Right now, you could be making several dangerous investing mistakes… and you might not even realise it.

Barclays Bank: Well Capitalized But Banking Reform Is A Risk

For years, a lot of (otherwise) smart people have believed three big myths about investing. And they could be costing you a lot of money…

BAML: Risk-Off Sentiment Gathers Pace

Dangerous Myth #1: “It’ll come back.”

The key to not suffering big losses – and to having enough capital to see another day – is to establish a plan for every investment and follow it. Before you buy a stock, know when you’ll sell it.

No one likes to admit defeat. But in investing, it’s important to have a disciplined approach to selling your bad positions.

For most people, clinging to the hope that a losing trade will turn around is far easier than admitting it didn’t work, selling, and moving on.

When a price drops, it’s easy to tell yourself: “If I just hang on a bit longer, this stock will reverse and go up.” If the market bounces back, you feel like a genius… until it falls again. And in a bear market, the trend is down – so those up days don’t make up for the down days.

Also, it’s easy to forget how much a falling stock needs to climb before you recover your losses. That stock that lost 50 percent doesn’t have to rise 50 percent before you’re back to breakeven. That stock has to double. And if you’re down 70 percent? It’s a three-bagger and then some, just to get back to where you started.

Waiting for a stock to recover means you could miss out on some other investment opportunities that come along, which is called the opportunity cost.

So how do you create a loss-aversion plan for every stock you own?

Have a mental stop-loss before you enter a trade.

The best kind of stop-loss order is a trailing stop-loss. This order “trails” a rising stock by always resting a pre-determined amount (either a percentage or an absolute figure) below the stock’s most recent high (that is, since you’ve owned it).

(One important point: Make sure you don’t put a standing market order in at your trailing stop level. You don’t want to tell your broker when you’re going to sell. Make sure that you make it a mental level – not one that you tell your broker. And then watch it.)

Seth Klarman: “Most Investments Are Dependent On Outcomes That Cannot Be Accurately Foreseen”

Selling a stock at a loss is disappointing. But it limits your downside and protects your capital so you can invest in other opportunities down the line.

So, take a look at your portfolio. How many of your positions are down 50 percent? Ask yourself, how many stocks have you owned – ever – that have doubled? And… how many of those positions that are down 50 percent (or more) are likely to double (or more)?…

So… maybe it’s time to walk away.

Dangerous Myth #2: “They’re professionals… they know what they’re doing.”

In the investment world – as in most other arenas of life – there are plenty of “experts” eager to tell you what to think. But relying too much on these types can be just as bad as investing blindly, for two reasons.

First, no one – not even (or especially) so-called experts – are right all of the time, or even most of the time. Listening to supposed authorities too much is called the “seersucker illusion” – from the expression: “For every seer, there is a sucker.”

People fall victim to this even though the average market “seer,” or expert, has a lousy record of predicting anything.

To Avoid Danger, Proper Framework Needed For Machine Learning Investing Systems

Second, most investment experts (or investment advisers, or private bankers, or something similar) are looking out for their own interests first. And they often do this to the disadvantage of their clients’ interests.

Investment advisers break the law in pursuit of their own interests with alarming frequency. And the most common sin is selling investment products that weren’t suitable for the customer. That might mean putting your grandmother, or maybe their own grandmother, into a high-risk growth stock, when all she’s looking for is income. This is followed by things like “misrepresentation” and “omission of key facts.” And then the big ones, “fraud” and “unauthorised activity.”

There are a few ways to defend yourself against bad advisers. One way is to avoid them altogether, and chart your own financial future.

Another is to use them for ideas… but not to rely on them. Only you are responsible for your money… anyone else won’t truly have your best interests in mind.

Dangerous Myth #3: “Dividends don’t really matter.”

Some investors believe that dividends don’t matter… that a few additional percentage points of return doesn’t make a lot of difference.

But if you’re a mere investment mortal, dividends are central to your returns. Over the past ten years, in many markets, dividends have been the only thing separating you from making money, or losing it.

