 172 gold bars spilled and no one was hurt in the incident.

Weaknesses

- The worst performing metal this week was platinum, down 1.61 percent as hedge funds cut their bullish outlook with the net-long position the lowest in two months. Incoming White House economic adviser Larry Kudlow made remarks this week that sent gold toward a weekly decline while buoying the dollar, reports Bloomberg. Kudlow signaled that President Donald Trump would support a strong dollar, against some risk-off sentiment in markets amid growth concerns, the article continues. Gold could see further swings as the Federal Reserve is expected to raise interest rates when it meets next week.

- Gold gained as much as 4.7 percent in January, writes Bloomberg, but those gains have narrowed to less than 1 percent. With traders pricing in a 93-percent chance that the Fed will raise rates next week, demand for non-interest-bearing bullion is dampening. In a similar unenthused note from strategist Joni Teves at UBS, the group’s recent trip to Switzerland has revealed tepid gold interest there, according to a recent report. On one hand, Swiss gold investors acknowledge that the yellow metal remains a relevant diversifier and hedge against risks, but on the other hand the market “remains capped as there is no urgency to put on gold positions in the current macro environment,” Teves writes.

- The breach of a tailings damn wall at Newcrest Mining’s Cadia gold mine will affect the company’s performance for fiscal year 2018, reports Western Australia Today, sending shares of Newcrest down 5 percent on the news. The dam wall incident comes only weeks following a report that the company saw a 58-percent fall in underlying profit for the first half of fiscal year 2018. A range of factors have attributed to Newcrest’s numbers including “lower gold and copper sales volume,” along with an earthquake that affected the Cadia mine las year.

Opportunities

- Many signs are pointing to a weakening U.S. dollar, which has historically been good for the price of gold. According to Bloomberg Intelligence, the dollar is hitting lows that are lower than last year’s lows, despite a spike in rate-hike expectations. In speculating why the dollar is not appreciating, Bank Credit Analyst (BCA) writes that textbook economic models suggest a combination of import tariffs, expansionary fiscal policy and tightening monetary policy should create a bullish environment for the dollar. BCA also added that if the dollar continues to be used by the White House to shrink the deficient through protectionist trade policy, it would make dollar-based financial systems more unstable and dangerous. Chief Investment Officer of DoubleLine Capital, Jeffrey Gundlach, said during a webcast for his $51.8 billion bond fund that “the odds are good that the next big move in the dollar is lower.”

- Steven Englander, writing for Bloomberg, said this week that the Treasury is flooding the market with short-term debt that investors are not interested in buying. Englander reports that since August 2017, Treasury bills maturing in one year or less make up 63 percent of the increase in bills, notes and bonds, which is a massive skew. He says this is stealth intervention, where the U.S. dollar would need to weaken to create demand for the low-yield debt that is currently being issued with effectively negative interest rates.

- The copper supply may tighten this year, potentially leading to copper stocks performing well due to potential labor strikes at Chilean mines. In addition, the Democratic Republic of Congo signed a new mining code that raises royalties and taxes on mining companies, to as high as 10 percent, which would increase the cost of capital for new and existing projects in the mineral-rich nation.

Threats

- President Trump’s response to China’s unfair trading practices is taking shape, including measures limiting Chinese investments in the U.S. and annual tariffs exceeding $30 billion per year. This potential policy could have a negative impact on real estate. New York, the largest destination for foreign capital in the U.S., might receive the biggest impact with Chinese investment into U.S. office buildings decreasing around 30 percent last year.

- Bloomberg economists Jamie Murray and Tom Orlik write that if a global trade war begins, it could cost 0.5 percent of global GDP by 2020. Estimates show that if the U.S. raises import costs by 10 percent and the rest of the world retaliates by adding tariffs to U.S. goods, it could cost around $470 billion, with many countries suffering financially.

- Caveat Emptor: it’s a term used in the pink sheet market to issue a “Buyer Beware” warning to investors who might be enticed to buy these shares. We highlight this term because two news stories this week mention two separate companies that trade over-the-counter (OTC) in the U.S., each announcing a land acquisition that may contain in excess of $1 billion in precious metal value. Typically, these promotions rarely work out as favorably for the investor.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended March 16 was StrikeBitClub, which gained 206.88 percent.

