This research note was originally published by the CFA Institute’s Enterprising Investor blog. Here is the link.

[REITs]

Q2 hedge fund letters, conference, scoops etc

SUMMARY

- Mutual funds exhibit momentum when measured by their one-year performance

- Momentum disappears when more reasonable fund selection criteria are applied

- Performance does not seem effective for fund selection for a full market cycle

CHASING PERFORMANCE

Chasing mutual fund performance suffers from a bad reputation these days. Of course, perspectives change all the time in finance. What was once considered poor form often becomes best practice and vice versa. Leveraged buyouts and activist investors, for instance, were once looked down on by much of the sector, but today their milder incarnations are staples of pension fund portfolios and are perceived as forces of good, not evil.

So maybe investing in the best-performing mutual funds isn’t a bad strategy. It is certainly a popular one. The question is, how does mutual fund momentum chasing play out in the US market?

CLASSIC MOMENTUM

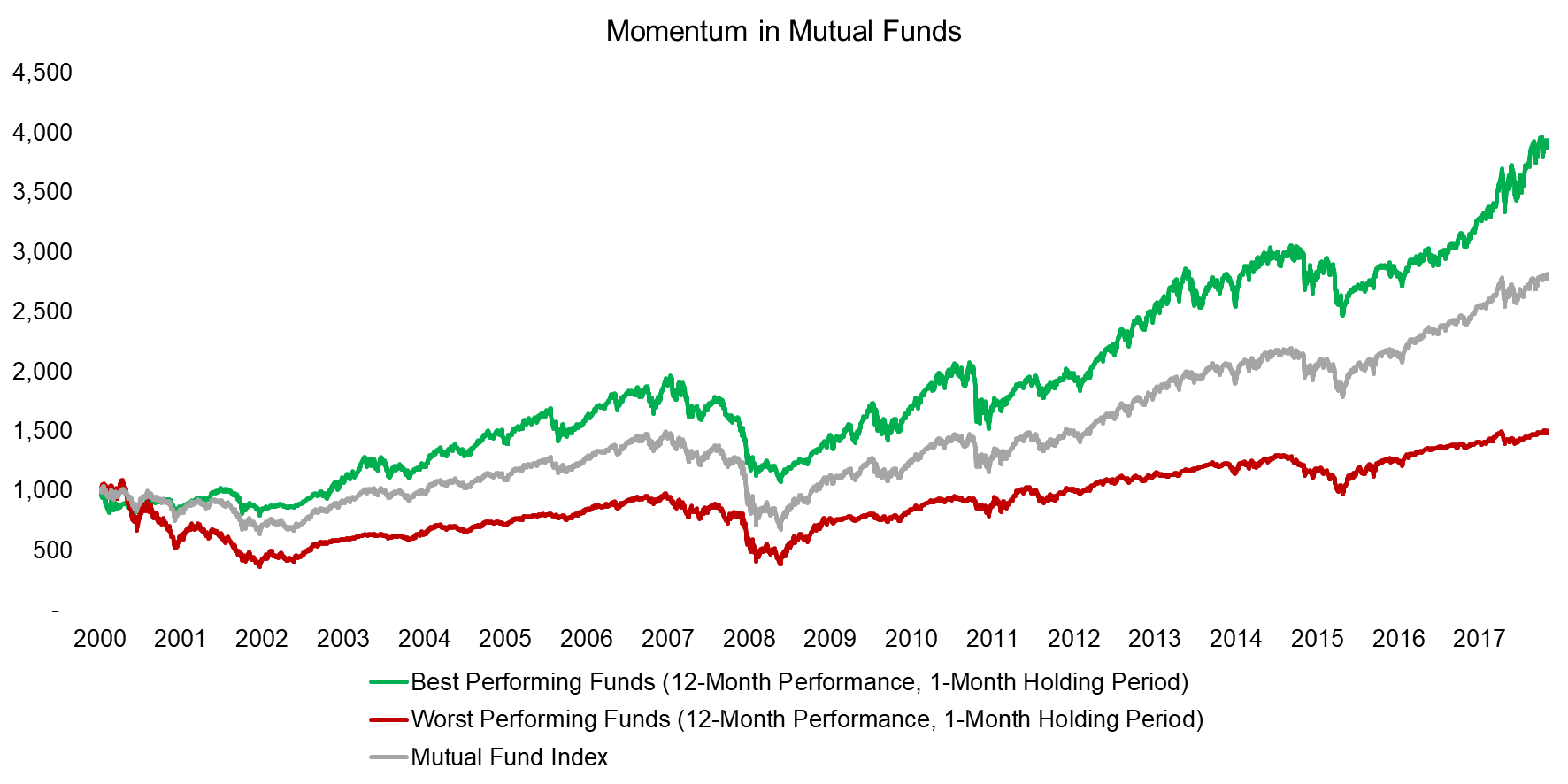

To answer that, we looked at US equity mutual funds from 2000 to 2018 and created long-only portfolios composed of the top and bottom 10% of funds. We then replicated classic equity momentum strategies, selecting mutual funds based on their performance over the previous 12-months and rebalancing the portfolio on a monthly basis.

We found the best-performing funds beat an equal-weight index of all equity mutual funds as well as the worst-performing funds by a handsome margin. Put another way: Performance chasing works.

