“… I think Cohn resigning, was basically (telling us) that trade protectionists

have taken over the economic thought process at the White House. And I think that’s really disturbing.”

– David Rosenberg

BoAML: Investors Yet to Act on Fears

China’s President Xi Jinping, in a speech this week, highlighted his desire to further open up China’s economy by increasing imports and protecting their trading partners’ intellectual property. The markets calmed.

Here are a few things for us to consider:

- Nearly 20% of China’s total exports went to the U.S. in 2017 or roughly $420 billion. 31% of their exports went to other Asian countries, 3% to Germany, 2.5% to the U.K., 11% to other European countries and the balance of exports of approximately 33% to other countries.

- The U.S. exported roughly $154 billion in goods to China in 2017. This represented approximately 8% of total U.S. exports. The U.S. sits in a better bargaining position.

Certain industries would be impacted more than others. For example, total U.S. auto exports to China were 20% of total global exports. Civilian aircrafts, engines, equipment and parts to China were 13% of total global exports. Other industries, especially agriculture were much greater: 55% of the soybean total global exports went to China; 75% of sorghum, barley and oats went to China; hides and skins 50%; logs and lumber 45%; fish and shellfish 22%; crude oil 20.5%; cotton and raw materials 17%.

So it is clear, some industries would be more affected than others. While the U.S. appears to sit in an advantageous position, China is smart and has a degree of leverage. Perhaps targeting industries more aligned to Trump’s political base. Though I’m not sure that will move the needle. Both countries should not underestimate the degree of national pride. Made in America or Made in China? Depends on just how upset each country’s consumer might be.

China has other plays. Currency manipulation could be used as a tool. China could also devalue their currency to offset the higher prices due to U.S. imposed tariffs. China could choose to dump their $1.2 trillion worth of U.S. Treasury holdings. That would put upward pressure on interest rates. And at a time that the U.S. Treasury is issuing even more bonds to cover its huge government spending shortfall… estimated to be north of $800 billion this year.

Such a mass sale would hurt China’s pocket, yet it would prove to be a dagger to the bond market’s heart at a time the federal government could least afford the additional interest expense. Though the last time China played the currency card (they devalued the Yuan in August 2015), it caused major instability and capital outflows from China. Consequences abound.

In conclusion, China does not sit in a strong position to win a trade war, but can inflict some pain on the U.S. economy and markets. Both sides have moves to make and the stakes are high.

It is my view that President Trump is creating leverage for coming negotiations. While no actual trade war bullets have been fired, negotiations could fail, which could result in a range of outcomes, including an all-out trade war. In the end, there’s no winner in a trade war. Trade wars lead to higher prices and slower economic growth. All parties lose.

This takes my head back to a panel discussion at the Mauldin Economics 2018 Strategic Investment Conference and I’ll conclude what was going to be a six-part series with today’s piece. Jacob Shapiro, Director of Analysis at Geopolitical Futures, emceed an expert panel that included David Rosenberg, Louis-Vincent Gave and Grant Williams. “Let’s get right down into it. What I want to ask about is the elephant that’s been in the room, and we’ve been talking about it a little bit but haven’t exactly addressed it. And even last week, I wasn’t sure this is what I was going to have to ask. But I think we have to ask about trade wars and tariffs. What does a trade war look like? Is it important? Are we in 1930? Or are we just in a minor spat over stuff? Maybe each one of you could take that question.”

Global Growth Has Peaked, We Are In A “Dangerous New Phase”

I share with you my high level notes on that discussion. Rosenberg has some interesting insight on NAFTA. It’s not just about China…

Grab a coffee and find that favorite chair. I promised you a much shorter On My Radar this week and I’m going to stay true to that promise. Today you’ll also find a great chart that shows “when the economy is in great shape; there is little risk of bear market.” Bear markets tend to be worse during recessions. Next week we’ll take a look at my favorite inflation and recession indicators. Bottom line: nothing to lose sleep over at the moment. You’ll also find the most recent Trade Signals charts. Moderately bullish conditions remain though the NDR CMG U.S. Large Cap Long/Flat indicator moved from 100% to 80% equity exposure earlier this past week. A slight de-risking of market exposure.

