Tweedy Browne Fund commentary for the third quarter ended September 30, 2022.

Q3 2022 hedge fund letters, conferences and more

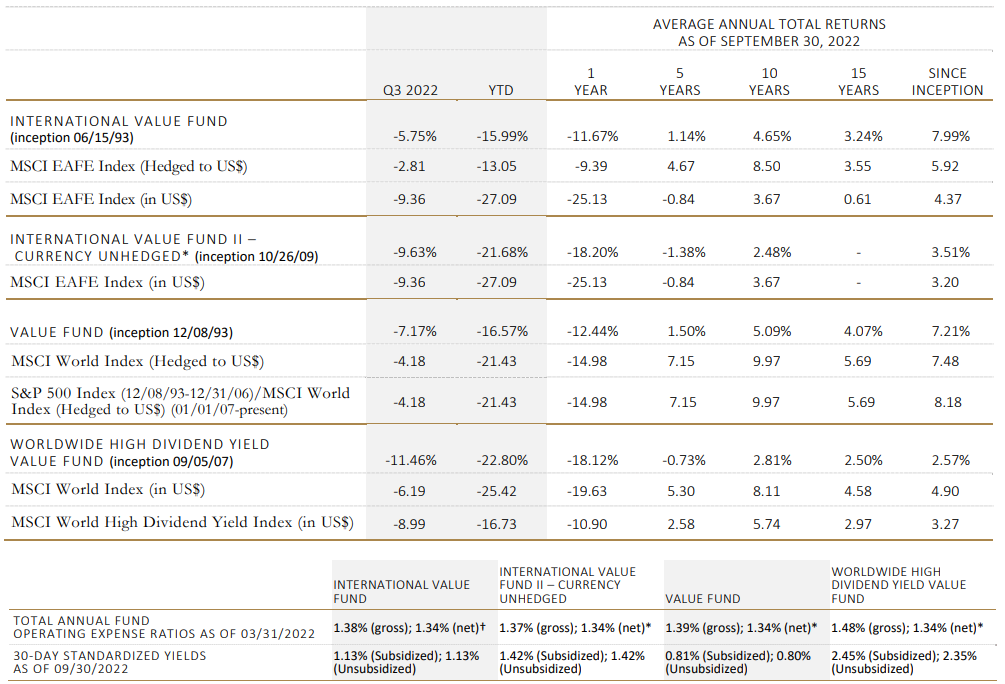

The performance data shown above represents past performance and is not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted.

Tweedy, Browne has voluntarily agreed, effective May 22, 2020 through at least July 31, 2023, to waive the International Value Fund’s fees whenever the Fund’s average daily net assets (“ADNA”) exceed $6 billion. Under the arrangement, the advisory fee payable by the Fund is as follows: 1.25% on the first $6 billion of the Fund’s ADNA; 0.80% on the next $1 billion of the Fund’s ADNA (ADNA over $6 billion up to $7 billion); 0.70% on the next $1 billion of the Fund’s ADNA (ADNA over $7 billion up to $8 billion); and 0.60% on the remaining amount, if any, of the Fund’s ADNA (ADNA over $8 billion). The performance data shown above would have been lower had fees not been waived pursuant to this arrangement from May 22, 2020 onwards.

* Tweedy, Browne has voluntarily agreed, effective December 1, 2017 through at least July 31, 2023, to waive a portion of the International Value Fund II’s, the Value Fund’s and the Worldwide High Dividend Yield Value Fund’s investment advisory fees and/or reimburse a portion of each Fund’s expenses to the extent necessary to keep each Fund’s expense ratio in line with the expense ratio of the International Value Fund. (For purposes of this calculation, each Fund’s acquired fund fees and expenses, brokerage costs, interest, taxes and extraordinary expenses are disregarded, and each Fund’s expense ratio is rounded to two decimal points.) The net expense ratios set forth above reflect this limitation, while the gross expense ratios do not. The International Value Fund II’s, Value Fund’s and Worldwide High Dividend Yield Value Fund’s performance data shown above would have been lower had certain fees and expenses not been waived and/or reimbursed during certain periods.

