“The greatest mistake of the individual investor is to think that a market that did well is a good market rather than a more expensive market.”

“Volatility is an instrument of truth, and the more you deny the truth, the more the truth will find you through volatility.”

– Chris Cole

“The most important rule is to play great defense, not great offense. Every day I assume every position I have is wrong. I know where my stop risk points are going to be. I do that so I can define my maximum drawdown. Hopefully, I spend the rest of the day enjoying positions that are going in my direction. If they are going against me, then I have a game plan for getting out.”

– Paul Tudor Jones

A lot happened this week as I’m sure you are well aware. The market reacted negatively Wednesday to Fed Chairman Jerome Powell’s assessment that the economy is strengthening and inflation could be gaining strength. Treasuries fell hard, as 10-year yield broke back above the 2.90 level. Risks: Inflation and higher interest rates…

The next day, the Bank Of Japan’s Haruhiko Kuroda said during his confirmation hearing for another term as central bank governor, “The BOJ will start thinking about how to exit its massive monetary stimulus program in around the fiscal year starting in April 2019.” Risks: Testing the end of the massive quantitative easing experiment… unquantifiable… yet unknown.

And the European Central Bank is debating how to exit its own stimulus program. Bundesbank Governor Jens Weidmann told Bloomberg this week that quantitative easing could end this year. Risks: The big three exiting QE – at the same time. Record gloval indebtedness…higher rates…not good. Like periods past, rising rates may likely lead us into recession. But wait, there’s more…

Yesterday afternoon, President Trump’s pledge to impose stiff tariffs on steel (25%) and aluminum imports (10%) sparked trade-war worries, sent stocks tumbling, triggered protests from American industries and lawmakers on Capitol Hill and prompted threats of retaliation across the world. Risks: Trade wars, price inflation, global slowdown, stagflation and recession.

Another major development, in my view, are the rumors of Gary Cohn’s departure from the White House. Cohn, the President’s chief economic advisor, opposed the tariffs and raised his concerns with the President. Trump called it a “small price to pay” and stuck by his trade promises despite Cohn’s advice. I’m hoping the rumors are not true.

On the surface, one might think this is no big deal; however, when you understand how the economic machine works, you begin to see how inter-connected and co-dependent we all are within a broad and competitive system. Protectionism and trade wars drives a wedge into the system. Beer, auto and boat makers worried about costlier aluminum and manufacturers of chemicals, air conditioners and oil pipelines concerned about pricier steel denounced the moves. China has found a newly opened window to pick a fight with U.S. farmers. Trade wars ripple. Economic madness.

Last summer, BMW, the German automaker said it will add another 1,000 jobs and invest $600 million in its South Carolina plant as part of a plan to boost annual production to as many as 450,000 vehicles. Move that plant back home? North Carolina has been courting Toyota and Mazda to come to the U.S. This is just one industry. Good for U.S. steel makers but bad for a lot of other industries.

The 737 airplane is made up of 367,000 parts and is assembled at a factory in Renton, Washington, south of Seattle. To build the plane, Boeing relies on a complex web of hundreds of suppliers providing everything from engines and fuselages to seats and exit signs.

Faster, cheaper, better… we benefit. To appeal to the airlines that buy their planes, and compete with Airbus, Boeing has not hesitated to outsource when there may be a cost savings. In doing so, the company is heavily dependent on international suppliers. Among major suppliers, China’s Xian Aircraft Co. makes the 737 vertical fins and Japan’s Mitsubishi Heavy Industries provides the wing’s inboard flaps. Add to the complex web, the number of companies outside the U.S. that supply parts needed to make the GE jet engine that GE sells to Boeing. Ok, you get the point.

Business arrangements are not going to go away quickly. Result, the higher prices will pass through to you and me. A jolt to the system. This from Martin Armstrong,

“The big problem is that Trump FAILS to understand how the economy truly functions. Imposing tariffs on foreign imports because they can produce something more efficiently is NOT protecting American jobs – it is imposing higher costs on the American public. If America cannot compete against foreign steel and aluminum, the answer is not tariffs, but TAX REFORM and UNION REFORM.”