Finally, I want to say thank you. I received a large number of emails after my personal story last week about the last few days of my father’s life and the Masters last week. It was a wonderful moment for me and dad. It was a Starbucks latte, the Masters on TV and five hours of dad fully engaged. I read your personal stories and I was really touched… please know I’m grateful.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- Mauldin Economics 2018 SIC — Expert Panel: David Rosenberg, Louis-Vincent Gave and Grant Williams

- When the Economy is in Great Shape, Can There be a Bear Market?

- Trade Signals — NDR CMG U.S. Large Cap Long/Flat Index De-risking to 80%

- Personal Note — Stay Over the Ball

Mauldin Economics 2018 SIC — Expert Panel: David Rosenberg, Louis-Vincent Gave and Grant Williams

Said the Bull…

Moderator Jacob Shapiro asked, “What does a trade war look like? Is it important? Are we in 1930? Or are we just in a minor spat over stuff? Maybe each one of you could take that question.”

Following are my notes in bullet point format:

David Rosenberg:

- “Well look, I don’t think it’s the start of the 1930s, but I think it’s a shift in the global trading environment that we haven’t seen to this extent. I don’t even think under Reagan and under George W. Bush, which had selective short-term tariffs, say on Japan.

- I think this is something that runs a lot deeper. And it’s because, I mean… Donald Trump. If you go back and you just Google or YouTube what he was saying in the 1980s about trade, he’s always had this view that the trade deficit is something that’s very bad for the United States. So this is all part and parcel of eliminating the trade deficit, point number one, which they think is bad for the economy.

- And it’s hard to handicap the extent to which the rest of the world is going to respond, despite all the bravado. Because for most countries, the U.S. consumer, which is like 20% of global GDP, is their biggest base. So you want to go a little easy on how far you want to retaliate.

- I would say that the Gary Cohn resignation, which follows a week after the U.S. ambassador to Mexico just announced her resignation, this is not good news for NAFTA in particular. And I think that Moodys.com ran some numbers… based on retaliatory measures by the rest of the world… there’s no question abrogation of NAFTA is horrible for Canada and it’s horrible for Mexico.

- But it’ll cost the U.S. four million jobs on net. So it’s not as if it’s going to be a walk in the park in the United States.

- And NAFTA is the world’s largest manufacturing supply chain. So that would be a massive disruption.”

David Rosenberg continued:

- “And I think Cohn resigning, when I said the white flag, I think that was basically it… that trade protectionists have taken over the economic thought process at the White House. And I think that’s really disturbing.

- To me, the big deal is going to be… and maybe we won’t know until after the Mexican elections in July… but to me, really… the line in the sand is going to be NAFTA.

- Because abrogating NAFTA is going to create tremendous disruption and probably trigger a recession earlier than I think it’s going to happen.” (Bold emphasis mine)

Louis-Vincent Gave:

- “I completely agree, of course, with everything David said.

- Look, for me the biggest issue is, I think, by using national security considerations to impose these tariffs, I think Pandora’s Box has been opened. In that, within the WTO you had one exception, which was you could claim things for national security. But people didn’t use that. And here it’s being used, frankly, so not only when you look at the fact that something like 40% of the aluminum that the U.S. imports is from Canada, which is hardly a security threat for the U.S. The fact that basically Pandora’s Box has now been opened is, to me, it is indeed disturbing.

- There’s no right time in the cycle for this, of course, but I think it’s happening at a very wrong time in the cycle when already the labor market is tight in the U.S., when already inflation is moving up, when, and as I said in my speech [see last week’s post On My Radar: Mauldin Economics 2018 SIC (Part 4) – Louis-Vincent Gave: China’s Game-Changing Policy Shifts for my notes on Louis-Vincent’s presentation], China itself is changing or attempting to change its stripes, when the manufacturing base in all our countries is as old as it’s ever been. To me, it seems very short sighted and could have big, big consequences.”

Louis-Vincent Gave continued:

- “And if indeed, one of the positive takes on it is that Trump is doing this to increase his leverage in the NAFTA negotiations that are ongoing now. So basically, it’s part of the art of the deal: You know, you play tough and then you get a better deal. And then at the back end, everything will work out.