Source: FactorResearch

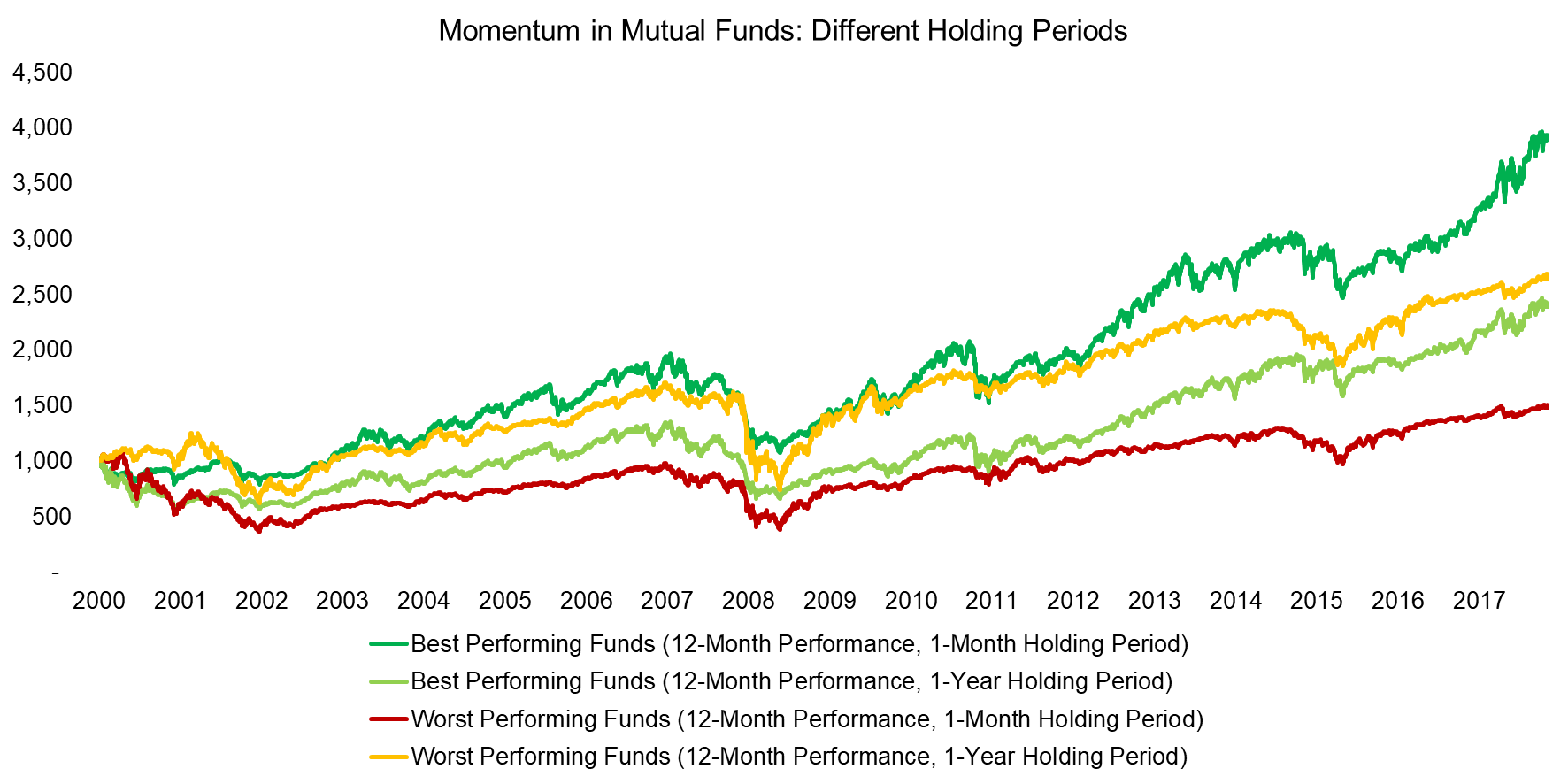

Of course, most mutual fund investors won’t be willing to rebalance their portfolios every month. Moreover, our calculations did not include transaction costs, which are likely in excess of 1%. As a consequence, these results are more theoretical than practical.

And, if we impose a minimum holding period of one year, performance chasing looks far less appealing. The best- and worst-performing funds with one-year holding periods generated similar returns from 2000 to 2018, albeit with significant differences in performance at different times.