Yes, one can argue that Trump is getting back at countries that impose tariffs on us. The great negotiator? A match that ignites a global trade war.

Bottom line: I’ve been reporting that global growth is solid. But way up there on my risk list is trade wars/protectionism. The big guy is throwing a giant monkey wrench into the spokes of the global economic system. This move may, and I’ll bet will, quicken the path to the next recession.

To which, Bridgewater Associates founder, Ray Dalio, sees 70% chance of recession before 2020. Amen, brother Ray.

“I think we are in a pre-bubble stage that could go into a bubble stage,” the hedge fund manager said during an appearance at Harvard Kennedy School’s Institute of Politics on Wednesday, according to a Reuters report. Source MarketWatch.

Dalio said investors should not panic and need to have a sound plan. If people become scared after the market has tumbled, it is too late, Dalio said, adding that people should probably buy when they are frightened and sell when they are not.

“The greatest mistake of the individual investor is to think that a market that did well is a good market rather than a more expensive market,” he said.

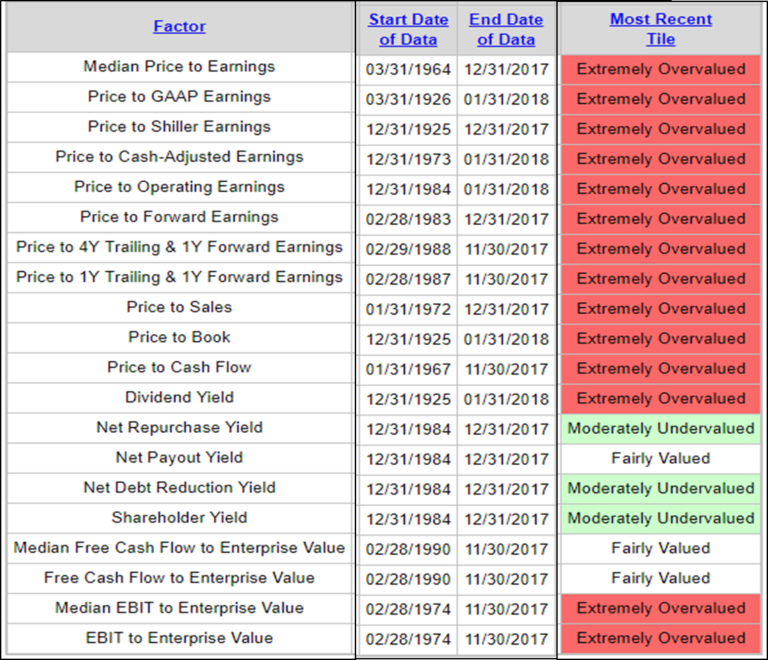

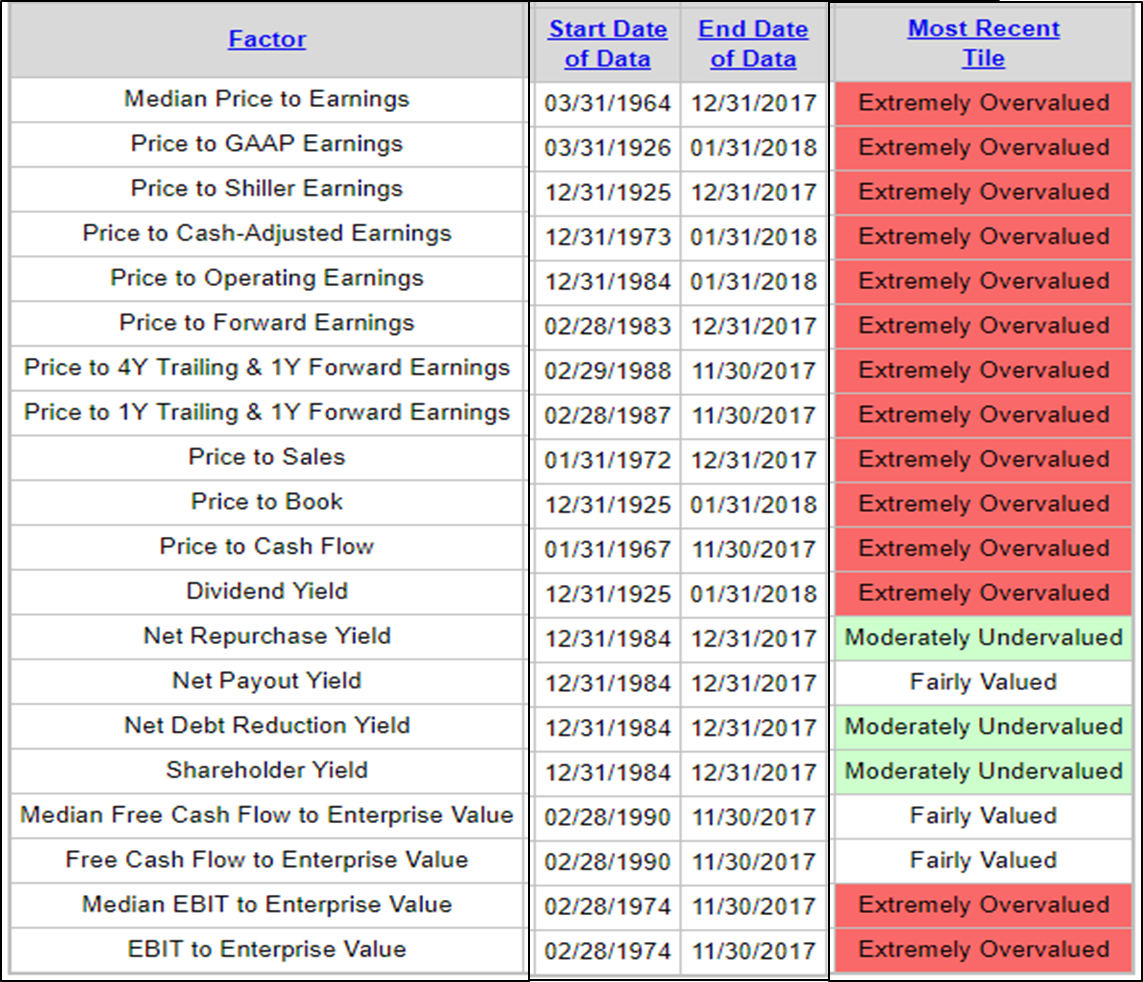

Speaking of more expensive, I’ll be presenting next week in San Antonio and San Diego on “Equity Market Valuations and What They Tell Us About Probable 7-, 10- and 12-Year Returns.” Essentially storying through the charts I shared with you in a recent On My Radar letter (here).

Here is a quick look at the summary of various valuation measures (note a lot of red):

Recently, I received an email from a reader noting that valuations are really not that stretched when you view them relative to low interest rates. I have a great deal of data on what current valuations predict in terms of forward returns but frankly I don’t have relative to interest rates valuation data in terms of forward returns. I’m going to dig in on that project, but I suspect; however, that all assets are priced off of the risk free rate and if the risk free rate is rising, then the relative interest rate argument quickly runs into trouble.

What I do know is the historical correlation with current valuations and subsequent 10-year returns is just way too high a correlation for us to ignore. And the ‘relative to low interest rates’ argument has problems kick in when interest rates rise.

Fed Chairman Powell is hinting to four more rate increases this year. Those inflation concerns are leading to higher interest rate concerns. We may be looking at 3.50% to 4% 10-year yields this year. And the ECB and the BOJ are hinting to a change of course. Rising rates are a risk, trade wars/protectionism is a risk and there are, of course, geopolitical risks.