- To help investors sift through the clutter, Thomson Reuters will begin tracking and analyzing bitcoin chatter across the web, writes Seeking Alpha. With help from MarketPsych Data, Reuters will scan over 400 websites as part of a new version of its MarketPsych Indices, to pick market-moving threads and transform them into a tradeable index, the article continues.

- According to Bloomberg, the biggest Indonesian platform to buy and sell digital currency may soon have more members than the nation’s century-old stock exchange. According to Indonesia Digital Asset Exchange’s CEO, the platform will have 1.5 million members buying and selling digital currencies by the end of 2018.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended March 16 was POLY AI, which lost 52.29 percent.

- Blockchain developer Ripple Labs lost its chance at having home-court advantage, reports Bloomberg, in a dispute with R3 Holdco. Ripple Labs was denied its bid by a San Francisco state appeals court, thus losing its bid in the dispute with R3. The dispute was over ownership rights to XRP, which was at one point worth over $16 billion.

- According to Allianz Global Investors, Bitcoin is “worthless” and the “bubble could pop soon,” reports Bloomberg. Even if blockchain technology can bring significant benefits to investors, the investment arm of Europe’s biggest insurer believes that the cryptocurrency is worthless.

Opportunities

- Ripple, which is the third most valuable cryptocurrency by market cap, announced the hiring of a chief market strategist to help “solidify the cryptocurrency in the minds of investors and potential customers,” reports Bitcoinist.com. Cory Johnson, who covered technology at Bloomberg for eight years, confirmed to CNBC that he has officially started working for Ripple last week.

- In an announcement on an official government website this week, China’s industry and IT ministry announced that it is working toward creating domestic standards to propel development and implementation of blockchain technology in the country. As CNN reports, the ministry revealed that it already conducted a “special study” to explore a framework for standardizing blockchain domestically.

- A cryptocurrency startup, TrueDigital, is chasing a cure for hacks, breakdowns and stolen funds, writes Bloomberg. The exchange has partnered with ConsenSys to create a reference rate for Ether – such benchmarks are a crucial step “because they supply the price reference traders use to calculate the value derivatives.”

Threats

- Following Facebook’s lead, Google will ban crypto-related advertising starting in June, reports Seeking Alpha. This includes ICOs, wallets and trading advice across any of its platforms. “We don’t have a crystal ball to know where the future is going to go with cryptocurrencies, but we’ve seen enough consumer harm or potential for consumer harm,” said Scott Spencer, Google’s director of sustainable ads.

- Elaine Ou, blockchain engineer at Global Financial Access, writes that Bitcoin is in the business of anarchy. She explains in an article for Bloomberg, that in Silicon Valley, “startups are urged to have a clear mission statement. If business lacks an explicit set of values to guide decisions, anarchy prevails.” However, although the idea that a $160 billion cryptocurrency is controlled by a software protocol running on autopilot is discomforting to some, Ou explains that, actually, sometimes it’s good to have no human governance. Her article is called “Bitcoin’s Anarchy Is a Feature, Not a Bug.”

- According to Reuters, a global regulatory crackdown on cryptocurrencies created by startups to finance new projects could slow the pace of virtual currency sales. Questions are mounting about their transparency and the risk of scams for investors. Although the rules are giving investors pause and delaying new offerings, some analysts are welcoming the respite. “We believe that regulation in the ICO space will filter out some of the nonsense in the marketplace and is part of the overall maturing of the crypto asset class,” Sam Lee, director of research at Strategic Coin said.

Energy and Natural Resources Market

Strengths

- Iron ore was the best performing major commodity this week rising 4.48 percent. The commodity rebounded from the lowest since November, as China’s top steel producing city plans to extend steel mill closures, which drive demand for higher grade, less polluting iron ore.

- The best performing sector this week was the S&P/TSX Diversified Metals & Mining Index. The index rose 4.75 percent as industrial metals outperformed on the back of strong China factory data, which posted better-than-expected results.

