FORECASTS & TRENDS E-LETTER

by Gary D. Halbert

May 1, 2018

1. GDP Growth Slowed in 1Q, But Beat Expectations

2. US Businesses Raise Pay at Fastest Pace in 11 Years

3. Fed Meeting Today, Tomorrow – No Rate Hike Expected

4. What You Should Know About the Flattening Yield Curve

5. The Most Interesting Political Article I Read Recently

[timeless]

Q1 hedge fund letters, conference, scoops etc

Overview

We touch on several bases today, starting with last Friday’s initial estimate of 1Q GDP, which was lower than the pace of growth in the 4Q but above the pre-report consensus. From there, we look at private-sector wages which rose by the most in 11 years in the 1Q – a nice surprise.

The Fed’s monetary policy committee is meeting today and tomorrow, and the question is whether there will be two or three more interest rate hikes this year. I’ll give you my thoughts. Next, we’ll take a look at the flattening yield curve and whether or not we should be worried about it.

And finally, I’ll share the most interesting political article I have read recently. Let’s jump in.

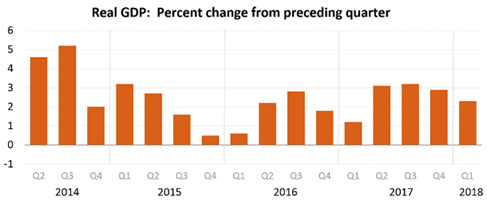

GDP Growth Slowed in 1Q, But Beat Expectations

The US economy slowed in the 1Q as consumer spending grew at its weakest pace in nearly five years. Gross Domestic Product increased at a 2.3% annual rate, the Commerce Department reported Friday in its initial estimate of 1Q GDP. Growth was also held back by a moderation in business spending on equipment and investment in homebuilding.

Despite that, the advance estimate of 2.3% was actually better than the pre-report consensus of 2.0%, but it was below the 2.9% GDP growth in the 4Q of last year. The 1Q GDP estimate tends to come in on the low side due to seasonal adjustments, but at least it was better than the 1.2% reading in 1Q 2017 and 0.6% in 1Q 2016.

Growth in consumer spending, which accounts for more than two-thirds of US economic activity, slowed to a 1.1% rate in the 1Q. That was the slowest pace since the 2Q of 2013 and followed the 4Q’s robust 4.0% rate. Consumer spending in the 1Q was undercut by a decline in purchases of motor vehicles, clothing and footwear, as well as a slowdown in food and beverage expenditures.

According to surveys, the Trump tax cuts were not reflected in many workers’ paychecks until late in the 1Q. Given that, the effects of the tax cuts are more likely to show up in the 2Q and beyond. Also, we know that many households are using the tax cuts to boost savings.

Business spending on equipment slowed to a 4.7% rate in the January-March quarter after double-digit growth in the second half of 2017. The cooling in equipment investment partly reflects a fading boost from a recovery in commodity prices.

Investment in homebuilding was unchanged in the first three months of the year, reflecting an acute shortage of properties that hurt home sales. Residential construction increased at a blistering 12.8% rate in the 4Q of last year.

Government spending grew at a 1.2% annual rate in the 1Q, slowing from the 4Q’s 3.0% pace. Federal spending is expected to accelerate in the 2Q since the US Congress recently approved more government spending.

Economists expect growth will accelerate in the 2Q and the second half of this year as the labor market is near full employment and both business and consumer confidence are strong. Lower corporate and individual tax rates, as well as increased government spending, will likely lift annual economic growth to the administration’s 3% target just ahead.

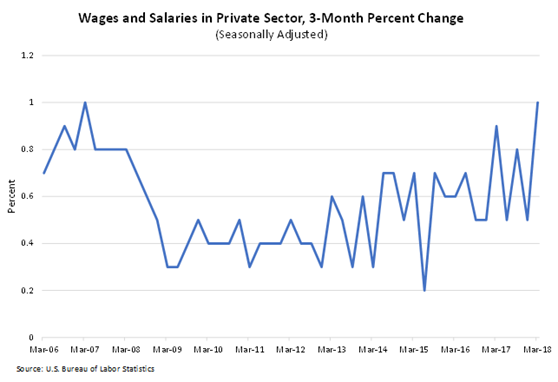

US Businesses Raise Pay at Fastest Pace in 11 Years

US private-sector workers received the biggest pay raise in 11 years in the first three months of the year, a sign that the tight job market is finally lifting wages.