The Funds do not impose any front-end or deferred sales charges. The expense ratios shown above reflect the inclusion of acquired fund fees and expenses (i.e., the fees and expenses attributable to investing cash balances in money market funds) and may differ from those shown in the Funds’ financial statements.

COMMENTARY

Despite a rather impressive summer rally that saw US and international equity market indices recover a significant portion of their 2022 declines, markets once again fell into turmoil in August and September as August inflation data offered little prospect for a “Fed pivot.” By quarter-end, many market indices had broken through their previous market lows and were trading well into bear market territory.

In this volatile environment, the Tweedy, Browne Funds trailed their respective primary benchmark indices for the quarter. Both the International Value Fund’s and Value Fund’s policies of hedging perceived foreign currency exposure back into the US dollar provided significant protection against return dilution from declining foreign currencies during the quarter. This was critically important during a period when the pound, the euro and the yen were in free fall. (Near quarter end, all three of these major currencies were trading at multi-decade lows against the US dollar.)This also in part accounted for the International Value Fund’s outperformance of the unhedged MSCI EAFE Index by 361 basis points. The Value Fund’s hedging policy also provided protection against declining foreign currencies during the quarter, but it was unable to best either the hedged or unhedged MSCI World Index.

More often than not, when equity markets have been in decline, as they have been over the last year, value-oriented investments have generally tended to hold up a bit better than broader market indexes. In this respect, the Tweedy, Browne Funds on the whole did not disappoint. For the year-to-date and one year periods ending September 30, the International Value Fund II, Value Fund, and Worldwide High Divided Yield Value Fund bested their respective benchmarks. While the International Value Fund underperformed its hedged benchmark for the year-to-date and one year periods, it outperformed the unhedged MSCI EAFE Index by 1110 and 1346 basis points respectively.

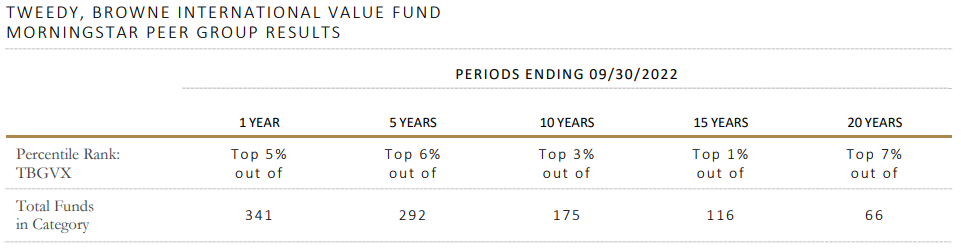

As you can see from the peer group comparison chart below, the International Value Fund continues to rank near the top of its peer group (Morningstar Foreign Large Value Funds) in virtually every standardized reporting period.

Morningstar has ranked the International Value Fund among its peers in the Foreign Large Value Category. Percentile rank in a category is the Fund’s total-return percentile rank relative to all funds that have the same Morningstar Category. The highest (or most favorable) percentile rank is 1 and the lowest (or least favorable) percentile rank is 100. The top-performing fund in a category will always receive a rank of 1. The “out of” number represents the total number of funds in the category for the listed time period. Percentile rank in a category is based on total returns, which include reinvested dividends and capital gains, if any, and exclude sales charges. Rankings may have been lower had fees not been waived from May 22, 2020 onwards. The preceding performance data represents past performance and is not a guarantee of future results.

PERFORMANCE ATTRIBUTION

Please note that the individual companies discussed herein were held in one or more of the Funds during the quarter ended September 30, 2022, but were not necessarily held in all four of the Funds. Please refer to each Fund’s portfolio page, beginning on page 5, for selected purchase and sale information during the quarter and the footnotes on page 14 for each Fund’s respective holdings in each of these companies as of September 30, 2022.

Rising inflation and interest rates, increasing prospects for a global recession, spiking energy prices, collapsing foreign currencies and the ongoing war in Ukraine continued to roil global equity markets, and in turn, our Fund portfolios during the quarter. Most sectors, industry groups (with the exception of energy), countries and individual securities faced declines during the period. While there were a few bright spots, they were few and far between.