- The best performing stock for the week was Kingboard Laminates Ltd. The Chinese manufacturer of specialty chemicals rose 13.29 percent, a significant beneficiary of better-than-expected industrial data coming out of China this week.

Weaknesses

- Coal was the worst performing commodity this week. The commodity dropped 4.2 percent as Chinese producers warned of weaker sales volumes as China continues to focus on controlling air pollution.

- The worst performing sector this week was the S&P1500 Fertilizer and Agricultural Chemical Index. The index dropped 4.73 percent after its largest constituent, Monsanto Co., dropped on reports that the Department of Justice may impose additional hurdles before approving its proposed acquisition by Bayer AG.

- The worst performing stock for the week was Newcrest Mining Ltd. The largest Australian gold miner dropped 8.62 percent after part of a tailings dam collapsed at its Cadia mine. Cadia is one of Australia’s largest gold-mining operations and Newcrest was forced to halt production.

Opportunities

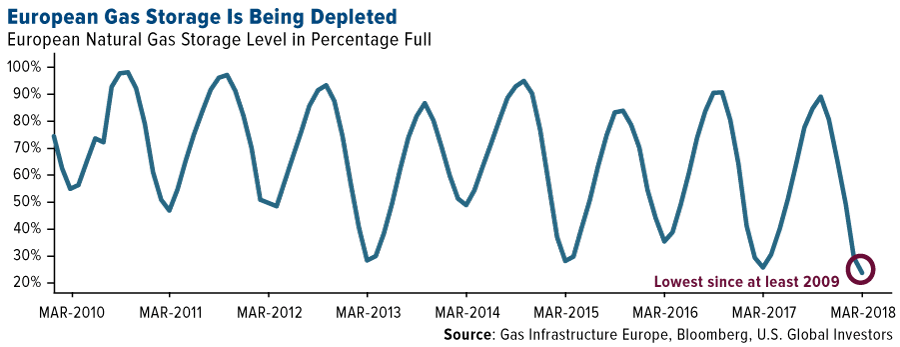

- European natural gas storage levels have dropped to the lowest level since at least 2009 before a wave of freezing weather is due later this week, increasing demand for the heating fuel, according to a Bloomberg report.

- The global oil demand will likely grow faster than expected this year, partly offsetting a surge in U.S. shale production and keeping the market in balance, the International Energy Agency said Thursday. The IEA predicted the world’s appetite for crude would increase by 1.5 million barrels a day to reach 99.3 million barrels a day in 2018, an upward revision of 90,000 barrels.

- Physical gold ETFs posted a spectacular increase in holdings this week as investors look for risk hedges. The GLD physical gold ETF added 4.4 tonnes of gold – valued at nearly $300 million – on a single day this week was the largest single addition in at least two months.

Threats

- Since its November monthly oil market report, OPEC has revised upwards its forecast of 2018 non-OPEC supply by almost 1 million barrels per day (b/d), from 58.54 million b/d to 59.53 million b/d. In its latest report, OPEC warned that non-OPEC supply “is now expected to grow at a faster pace” than initially expected, thus risking yet another oversupply imbalance in the global crude market.

- Bank of America warns of an imminent $5 per barrel correction in oil prices. “With speculative shorts already at a 15-year low, the positioning risk to the oil market is that some of the bears wake up from winter hibernation, if they do, WTI crude oil prices could lose $5/bbl within just a few weeks,” according to the bank’s analysts.

- February housing starts dropped 7 percent to 1.236 million, far below the 1.287 million rate expected after hitting its highest point in over a year in January.

China Region

Strengths

- Thailand and Vietnam put in particularly strong showings this week, with the SET Index up 2.15 percent and the Ho Chi Minh Stock Index up 2.39 percent.

- Information technology constituted the strongest-performing sector in the Hang Seng Composite Index for the week, climbing 3.25 percent. The HSCI finished up 1.68 percent over the last five trading days.

