In Berkshire Hathaway’s latest annual shareholder letter Warren Buffett provides a great illustration of how price randomness in the short term can obscure longterm growth in value. His following real-life example demonstrates that in order to achieve longterm outperformance investors must suffer through periods of significant underperformance.

[buffett]

Check out our H2 hedge fund letters here.

Here’s an excerpt from that letter:

Charlie and I view the marketable common stocks that Berkshire owns as interests in businesses, not as ticker symbols to be bought or sold based on their “chart” patterns, the “target” prices of analysts or the opinions of media pundits. Instead, we simply believe that if the businesses of the investees are successful (as we believe most will be) our investments will be successful as well. Sometimes the payoffs to us will be modest; occasionally the cash register will ring loudly. And sometimes I will make expensive mistakes. Overall – and over time – we should get decent results. In America, equity investors have the wind at their back.

From our stock portfolio – call our holdings “minority interests” in a diversified group of publicly-owned businesses – Berkshire received $3.7 billion of dividends in 2017. That’s the number included in our GAAP figures, as well as in the “operating earnings” we reference in our quarterly and annual reports.

That dividend figure, however, far understates the “true” earnings emanating from our stock holdings. For decades, we have stated in Principle 6 of our “Owner-Related Business Principles” [bottom of this page] that we expect undistributed earnings of our investees to deliver us at least equivalent earnings by way of subsequent capital gains.

Our recognition of capital gains (and losses) will be lumpy, particularly as we conform with the new GAAP rule requiring us to constantly record unrealized gains or losses in our earnings. I feel confident, however, that the earnings retained by our investees will over time, and with our investees viewed as a group, translate into commensurate capital gains for Berkshire.

The connection of value-building to retained earnings that I’ve just described will be impossible to detect in the short term. Stocks surge and swoon, seemingly untethered to any year-to-year buildup in their underlying value. Over time, however, Ben Graham’s oft-quoted maxim proves true: “In the short run, the market is a voting machine; in the long run, however, it becomes a weighing machine.”

************

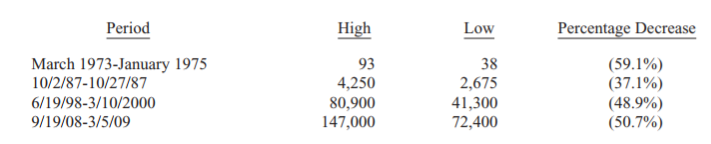

Berkshire, itself, provides some vivid examples of how price randomness in the short term can obscure longterm growth in value. For the last 53 years, the company has built value by reinvesting its earnings and letting compound interest work its magic. Year by year, we have moved forward. Yet Berkshire shares have suffered four truly major dips. Here are the gory details:

This table offers the strongest argument I can muster against ever using borrowed money to own stocks. There is simply no telling how far stocks can fall in a short period. Even if your borrowings are small and your positions aren’t immediately threatened by the plunging market, your mind may well become rattled by scary headlines and breathless commentary. And an unsettled mind will not make good decisions.

In the next 53 years our shares (and others) will experience declines resembling those in the table. No one can tell you when these will happen. The light can at any time go from green to red without pausing at yellow. When major declines occur, however, they offer extraordinary opportunities to those who are not handicapped by debt. That’s the time to heed these lines from Kipling’s If:

“If you can keep your head when all about you are losing theirs . . .

If you can wait and not be tired by waiting . . .

If you can think – and not make thoughts your aim . . .

If you can trust yourself when all men doubt you…

Yours is the Earth and everything that’s in it.”

Principle 6 of our “Owner-Related Business Principles”

Accounting consequences do not influence our operating or capital-allocation decisions. When acquisition costs are similar, we much prefer to purchase $2 of earnings that is not reportable by us under standard accounting principles than to purchase $1 of earnings that is reportable. This is precisely the choice that often faces us since entire businesses (whose earnings will be fully reportable) frequently sell for double the pro-rata price of small portions (whose earnings will be largely unreportable). In aggregate and over time, we expect the unreported earnings to be fully reflected in our intrinsic business value through capital gains.

We attempt to offset the shortcomings of conventional accounting by regularly reporting “look-through” earnings (though, for special and nonrecurring reasons, we occasionally omit them). The look-through numbers include Berkshire’s own reported operating earnings, excluding capital gains and purchase-accounting adjustments (an explanation of which occurs later in this message) plus Berkshire’s share of the undistributed earnings of our major investees – amounts that are not included in Berkshire’s figures under conventional accounting. From these undistributed earnings of our investees we subtract the tax we would have owed had the earnings been paid to us as dividends. We also exclude capital gains, purchase-accounting adjustments and extraordinary charges or credits from the investee numbers.

We have found over time that the undistributed earnings of our investees, in aggregate, have been fully as beneficial to Berkshire as if they had been distributed to us (and therefore had been included in the earnings we officially report). This pleasant result has occurred because most of our investees are engaged in truly outstanding businesses that can often employ incremental capital to great advantage, either by putting it to work in their businesses or by repurchasing their shares. Obviously, every capital decision that our investees have made has not benefitted us as shareholders, but overall we have garnered far more than a dollar of value for each dollar they have retained. We consequently regard look-through earnings as realistically portraying our yearly gain from operations.

In 1992, our look-through earnings were $604 million, and in that same year we set a goal of raising them by an average of 15% per annum to $1.8 billion in the year 2000. Since that time, however, we have issued additional shares – including a significant number in the 1998 merger with General Re – so that we now need look-through earnings of $2.4 billion in 2000 to match the per-share goal we originally were shooting for. This is a target we still hope to hit.

You can read the entire latest shareholder letter here.

You can read the Berkshire Hathaway ‘Owners Manual’ here.

For more articles like this, check out our recent articles here.

Article by Johnny Hopkins, The Acquirer’s Multiple