The Labor Department reported Friday that its Employment Cost Index shows wages and salaries in the private sector rose almost 1% between January and March compared with the previous quarter. That’s the largest gain since the 1Q of 2007 before the Great Recession began.

The gain was boosted in part by healthy year-end commissions that are typically paid to sales workers at the beginning of the year. The increase may also reflect other one-time factors such as bonuses paid out after the Trump administration’s corporate tax cut took effect.

In the past year, wages for private sector workers rose 2.9%, the healthiest increase since the 3Q of 2008. By comparison, wages for private sector workers rose at about a 3.5% annual pace in 2007, before the recession hit.

The Employment Cost Index measures healthcare and other benefits as well as pay. Overall compensation for US workers rose 2.7% in the 1Q from a year earlier. That is also the fastest gain since the 3Q of 2008. Wages and salaries make up about 70% of total compensation, and benefits comprise the other 30%.

Other measures of pay have also risen, but at a choppier pace. Average hourly pay as measured in the monthly jobs report has increased 2.7% in the past year.

The unemployment rate is currently at a 17-year low of 4.1% and employers are hiring vigorously. Many businesses are struggling to find qualified workers and they’re offering higher pay as a result.

Forecasters worry that stronger pay gains could add to inflationary pressure on the US economy. Yet the Consumer Price Index fell 0.1% in March and was up 2.4% for the 12 months ended March. Higher inflation may be coming at some point but it does not seem to be a significant problem for now.

Fed Meeting Today, Tomorrow – No Rate Hike Expected

The Fed Open Market Committee (FOMC) which sets monetary policy is meeting today and tomorrow. In March, the FOMC raised the short-term Fed Funds rate by 0.25% to a range of 1.50%-1.75% as was widely expected.

It is not expected that the FOMC will hike the Fed Funds rate at this week’s gathering largely because there is no press conference following this meeting. It is more likely that the FOMC will hike the rate at the next meeting scheduled for June 12-13 when a press conference will follow. The press conferences allow the Fed Chair to explain the reasoning whenever there is a change in interest rates.

The thinking among most Fed-watchers is that the Committee will raise the rate at the June meeting and again in either September or December, for a total of three rate hikes this year. There has been speculation since Jerome Powell replaced Janet Yellen as the new Fed Chairman that he may be considering four rate hikes this year.

The minutes of the March 20-21 meeting published on April 11 did not indicate that the Committee specifically discussed a fourth rate hike this year. Rather, the Committee maintained its usual language that the number of rate hikes will be determined by the economy and inflation.

Speaking of inflation, the Personal Consumption Expenditures Index (PCE) rose to 2% for March, up from 1.7% in February. Core PCE (less food and energy) rose to 1.9% in March from 1.6% in February. Core PCE is the Fed’s preferred measure of inflation.

It will be interesting to see if tomorrow’s policy statement addresses the fact that 1Q GDP came in at 2.3%, down from 2.9% in the 4Q. I rather doubt that will have much influence on the Fed’s interest rate intentions, especially since the GDP data will be revised two more times just ahead.

What You Should Know About the Flattening Yield Curve

There has been increasing concern in the financial media about the fact that the yield curve – the spread between shorter-term Treasury notes and longer-term Treasury bonds – has been narrowing over the last several years. There are even fears that the yield curve could “invert” with short-term rates rising above long-term rates later this year – which historically has been a precursor to recessions. I don’t share those concerns at this point.

A meaningful discussion of the yield curve and its implications for the economy is way too complicated to get into in the limited space I have left today. But since the topic is on many investors’ minds currently, here is a good article on the topic from Liz Ann Sonders of Charles Schwab. She explains it as well as I could and makes some interesting observations:

What You Should Know About the Flattening Yield Curve

There is another very good article on the flattening yield curve by Barry Ritholtz in SPECIAL ARTICLES below.

The Most Interesting Article I Read Recently

As most of my clients and readers know, the mainstream media is on a dedicated mission to get rid of President Trump. They are convinced that he colluded with the Russians to rig the election in his favor over Hillary Clinton. They despise him! Yet so far, they have failed miserably in their mission.

The following article offers a completely different view and one that may surprise you. I won’t summarize it; you need to read it for yourself. One warning, however: If you are a big fan of Hillary and Bill Clinton, you probably don’t want to read this article. Otherwise, dig in!

What Did the Media Know and How Long Have They Known It?

All the best,

Gary D. Halbert

SPECIAL ARTICLES

US Growth Cools to 2.3% While Wages Accelerate

Don’t Freak Out About the Flattening Yield Curve

Gary’s Between the Lines Blog: Americans Are Fleeing High-Tax States in Droves