- China had a relatively light week of data, but the data came in reasonably strong, giving no indications of any immediate slowdown or concerns. Retail sales came in up 9.7 percent, ever so slightly shy of expectations for 9.8 percent. But industrial production came in at 7.2 percent year-over-year growth, handily beating expectations for a 6.2 percent showing, and FAI came in up 7.9 percent for the February period, well ahead of surveys anticipating a 7.0 percent print.

Weaknesses

- Domestic vehicle sales for the February period in Vietnam fell to a five year low, declining by 28.8 percent, a significant drop from the prior reading’s gain of 29.4 percent.

- Malaysia’s year-over-year industrial production numbers for the January period rose only 3.0 percent, shy of expectations for a gain of 6.8 percent, and just barely up from the prior month’s 2.9 percent reading.

- Retail sales in Singapore fell 5.4 percent month-over-month for the January period, and 8.4 percent year-over-year. Both numbers missed analysts’ expectations.

Opportunities

- China is giving power to its central bank to write the rules for the financial sector, reports Bloomberg. The move comes as a sweeping overhaul aimed at “closing regulatory loopholes and curbing risk in the $43 trillion banking and insurance industries.” Caixin announced the plans to merge the banking regulators (CBRC) with the insurance regulators (CIRC) to form a new agency called the China Banking and Insurance Regulatory Commission (CBIRC). As Bloomberg highlighted, “the pace of financial reform is quickening.” Separately, Agricultural Bank of China Ltd. announced a share sale to shore up capital, signaling that the process of bolstering state-owned lenders is also underway.

- “China’s top steel-making city is imposing further production cuts beyond the winter heating season,” Bloomberg reports of Tangshan, “as the nation presses ahead with a campaign for cleaner skies.” The move affects less than 1 percent of current national capacity but nonetheless “signals the government’s intent to prioritize clean air over industrial output,” the article argues.

- The announcement of a formal summit between the United States and North Korea represents some form of opportunity, though not a necessarily riskless sort of opportunity. One can be optimistic, though. It remains difficult to imagine an incredibly thorny issue getting all packaged up cleanly in any sort of hasty manner, but hey, who knows? Maybe we’ll get the announcement via Twitter.

Threats

- Rex Tillerson’s removal from office as U.S. Secretary of State by President Donald Trump came at roughly the same time as the administration’s formal announcement of an upcoming U.S.-North Korea summit. Curiously, Tillerson is one who had been, at least publicly, a firm proponent of talking with North Korea. It is uncertain what exact complications his removal will have on the trajectory and direction of any forthcoming talks.

- Hong Kong is reportedly considering taxing vacant housing, according to Bloomberg News, in efforts presumably aimed at curbing the pace of price increases. Hong Kong’s vacant housing is estimated to be about 3 percent.

- Concerns over tariffs and/or trade wars remain relevant.

Emerging Europe

Strengths

- Romania was the best performing country this week, gaining 4 percent. The Bucharest stock exchange was supported by banks. BRD Groupe Societe Generale gained 9.2 percent in the past five days, followed by 8.5 percent gain in Banca Transilvania. Banca Transilviania received the necessary approval from the National Bank of Romania for the acquisition of shares held by Eurobank Group in Bancpost.

- The Hungarian forint was the best performing currency this week, gaining 10 basis points against the U.S. dollar. The Budapest stock exchange was closed Thursday and Friday in celebration of the 1848 uprising against Habsburg rule. A “peace march” was organized in the country’s capital, during which Victor Orban has warned “countries that do not stop immigration will be lost.” Hungary will hold parliamentary elections in three weeks.

- Information technology was the best performing sector among eastern European markets this week.

Weaknesses

- Poland was the worst performing country this week, losing 2.8 percent. February inflation decelerated to 1.4 percent year-over-year from 1.9 percent in January, well below the forecasted CPI reading of 1.8 percent. It fell below the bottom end of the National Bank of Poland’s fluctuation band of +/- 1 percent around its target of 2.5 percent. Food and fuel prices dropped the most.

- The Turkish lira was the worst performing currency this week, losing 2.8 percent. The currency depreciated each day this week, heading for its longest losing streak in almost five months, following a credit downgrade last week and a slew of disappointing economic data.

- Industrials was the worst performing sector among eastern European markets this week.

