Portfolio Manager Chuck Royce and Co-CIO Francis Gannon discuss why non-earners and healthcare are doing well, but industrial and material businesses seem to be unrecognized by the market—at least for now.

[timeless]

Q2 hedge fund letters, conference, scoops etc

Francis Gannon How are you thinking about valuations today?

Chuck Royce I believe that we remain in the period of change with rates drifting higher, as they have, with returns coming down, which they have a little bit in the three- and five-year category, certainly not in the two-year category. I think returns are coming down though in general. And I think volatility’s going up. So we’re continuing to use those pathways in our, our stock selection, so we are thinking very strongly that multiples will continue to compress and we’re taking advantage of the current markets to lighten up the higher multiple types of stocks.

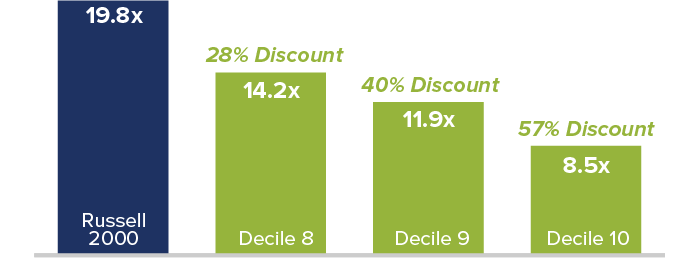

Many Small-Caps Sell at a Significant Discount

Bottom Three Deciles in Russell 2000 Median LTM EV/EBIT1 ex negative EBIT as of 6/30/18

1 Last Twelve Months Enterprise Value/Earnings Before Interest and Taxes

FG One of the things I thought would be interesting to talk about is, what are you hearing from companies today about inflation? About tariffs? What’s the mindset from many of these businesses that you’re hearing from?

CR Well, everyone has their own set of inflation problems. Hiring people is a long-term problem in the areas where you’re trying to hire highly technically skilled people. There’s considerable inflation in that zone and has been for some time. Managing that is part of their job. Inflation of cost structures is another part to the equation. Those that rely on commodity inflation, that’s entering into the picture a little bit in the oil world. So everybody thinks about it in their own particular way. The better companies manage these things in a better way. The threat of tariffs is of course what’s bothering the marketplace. We have many companies that have… you know, they have vulnerability to severe tariffs, as does the whole world. But I think this is more of a headline risk than a reality today, and I suspect these things will be resolved in time.

FG So inflation is part of the normalization process we’ve been talking about for a period of time.

CR: Absolutely.

FG So what’s the case for cyclicals now?

CR The case for cyclicals is as strong today as it’s been for some time. Within the cyclical zone… first place, we’ve always used cyclical, we’ve always used industrials, lots of industrials, we love high quality industrial companies. They tend to have a global reach. And they tend to sell at a lower multiple. They certainly did not do us any performance benefits in the second quarter. The world favored, again, tech and health in this quarter. A little bit of a surprise, because we believe in this road to normalization that that wouldn’t be as true as it was let’s say for last year. But apparently this quarter is sort of back to what was happening last year. Nevertheless, we believe that a great industrial sort of well positioned in their markets, will do quite well over time.

Cyclicals Cheaper than Defensives

Median LTM EV/EBIT¹ Ex. Negative EBIT for Russell 2000 as of 6/30/18

¹ Last Twelve Months Enterprise Value/Earnings Before Interest and Taxes

FG Why do you think we’re seeing that disconnect between the underlying fundamentals we’re hearing from many of our cyclical businesses, and the reality of the market, where non-earners were doing well, healthcare is doing well, but these industrial businesses, material businesses, seem to be unrecognized by the market, at least for the moment?

CR Frank, I’m not sure I can give you a perfect answer on that. These things are never lined up perfectly, and that’s what taking long-term bets is all about, actually.

FG Have you lost confidence in some of the cyclical businesses just given the many factors that are affecting them right now?

CR No. We are increasing cash around the edges and we are taking advantage of this stronger than expected market to reduce the sort of higher multiple components of our portfolios.

Article by Chuck Royce and Francis Gannon, Royce Funds