Source: FactorResearch

CLASSIC MUTUAL FUND SELECTION

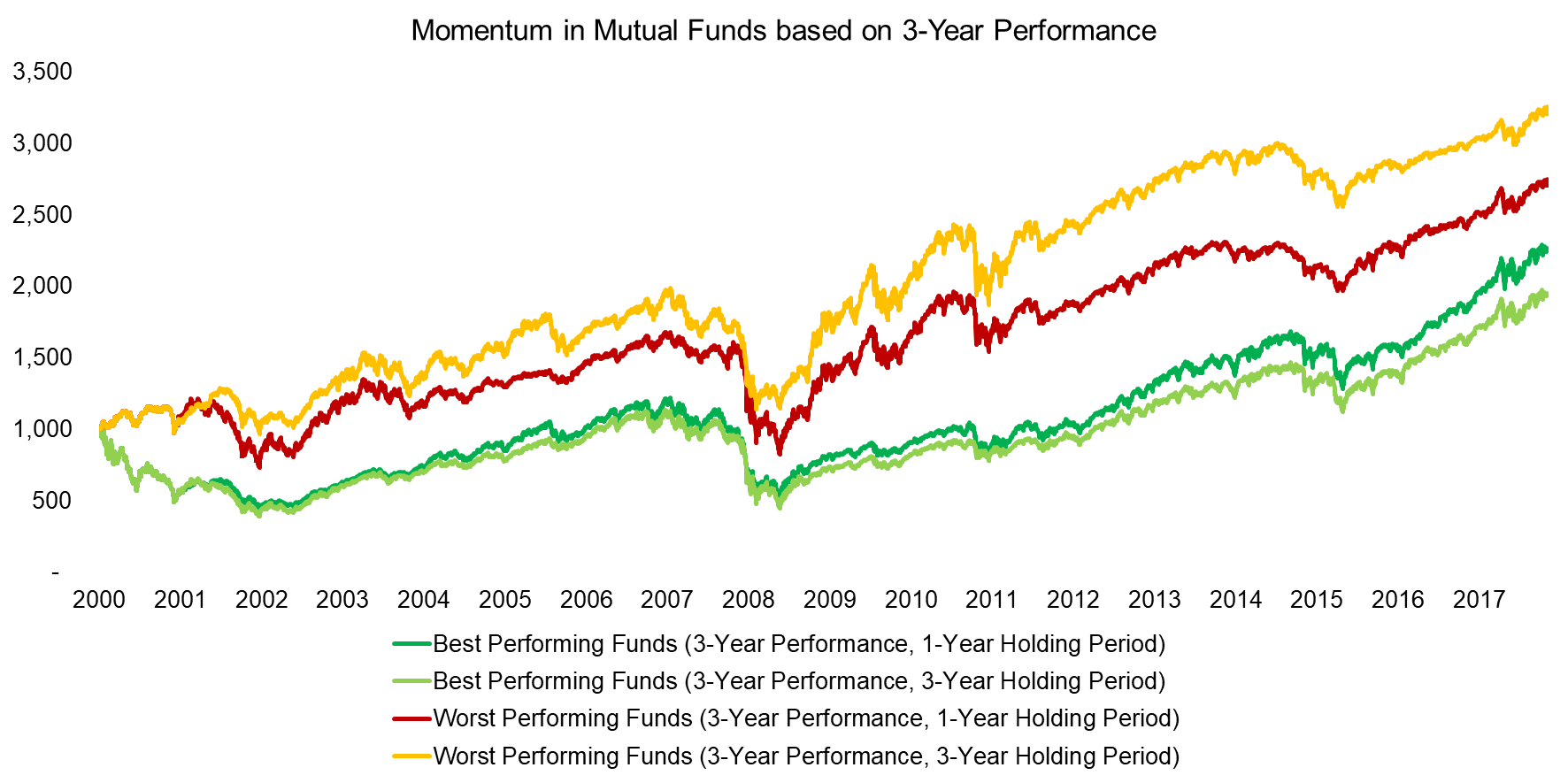

Although buying winners and selling losers in equities is typically based on a 12-month lookback period, such a time frame is rather short for most mutual fund allocators. Since investors seek to distinguish the skilled managers from the lucky, they usually analyze fund manager performance over several years.

Three years is considered the bare minimum for evaluating mutual funds, which hopefully includes some ups and downs in stock markets. Applying this momentum strategy, we selected funds based on their three-year performance and held them for one and three years, respectively.

The results suggest that mutual fund chasing deserves its bad reputation. The worst-performing funds outperformed the best-performing, regardless of the holding period. This indicates that mean-reversion, not momentum, dominates fund returns when measuring funds on longer-term performance.

Source: FactorResearch

That said, when the analysis begins has a significant influence on the outcome. For example, the worst-performing funds generated the best returns between 2000 and 2002, but fell back to earth thereafter. Why the initial outperformance? The implosion of the dot-com bubble: The worst-performing funds probably held far fewer technology stocks than their counterparts.

The same calculus applies to the global financial crisis in 2008 and 2009: The drawdowns of the best-performing funds are significantly higher than those of the worst performers, presumably because the latter had less exposure to the sectors — banks and real estate, for example — that underperformed during the crisis.

These results suggest the best-performing funds lose more during crashes, giving up all the outperformance they achieved in the stable years. Therefore, past performance does not seem meaningful for selecting funds for a full market cycle.