While the majority of the Funds’ portfolio companies continued to make financial progress during the quarter, profit margins at many of them began to come under some pressure due to factors such as rising input costs. Some of the decline in stock prices at many of these companies was also tied to multiple contraction in the face of rising interest/discount rates, as opposed to deteriorating fundamentals. In addition, several of the Funds’ investments in Chinese equities, particularly a few of the dominant Chinese internet companies, remained under pressure due to uncertainties around government intervention and a slowdown in growth associated with China’s aggressive COVID lockdown policies.

Returns for the quarter were led by solid results from a number of our branded consumer product holdings, including Diageo, Heineken, Coca-Cola FEMSA, and Unilever; strong returns from biotech holdings, Ionis Pharmaceutical and Vertex Pharmaceutical; banks such as DBS Group, United Overseas Bank, and Wells Fargo; and machinery companies, CNH Industrial and Krones. In contrast, we had disappointing returns from the Funds’ airfreight and logistics holdings, FedEx and Deutsche Post; technology-related companies such as Alphabet, Intel, and Chinese tech giants, Alibaba, Baidu, and Tencent; media companies including Comcast, Megacable, and Paramount; and pharmaceutical companies, GSK (formerly GlaxoSmithKline) and Johnson & Johnson. Fresenius Medical, Verizon, SCOR, and CK Hutchison also were negative contributors.

PORTFOLIO ACTIVITY

Portfolio activity slowed somewhat on the buy-side during the quarter, but we did establish a few new positions including Husqvarna, the Swedish distributor of outdoor power tools including robotic lawnmowers; KBC, the Belgian bank that enjoys a strong banking franchise in Belgium and in central and eastern Europe; and Nihon Kohden, the Japanese based company that develops, manufactures and sells medical equipment, transformers, and power switches. In our view, these newly added positions were trading at significant discounts from our conservative estimates of their underlying intrinsic values at purchase, had solid balance sheets that should allow them to weather economic storms, appear to be positioned to benefit from future runways of potential growth, and in the case of Husqvarna and KBC, knowledgeable insiders had recently purchased shares at or around the prices we were paying for the Funds’ shares.

On the sell-side, we sold our remaining shares in BASF, the German chemical giant; Bollore, the French holding company; JD.com, the Chinese internet commerce company; Orange, the French utility company; and A-Living, the Chinese property management company. The stock prices of these businesses had either reached our estimates of underlying intrinsic values, or had been compromised in some way by virtue of declines in our estimates of their underlying intrinsic values and future growth prospects.

In addition to these buys and sales during the quarter, there were a number of additions to and trimming of existing positions.

PORTFOLIO POSITIONING AND OUTLOOK

Rising equity market volatility continues to churn up investment opportunities, particularly in non-US equity markets where many stocks, in our view, are currently priced for Armageddon. As a result of this ongoing volatility, our fund portfolios over the last year have been in the process of becoming refreshed with a significant number of new stocks, including an increasing number of smaller and medium capitalization European and Asian-based companies. In many, if not most, of these new investments, knowledgeable insiders have been actively purchasing shares at or around the prices we are paying. This alignment of interests between knowledgeable insiders, i.e. c-suite executives and key directors, and outside investors is particularly comforting in the highly uncertain investment environment we find ourselves in today. “Coattailing” insiders who are purchasing shares believed to be undervalued has empirically been shown to often be a profitable investment strategy.

The opportunity set being presented to us today in non-US equities is one of the best we have seen in well over a decade. As a result, we continue to believe that our Funds are well positioned for what could be a period of relative prosperity for our style of investing.

As Jason Zweig recently pointed out in his “The Intelligent Investor” column in The Wall Street Journal,

The obvious negatives are already priced in: a prolonged war in Ukraine, an acute energy crisis and raging inflation, a brutal recession, floundering currencies. With pessimism this pervasive, it wouldn’t take many positive surprises to overturn the obvious—and make global diversification lucrative again.

Where You Can Find Stock Market Bargains

The Wall Street Journal | September 16, 2022

Thank you for investing with us.

Roger R. de Bree, Andrew Ewert, Frank H. Hawrylak, Jay Hill,

Thomas H. Shrager, John D. Spears, Robert Q. Wyckoff, Jr.

Investment Committee

Tweedy, Browne Company LLC

October 2022