Frankly, I’d feel a lot better about equities if their current valuations weren’t high. Risk is high because valuations are high. Future returns are low because valuations are high. See here for the most recent forward return estimates.

The next three charts are a quick summary of probable seven and ten year equity market returns:

Send me a note if you’d like a deeper explanation on the above charts.

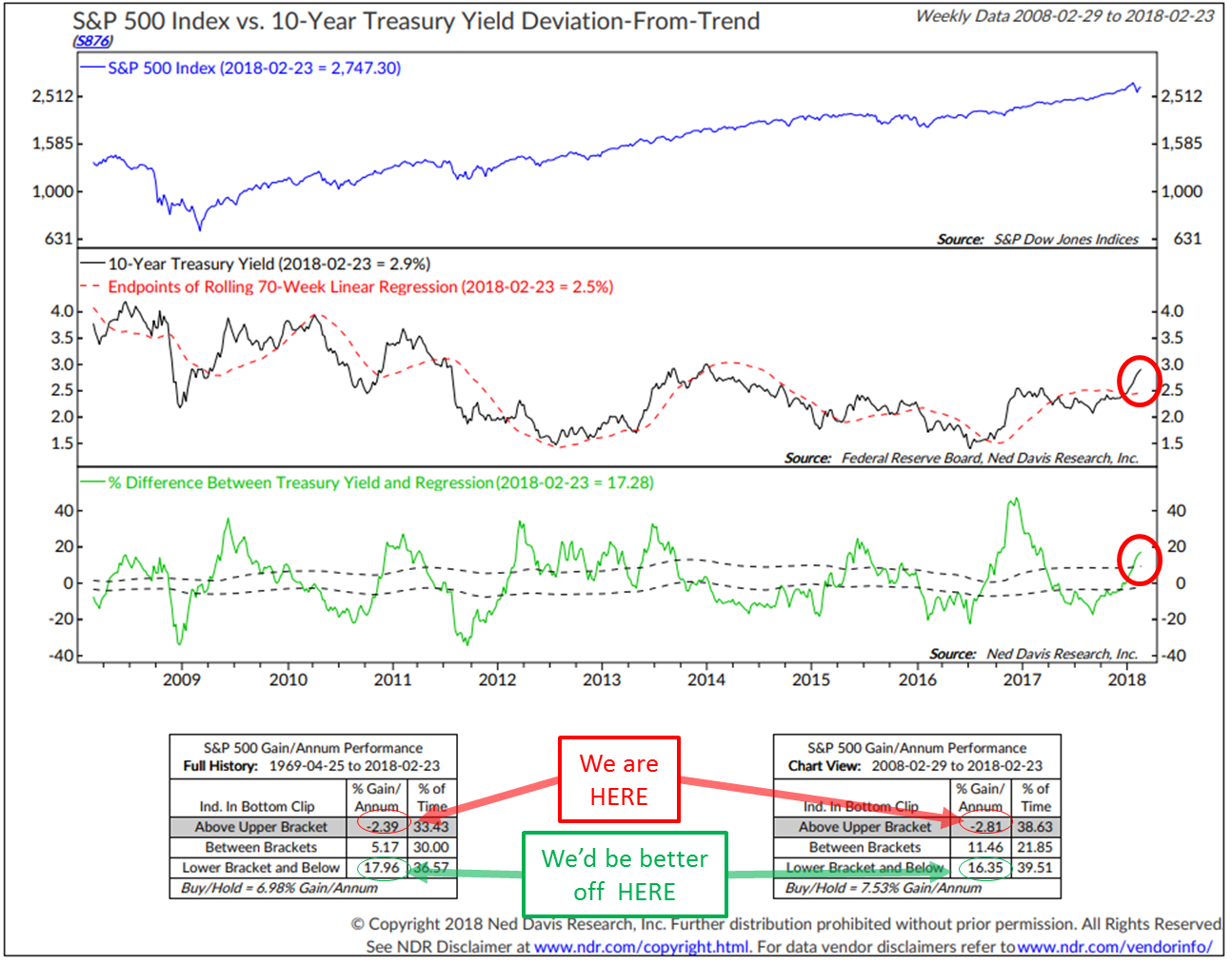

Finally, let’s take a look at the interest rate problem. I’ll be sharing the following chart in my presentations next week. It simply measures the intermediate term trend in interest rates and the impact that rising rates have on stocks. Note the return for the S&P 500 when rates are rising (the “We Are Here” arrows). Also note the “We’d be better off Here” arrows. Data is from 1969 to present and 2008 to present.