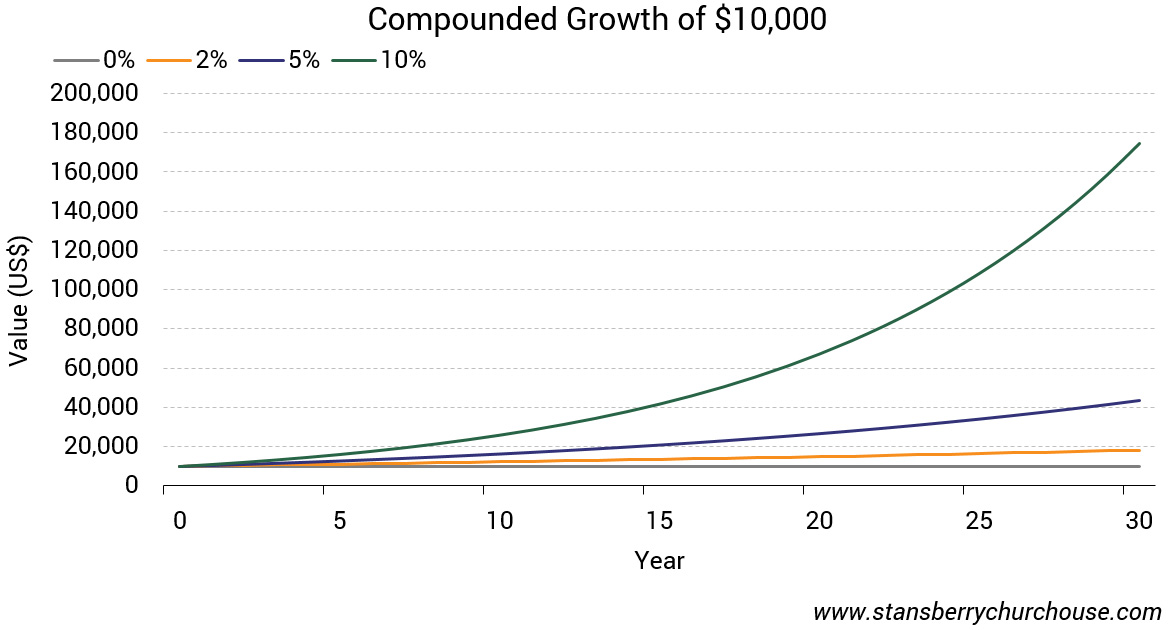

I’ll explain this in a minute. But first, understanding how a seemingly lousy 3 or 4 percent dividend yield can make such a big difference is a function of the most powerful force in finance: Compound interest.

Here’s how compounding works… you invest a sum of money that generates a steady return. But instead of taking that return and spending it, you reinvest it by buying more of the original investment. The next year both the original investment and the reinvested interest will earn interest, which you again reinvest.

With compounding, your original investment is growing in size due to repeated reinvestment, and every year you are getting a larger and larger sum of interest. It’s like a snowball rolling downhill, growing bigger in size as it picks up more snow on the way.

Let’s say an investor puts US$10,000 in a deposit paying a 5 percent dividend annually.

At the end of the first year, he is paid US$500. But instead of taking this dividend out of his account, he reinvests the US$500 on the same terms.

At the end of the second year, he’ll receive a dividend of US$525 (5 percent on US$10,000 + 5 percent on US$500). He reinvests this, and the invested amount grows to $11,025.

At the end of the third year, the investor will receive US$551.25 in dividends. His investible sum has now grown to US$11,576.25. Note the similarity to a snowball… the money that is working for the investor is growing larger every year.

The amount the investor receives every year is increasing due to the magical effect of compounding.

This is why investors who opt to re-invest their dividends, rather than pocket the income, will have far better investment returns.

How important are dividends? In some markets, over the past 10 years, dividends have accounted for more of your return, over the long term, than capital appreciation. Yes… that measly 3 percent yield contributed more to returns, than the actual price appreciation of the underlying stock or market. And in a few markets, investors would be losing money if not for dividends.

UBS Wealth Management Combination Makes It King

As shown in the figure above, over the past 10 years Chinese stocks returned 0.4 percent per year, based solely on capital appreciation. But reflecting compounded dividends, they returned 2.9 percent annually.

Meanwhile, Asia Pacific ex Japan stocks returned just 0.7 percent of their value on the basis of capital appreciation. But with compounded dividends, they returned 3.4 percent.

Aging Infrastructure Accelerates Water Crisis

The U.S. is the only market where you would have made more through simple capital appreciation than compounded dividends – thanks to the country’s long bull market.

The difference in performance is astounding – and is one reason why investors should include high-quality dividend stocks in their portfolio.

Remember, it might look like another 3 or 4 percent isn’t worth paying attention to. But it could make all the difference, and also help you generate enormous returns over time.