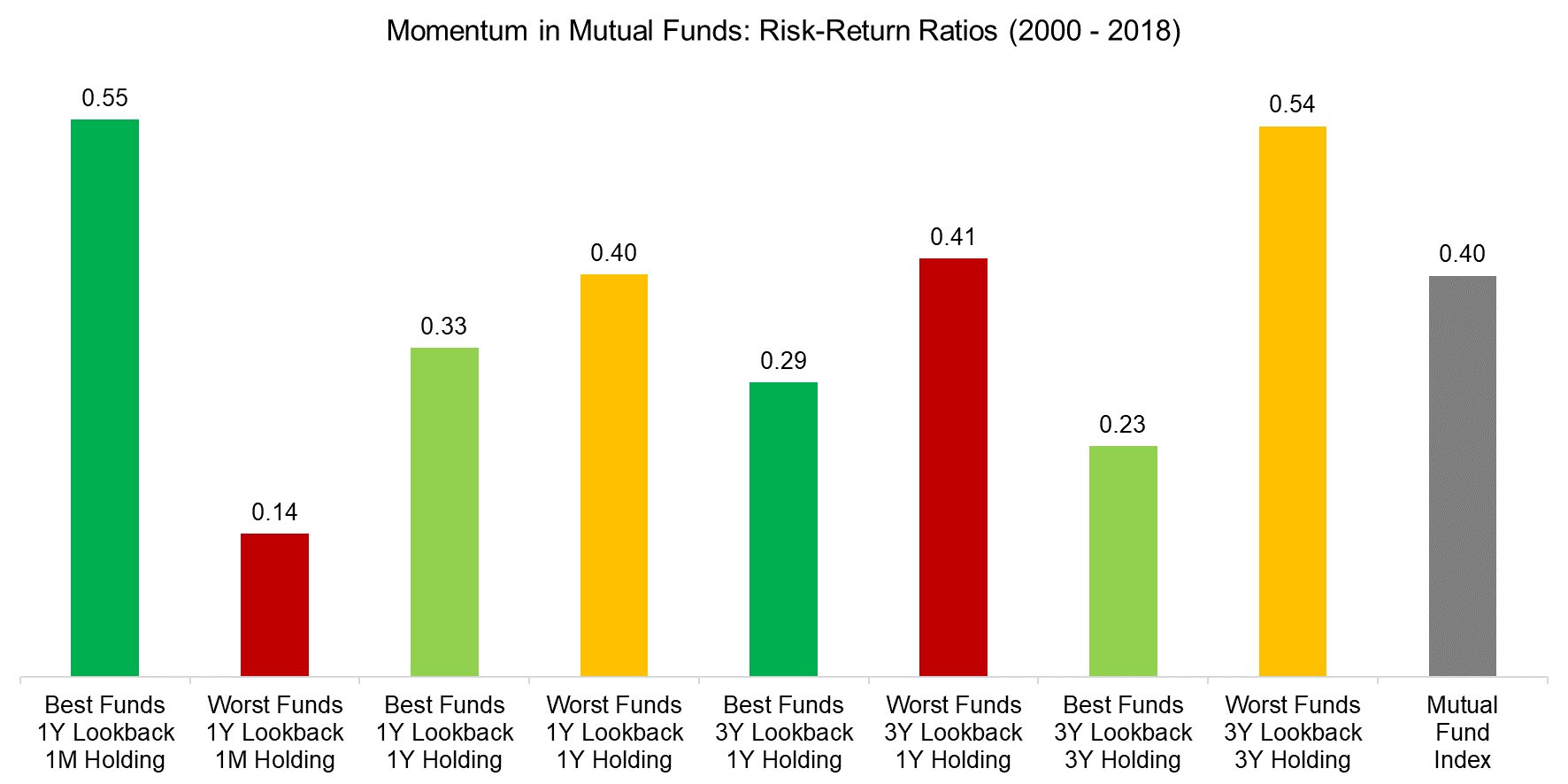

RISK-METRICS COMPARISON

So do the worst funds yield less attractive risk-adjusted returns than their better-performing peers. We found the dismal performers generated higher risk-return ratios than the standout funds in all scenarios except for one: when momentum is measured with a 12-month lookback and one-month holding period. And that scenario would likely be different were trading costs factored in.

Source: FactorResearch

FURTHER THOUGHTS

So does performance chasing in the mutual fund universe deserve its less-than-stellar reputation? It depends. If the momentum strategy is systematically implemented, frequently rebalanced, and has low transaction costs, it can generate excess returns.

But as a rule, performance chasing is best avoided. Our analysis indicates that investors would be better off betting on mean-reversion.

RELATED RESEARCH

Sector versus Country Momentum

ABOUT THE AUTHOR

Nicolas Rabener is the Managing Director of FactorResearch, which provides quantitative solutions for factor investing. Previously he founded Jackdaw Capital, an award-winning quantitative investment manager focused on equity market neutral strategies. Before that Nicolas worked at GIC (Government of Singapore Investment Corporation) in London focused on real estate investments across the capital structure. He started his career working in investment banking at Citigroup in London and New York. Nicolas holds a Master of Finance from HHL Leipzig Graduate School of Management, is a CAIA charter holder, and enjoys endurance sports (100km Ultramarathon, Mont Blanc, Mount Kilimanjaro).

Article by Factor Research