Let’s keep our eye on this as time moves forward.

“The moment of truth has arrived for [the] secular bond bull market!

[Bonds] need to start rallying effective immediately or obituaries need to be written.”

—Jeffrey Gundlach

Rates were 2.55% on the 10-year when I quoted Gundlach in OMR on January 12, 2018 (see, The Moment of Truth for the Secular Bull Market in Bonds has Arrived). Then, the intermediate trend in interest rates was neutral. Rates are now another 30 bps higher since then and the trend is now negative.

It will be rising rates that drive us into the next recession. Ray Dalio’s 70% chance of recession before 2020 makes sense to me. I’ll share my favorite recession probability charts with you next week, along with some of my notes from the Mauldin Economics 15th Annual Strategic Investment Conference. It is the best conference I attend each year. Looking forward to learning more…

Grab a coffee and find your favorite chair. Click through and you’ll find an interesting take on corporate buybacks (they’ve been big and likely some more gas left in the buying tank) and the “end of the low volatility regime” along with the latest Trade Signals. And despite the tone of risk shared with you above, the trend in equities remains bullish (weakening but bullish). Keep Paul Tudor Jones’s “have a game plan for getting out” advice front of mind. Key words – game plan.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- The end of the low volatility regime (continued): Why buybacks are a clear and present danger to the anomalous market they helped fuel

- Trade Signals — Bullish Equity Trend Rolls On; Fixed Income Signals Remain Bearish

- Personal Note

Why buybacks are a clear and present danger to the anomalous market they helped fuel

“Volatility is an instrument of truth, and the more you deny the truth, the more the truth will find you through volatility.”

– Chris Cole

Unfortunately, this cartoon seems all too apropos today.

I shared with you a link to Chris Cole’s October article on Volatility. If you missed it you can find it here. So when I came across the following article, it caught my eye enough to share it with you today:

As Artemis Capital’s Chris Cole told The New York Times in September: “Volatility is an instrument of truth, and the more you deny the truth, the more the truth will find you through volatility.” Over the past decade, there has been no corporate instrument of mistruth more powerful than buybacks, an issue we have dissected in these pages for years. U.S. firms have spent roughly $4 trillion on buybacks since 2009, making corporations the biggest single source of demand for U.S. shares. According to Artemis’s calculations, buybacks have “accounted for +40% of the total earnings-per-share growth since 2009, and an astounding +72% of the earnings growth since 2012.”

No doubt there is a clear bull case for why buybacks could prove the savior, rather than the Achilles’ heel of U.S. equity markets this year. With the new tax law reducing liabilities and incentivizing repatriation, buybacks are already on record pace — $171 billion worth have been announced so far in 2018, more than double the amount disclosed by mid-February 2017.If a tax-bill-fueled buyback bonanza can effectively “buy the dips”, market tranquility can be protected, preventing a large-scale unwinding of low-volatility-pegged strategies.

However, this optimism neglects the threats facing the buyback-industrial-complex. A political backlash against buybacks is intensifying as the tax bill manifests — since passage, total buybacks announced exceed worker bonuses and raises by roughly 63x. Yet, even if political concern doesn’t materialize into action, a more systemic problem remains: rising interest rates combined with the toxic mix of corporate inequality and debt.