Opportunities

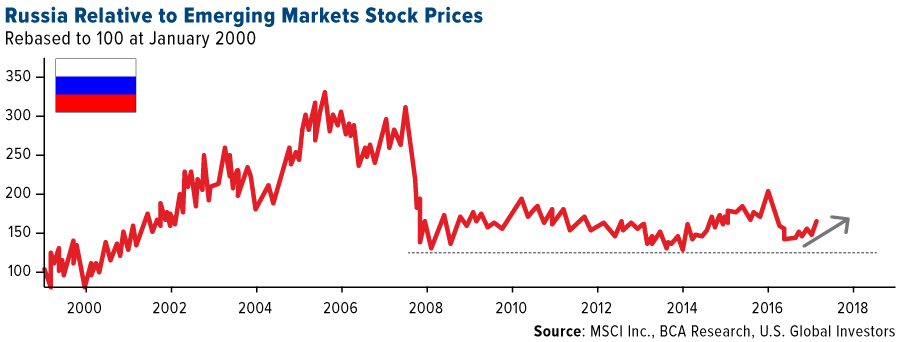

- BCA Research has a positive view on Russia, saying that the country has tight and conservative fiscal policy, slightly letting the nominal expenditures to grow since the oil crash while spending has fallen considerably, improving the fiscal deficit. Moreover, the central bank of Russia has refrained from injecting excess liquidity into the banking system and has marinated high real interest rates. Per the chart below, Russian stocks are making a major bottom formation relative to the emerging market benchmark and should outperform in the coming year.

- European Central Bank (ECB) President Mario Draghi said recently at a conference that he wants to see sustained adjustment in inflation’s path toward a target of 2 percent being met, in order for the quantitative easing (QE) program to end. He argued that euro strength could weigh on inflation down the line, and the performance of underlying inflation remains subdued versus previous recoveries. On Friday, final February inflation was reported at 1.1 percent year-over-year versus prior 1.2 percent. The low inflation reading means the ECB will likely be slow to change its bond-buying program quickly.

- Fitch Ratings expects the Polish economy to grow by 3.9 percent in 2018 compared with the 3.6 percent pace it forecast in December, Polish state news agency PAP cites Fitch saying in a statement.

Threats

- Prime Minister Theresa May ordered the expulsion of 23 Russian diplomats in retaliation for the poisoning, on British soil, of a former spy and his daughter with nerve agent, escalating tensions between Vladimir Putin and the West. May said the U.K. will move to freeze Russian state assets where necessary in response to what she said was an “unlawful use of force” by Russia against the U.K. The threat of more sanctions imposed on Russia by Western Europe and the U.S. is still in the air.

- The U.K.’s largest lenders face tougher capital demands in this year’s stress test, as the Bank of England steps up efforts to avert a repeat of the financial crisis, according to Bloomberg’s Daily Briefs. Banks will be held to a single capital standard that includes their minimum capital requirements. Previously, only such a change applied to the world’s biggest lenders was factored in.

- Russia will hold presidential elections this Sunday, and Vladimir Putin will most likely win the next term, but two important factors may emerge from the voting results. First of all, we can see how Crimea voted. According to Putin, the annexation of Crimea was supported by its people. Secondly, Putin wants a 70 percent turnout with 70 percent voting for him. Low turnout will be seen as a negative surprise.

Leaders and Laggards

Weekly Performance Index Close Weekly

Change($)Weekly

Change(%)Russell 2000 1,586.05 -11.09 -0.69% S&P Basic Materials 370.81 -12.30 -3.21% Nasdaq 7,481.99 -78.82 -1.04% Hang Seng Composite Index 4,370.62 +72.28 +1.68% S&P 500 2,752.01 -34.56 -1.24% Gold Futures 1,313.60 -10.40 -0.79% Korean KOSPI Index 2,493.97 +34.52 +1.40% DJIA 24,946.51 -389.23 -1.54% S&P/TSX Global Gold Index 183.94 +3.89 +2.16% SS&P/TSX Venture Index 833.67 +4.77 +0.58% XAU 78.70 -0.20 -0.25% S&P Energy 497.93 -4.25 -0.85% Oil Futures 62.18 +0.14 +0.23% 10-Yr Treasury Bond 2.84 -0.05 -1.76% Natural Gas Futures 2.70 -0.04 -1.32% Monthly Performance Index Close Monthly