- If it does lead to the implosion of NAFTA, which seems likely as Dave was highlighting, then that’s very, very bad news.”

Grant Williams:

- “First of all, never sit down the far end, because all the smart stuff gets said and you’re left holding the bag…

- When I first read about it, I was alarmed like everybody else. When I found out that trade wars are both great and easy to win, I calmed down a little bit. So I feel happier now. [Grant said in a smug way… a fun poke at Trump.]

- But you know, to me, it’s more symptomatic of the fact that right now we’re at a point where the entire world is shifting. And you know, we had two fantastic presentations this morning. First of all from Rosie [David Rosenberg], who has been renowned for being bullish. And when Rosie switches, you need to pay attention, because he’s stuck with his guns that entire time.

- Then you get the guy [Louis-Vincent Gave] who was the perma-bull on China shifting. And saying in so many words, “I’m no longer a perma-bull on China.” So I think everywhere we look, whether it’s Louis-Vincent’s point about China looking to pay for oil in yuan, I think it’s such a crucial story to understand.

- Everywhere we look there are shifts happening… And these things tend to happen at major inflection points. And my worry about the trade war and the tariffs is that they open up the possibility of miscalculations. And human beings and politicians, particularly the kind of politicians we seem to have spread out around the world now, are very prone to overstepping and making a step too far, and then things get out of control very quickly.

- And I think we really do need to open our eyes to possibilities in secular shifts that we perhaps have thought weren’t even on the table for the last decade or so.”

“Open our eyes…” Indeed. This is big, friend. Keep it on your radar.

When the Economy is in Great Shape, Can There be a Bear Market?