According to an IMF estimate from last spring: “Large U.S. corporations have experienced a negative net equity issuance of $3 trillion since 2009 due to share buybacks.” U.S. corporate debt — piled on by both strong and weak hands — sits at an all-time high of $13.7 trillion. Meanwhile, the tax bill will disproportionately benefit the strong hands — for one, the richest 10% of companies control 80% of the $1 trillion offshore cash hoard. Begging the pressing question: As the cost of debt goes up, can the buyback spending of the strong offset the turbulence caused by the weak?

Buybacks have been essential fuel for the low-volatility regime, enabling steady equity appreciation and in turn, the rules-based strategies pegged to that tranquility. Now, as volatility returns to equity markets, buybacks will likely prove key to understanding and anticipating the threat of a high-volatility crash.

The past two weeks have offered a clear illustration of the importance of buybacks to the low-volatility regime. Not surprisingly, the “VIX tantrum” corresponded to the tail end of the buyback blackout period (the SEC forbids buybacks during quarterly reporting to control insider trading). Since 2009, the largest equity drawdowns — August 2015, January to February 2016, and two weeks ago — all occurred in or right after the share buyback blackout period. Even less surprising, corporations stepped in after February 5, 2018, bought the dip, and suppressed volatility. Goldman Sachs’ unit that executes share buybacks for clients had its busiest week ever, seeing roughly 4.5x its average daily volume over 2017.

In a report released last October, Artemis Capital encapsulated the importance of buybacks to the low-volatility regime:

“The later stages of the 2009–2017 bull market are a valuation illusion built on share buyback alchemy…The technique optically reduces the price-to-earnings multiple because the denominator doesn’t adjust for the reduced share count…Share buybacks are a major contributor to the low volatility regime because a large price insensitive buyer is always ready to purchase the market on weakness…Share buybacks result in a lower volatility, lower liquidity, which in turn incentivizes more share buybacks, further incentivizing passive and systematic strategies that are short volatility in all their forms…Like a snake eating its own tail, the market cannot rely on share buybacks indefinitely to nourish the illusion of growth. Rising corporate debt levels and higher interest rates are a catalyst for slowing down the $500-$800 billion in annual share buybacks artificially supporting markets and suppressing volatility.”

Looking solely at topline numbers, the buyback slowdown Artemis fears appears less likely today than ever. Cisco has announced $25 billion in share buybacks already this year. Wells Fargo $22.6 billion. Pepsi $15 billion. Alphabet $8.6 billion. And UBS has predicted Apple will double its buybacks to $60 billion over the next six years as it repatriates its record $265.1 billion offshore cash hoard.

However, the topline numbers neglect the severe inequality within the corporate ecosystem. As of 2015, just 30 firms accounted for half the profits of all publicly-listed U.S. companies, down from 109 in 1979. Only through cheap debt accumulation have laggards been able to afford the buybacks necessary to keep stock appreciation stable. As the IMF warned last year, 22% of U.S. corporations are at risk of default if interest rates rise.

The tax bill may exacerbate, rather than relieve this threat. Moody’s concluded in a report earlier this year: “Low-rated or cyclical companies could see more of their income become taxable as their financial performance deteriorates and their interest expense to EBITDA/EBIT rises meaningfully above the 30% threshold.” ValueWalk summed up Moody’s analysis further: “High quality companies will benefit but low-quality levered companies could get hit hard.”

The short term could survive this threat. As leaders convert their tax-bill windfall into buybacks, laggards may face escalating market and shareholder pressure to keep pace. The past decade plus has provided countless examples of inopportune, if not reckless buybacks. From GE between 2005 and 2007 to Glencore in 2014 and American Airlines since its 2011 bankruptcy, corporate C-suites have time and again prioritized the short-term benefits of buybacks over medium- to long-term debt-management.