Change($)Monthly

Change(%)Korean KOSPI Index 2,493.97 +72.14 +2.98% Hang Seng Composite Index 4,370.62 +156.91 +3.72% Nasdaq 7,481.99 +338.37 +4.74% XAU 78.70 -6.80 -7.95% S&P/TSX Global Gold Index 183.94 -7.64 -3.99% Gold Futures 1,313.60 -44.40 -3.27% S&P 500 2,752.01 +53.38 +1.98% S&P Basic Materials 370.81 -6.69 -1.77% DJIA 24,946.51 +53.02 +0.21% Russell 2000 1,586.05 +63.95 +4.20% SS&P/TSX Venture Index 833.67 -2.50 -0.30% Oil Futures 62.18 +1.58 +2.61% S&P Energy 497.93 -5.96 -1.18% Natural Gas Futures 2.70 +0.11 +4.21% 10-Yr Treasury Bond 2.84 -0.06 -2.03% Quarterly Performance Index Close Quarterly

Change($)Quarterly

Change(%)Korean KOSPI Index 2,493.97 +11.90 +0.48% Hang Seng Composite Index 4,370.62 +389.84 +9.79% Nasdaq 7,481.99 +545.41 +7.86% Natural Gas Futures 2.70 +0.08 +3.22% Gold Futures 1,313.60 +51.60 +4.09% S&P 500 2,752.01 +76.20 +2.85% S&P Basic Materials 370.81 +0.34 +0.09% S&P/TSX Global Gold Index 183.94 -4.83 -2.56% XAU 78.70 -1.53 -1.91% DJIA 24,946.51 +294.77 +1.20% Russell 2000 1,586.05 +55.62 +3.63% SS&P/TSX Venture Index 833.67 +32.44 +4.05% S&P Energy 497.93 -11.31 -2.22% Oil Futures 62.18 +4.88 +8.52% 10-Yr Treasury Bond 2.84 +0.49 +20.82% U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2017):

Tahoe Resources Inc

Cardinal Resources Ltd

Leagold Mining Corp

Victoria Gold Corp

OSISKO GOLD ROYALTIES LTD

Gold Fields Ltd

Geely Automobile Holdings Ltd*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell ®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.The Bloomberg Dollar Spot Index (BBDXY) tracks the performance of a basket of 10 leading global currencies versus the U.S. Dollar. S&P/TSX Capped Diversified Metals and Mining Index is an index of companies engaged in diversified production or extraction of metals and minerals. The S&P 1500 Supercomposite is a broad-based capitalization-weighted index of 1500 U.S. companies and is comprised of the S&P 400, S&P 500, and the S&P 600. The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money. The Empire State Manufacturing Index is an index based on the monthly survey of manufacturers in New York State conducted by the Federal Reserve Bank of New York. The index summarizes general business conditions in New York State. The Philadelphia Federal Index is a regional federal-reserve-bank index measuring changes in business growth. The index is constructed from a survey of participants who voluntarily answer questions regarding the direction of change in their overall business activities. The survey is a measure of regional manufacturing growth. When the index is above 0 it indicates factory-sector growth, and when below 0 indicates contraction. Also known as the “Business Outlook Survey”. ZEW Germany Expectation of Economic Growth is a survey on the question of economic growth in six months. Bloomberg’s Fear/Greed Indicator is an oscillator based on the ratio of buying strength to selling strength. The Geopolitical Risk Index counts the occurrence of words related to geopolitical tensions in 11 leading international newspapers. Diversification does not protect an investor from market risks and does not assure a profit. The SET Index is a Thai composite stock market indexwhich is calculated from the prices of all common stocks (including unit trusts of property funds) on the main board of the Stock Exchange of Thailand (SET), except for stocks that have been suspended for more than one year. The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange. The index was created with a base index value of 100 as of July 28, 2000.