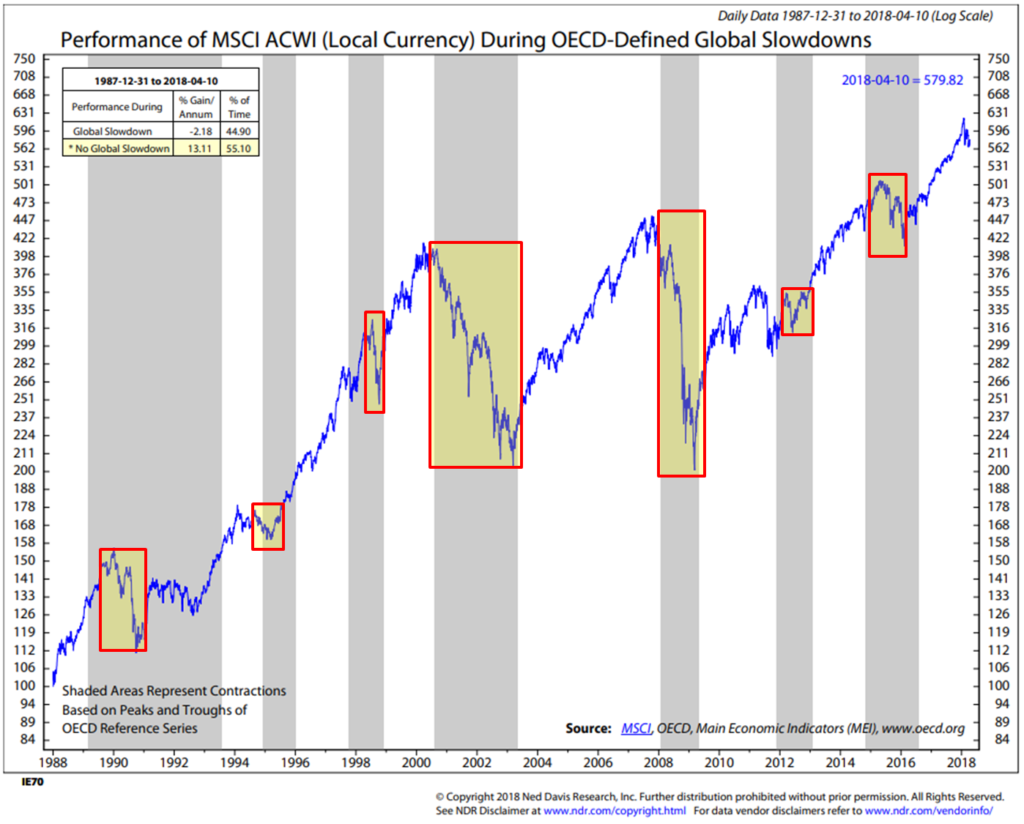

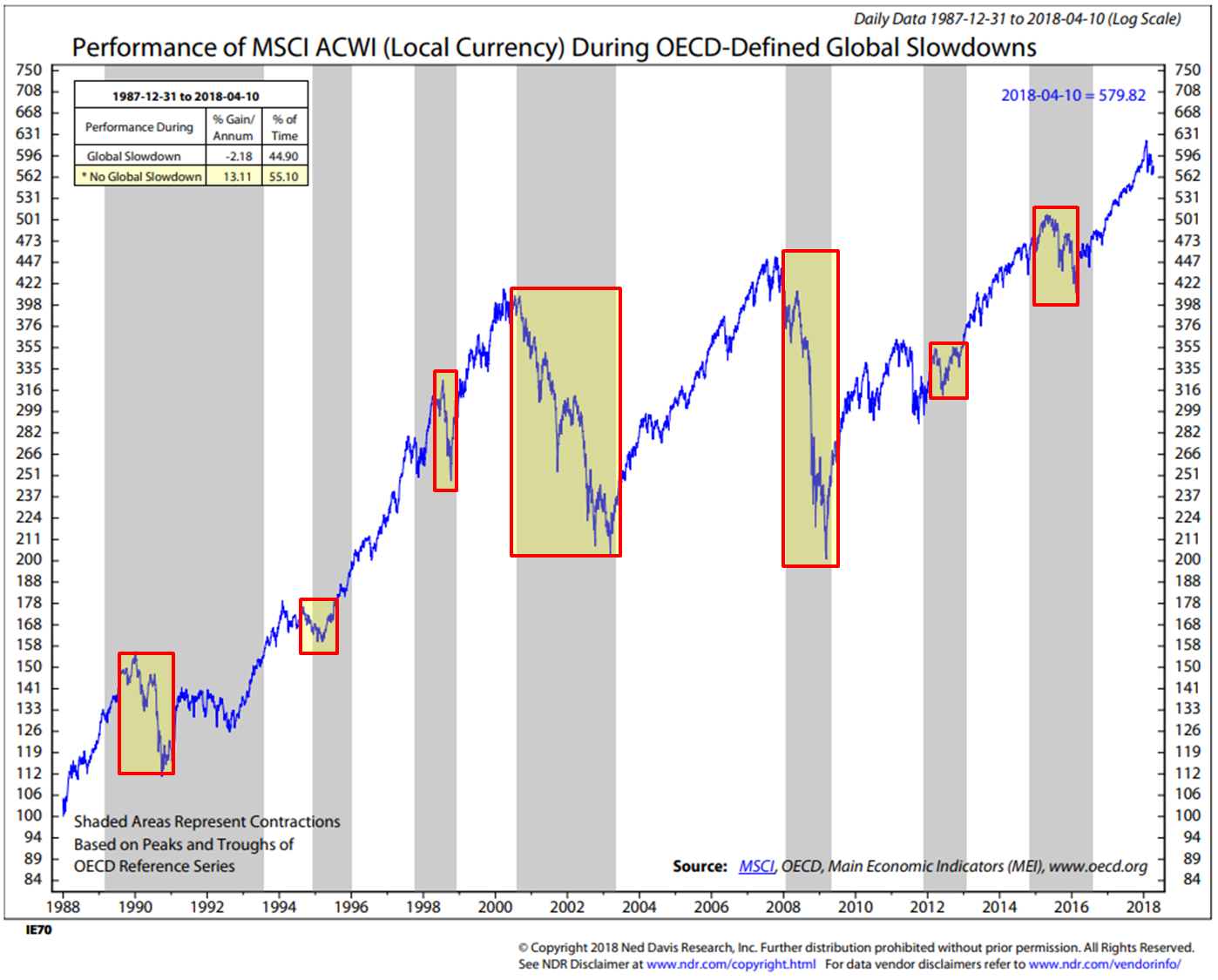

The short answer is no. Possible? Yes, but history suggests it’s highly unlikely. The large stock market declines have occurred during or near global recessions.