Adding to the potential pain, corporations generally retreat from buybacks at times of market uncertainty. The only year in the last 14 in which big U.S. companies spent less on buybacks than dividends was 2009. As Reuters wrote last week: “Share buybacks proliferate when the market is rising but evaporate when the market collapses”:

Source: FactSet

Until the early 1980s, buybacks were illegal in the U.S. due to concerns executives would use them to manipulate share prices. Today, politicians on both sides of the aisle are threatening restrictions, if not a reinstatement of the ban. Democrats have already made it clear buybacks will be a primary attack point as they seek to sway public opinion about the tax law and take back the House and Senate in the midterms. If rising interest rates and market volatility don’t curb buybacks, politicians may step in and do the job anyway.

One way or another, as the low-volatility regime winds down, buybacks appear destined for a day of reckoning. They have played far too big a role in the QE era not to cause complications as QT progresses. In the words of Warren Buffett: “Only when the tide goes out do you discover who’s been swimming naked.”

This article was originally published in “What I Learned This Week” on February 22, 2018. To subscribe to our weekly newsletter, visit 13D.com or find us on Twitter @WhatILearnedTW. The article was originally published in “What I Learned This Week” on February 22, 2018. To learn more about 13D’s investment research, please visit their website.

SB here: I wake up every day thinking about risk. And this letter tries to focus on macro risks, investment risk management and areas of opportunity. As Paul Tudor Jones said, “… most people lose money as individual investors or traders because they’re not focusing on losing money. They need to focus on the money that they have at risk and how much capital is at risk in any single investment they have. If everyone spent 90 percent of their time on that, not 90 percent of the time on pie-in-the-sky ideas on how much money they’re going to make, then they will be incredibly successful investors.”

Trade Signals — Bullish Equity Trend Rolls On; Fixed Income Signals Remain Bearish

S&P 500 Index — 2,738 (02-28-2018)

Notable this week:

Trade signals are unchanged since last week. Fixed income signals remain bearish. The Zweig Bond Model (a trend model for the bond market) is in a bearish “sell” signal. HY is also in a “sell” signal. The equity market trend remains bullish as measured by the Ned Davis Research CMG U.S. Large Cap Long/Flat Index (indicator) and the 13- vs. 34-week Moving Average (MA) of the S&P 500 Index (charts below). Volume demand (buyers) remains bullish. Don’t Fight the Tape or the Fed is signaling a moderately bearish -1 reading (see information below). We need to be on guard for a -2 indicator. The long-term trend in gold remains bullish.

Long-time readers know that I am a big fan of Ned Davis Research. I’ve been a client for years and value their service. If you’re interested in learning more about NDR, please call John P. Kornack Jr., Institutional Sales Manager, at 617-279-4876. John’s email address is jkornack@ndr.com. I am not compensated in any way by NDR. I’m just a fan of their work.

Click HERE for the latest Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note

Hugh Jackman owns a coffee shop called Laughing Man located in Tribeca, just a few blocks from my daughter’s office. I was in NYC for a big meeting and I think it was a big success. But nothing is better than being with the people you love most… my Brianna.

I’ll be in Austin presenting at an advisor event on March 5 and heading from there to San Diego to attend and present on valuations and returns at the Mauldin Economics Strategic Investment Conference on March 6-9. I’m really looking forward to next week. Much to learn.

And I’ll be sharing my notes with you over the coming few weeks. It should make for great content. Inflation, deflation, higher rates, increased vol, geopolitical risks and Fed policy. A chart geek’s Disney Land. I’ll see if I can get access to some of the presentations and the video recording of my presentation.

The SIC lineup is outstanding: David Rosenberg, Dr. Lacy Hunt, Mark Yusko, Stanford University’s Niall Ferguson, Karen Harris from Bain & Company, Jeffrey Gundlach, George Friedman, George Gilder, John Burbank and John Mauldin and more…

For now it’s time to rush out of the office as son, Kyle, is performing in his high school presentation of Hairspray tonight. He says his classmates are ready and he never says that. Susan and I along with my invaluable assistant, Linda; cousin Tommy and our boys are heading to the show. And tomorrow, the Philadelphia Union open their 2018 MLS season. A fun weekend awaits.

Wishing you and your family the very best. Do something fun for yourself! Life is way too short.