Here is how you read the next chart:

- The following chart plots the performance of the MSCI All Country World Index during global slowdowns (blue line).

- The yellow highlighted areas show the large drawdowns (data represented is 1988 – present)

- The shaded vertical lines show the recession periods.

Bottom line:

- 1990-1991 recession — the ACWI declined approximately -30%

- 2000-2003 recession — the ACWI declined approximately -52%

- 2008-2009 recession — the ACWI declined approximately -55%

There was, of course, the Eurozone debt crisis in 2011 (-21%), the Long-Term Capital Management crisis in 1998 (-26%) and the -21% decline in 2015, to name a few others, yet it is in recession that the bad stuff happens… we will look at those charts next week (no sign of recession in the next six to nine months).

Finally, can we keep in the back of our mind that the global central bankers invented a brand new way to support the markets with their goals to get the economy going post the 2008 great financial crisis? Think about the above commentary on trade. It is one issue. The globe is deeply in debt. Much of it short-term debt. The Fed is raising interest rates… this is a different period from that which inflated asset prices. Higher rates on record high debt means budgets are further pinched.

Ten of the last 13 Fed rate raising cycles have landed us in recession. The three that didn’t were modest economic contraction, but I’d argue our current starting conditions of record high government debt, record high corporate debt and record high equity market valuations are not good starting conditions. I totally expect that the current Fed interest rate raising cycle will land us in recession. Inflation is the current cover to continue raising rates so the Fed continues on plan… I see 2019 recession and similar market declines to those we experienced during the last two recessions… maybe -60% to -70% before it is over. That to me is one super outstanding investment opportunity. More defense than offense until the starting conditions get great.

Trade Signals — NDR CMG U.S. Large Cap Long/Flat Index De-risking to 80%

S&P 500 Index — 2,652 (04-11-2018)

Notable this week:

NDR CMG U.S. Large Cap Long/Flat Index moved to an 80% large cap exposure signal from 100%. The 13-week trend line vs. the 34-week trend line remains on a buy signal. Volume Demand continues to be greater than volume supply which supports a bullish posture. The CMG HY Bond Program moved to a “buy” signal. And extreme investor pessimism is short-term bullish for the market as well as you’ll see in the posted charts.

The 200-day MA line and the February low remain important downside support. Here is a look:

From time to time I’m asked about NDR’s Big Mo (Momentum) indicator. While it’s composite trend line is moving lower, it too remains in a buy signal.

You’ll find the updated Trade Signals charts and current positioning of our CMG TREND Series of Portfolios below.

The next section walks you through all of the Trade Signals charts.

Prices Of This Metal Could Be About To Soar

Long-time readers know that I am a big fan of Ned Davis Research. I’ve been a client for years and value their service. If you’re interested in learning more about NDR, please call John P. Kornack Jr., Institutional Sales Manager, at 617-279-4876. John’s email address is jkornack@ndr.com. I am not compensated in any way by NDR. I’m just a fan of their work.

Click HERE for the latest Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note — Stay Over the Ball

The Philadelphia Union is playing a home game tonight at 8:00 pm. Susan, the boys and I are heading to the game. It looks like it is going to be a very so-so season. Then tomorrow I’m going to Penn State and taking son, Matthew, and nephews Mike and Dan to play golf at Centre Hills. Dad’s old home course. His best friend, Bruce Parkhill, planted a tree for him several years ago and set a plaque in his honor at the base of that tree. We have a remaining few of dad’s ashes and we are going to set them on his old home course. Dad had a funny looking swing. When he hit a good shot he’d quickly ask, “Did I loop?” My answer was always the same, “Unfortunately, yes.” It wasn’t the best back swing but it worked.

As I was finishing the letter today, my sister, Amy, sent me this note. To say he was obsessed with golf is an understatement… “Stay over the ball (no sway) – right knee in. When swinging – right palm open…” It is written on the back of an old score card. Anyway, it made my day…

Dad, step-mom Eilene and me in 2011.

A cold IPA and peanuts are in my immediate future… A fun weekend ahead… and it’s going to be in the 70s.

Meetings in Florida, Austin and Dallas are approaching quickly. Enjoying the ride… hope you are enjoying yours as well!

Wishing you the best!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.