FORECASTS & TRENDS E-LETTER

by Gary D. Halbert

May 8, 2018

- Treasury Borrowing Hit Record $488 Billion in 1Q

- Why Deficits Could be Worse Than the CBO’s Estimates

- Trillion Dollar Deficits to Become the “New Normal”

- When It Comes to Debt, US Stands Alone in Developed World

[REITs]

Q1 hedge fund letters, conference, scoops etc, Also read Lear Capital: Financial Products You Should Avoid?

Treasury Borrowing Hit Record $488 Billion in 1Q

The Treasury Department announced last week that the government borrowed a record $488 billion in the January-March quarter. The Treasury said that actual borrowing in the 1Q exceeded the old record of $483 billion set in the first quarter of 2010 – the period when the country was struggling to pull out of a deep recession and prop-up the financial system following the 2008 financial crisis.

What makes the just passed quarter particularly troubling is that there was no crisis, no major alarming events and not even a recession. In fact, in the first quarter US GDP rose by 2.3% according to the Commerce Department amid what experts said was a global coordinated recovery.

President Trump’s tax cuts, the two-year budget deal that led to higher spending caps for this year and next and the $1.3 trillion fiscal 2018 omnibus spending bill are the main contributors to the worsening fiscal picture compared to last year. In addition, several rounds of supplemental appropriations for the relief efforts after three major hurricanes in 2017 have contributed to the bloated federal spending this year.

What is scary is how fast the US is ramping up federal debt. In the first six months of the fiscal year, October 2017-March 2018, the US budget deficit rose to $600 billion as spending increased at three times the pace of revenue growth. If that growth rate were to continue, the US deficit would soar to $1.2 trillion for FY2018.

Fortunately, the Treasury said it expects it will only need to borrow $75 billion in the current quarter. Still, the Congressional Budget Office forecasted in April that the budget deficit for FY2018 will hit $804 billion, up $241 billion from its previous estimate of $563 billion last year.

Why Deficits Could be Worse Than the CBO’s Estimates

In April, the Congressional Budget Office revised its estimates of the annual budget deficits for FY2018 to FY2028. The revisions were substantially higher than its forecast last year. In addition to the increase for FY2018 noted above, the CBO increased the deficit estimate for FY2019 to $981 billion, up from $689 billion forecast last year.

The CBO now forecasts that the annual budget deficit will top $1 trillion by 2020 and remain above a trillion in each year thereafter until at least 2028 (see below). If accurate, that means the national debt, now at just over $21 trillion, will be well above $30 trillion by 2028. This is mindboggling! And it could turn out to be even worse.

A new report from the non-partisan Tax Policy Center (TPC) says that as grim as those projections from the CBO may be, they probably understate the case.

The TPC argues that in several instances, the CBO’s economic and political assumptions are overly optimistic, and that more realistic scenarios produce even larger deficit projections. A more negative outlook emerges once TPC makes more realistic adjustments for:

- Recession Risk: The CBO assumes the economy will be at full employment on average for the next 10 years. A more realistic outlook would include the likelihood of a recession at some point, which would significantly reduce federal revenues and increase expenses, producing a larger deficit.

- Permanent Tax Cuts: The CBO assumes that the temporary individual tax cuts will be allowed to expire after 2025, but there’s a good chance that Congress will extend them, largely for political reasons. If lawmakers do extend the cuts, the debt-to-GDP ratio will reach 106.5 percent in 2028, well above the CBO’s current projection of 96 percent.

- The Long Term: The CBO analysis stops at 2028, but the fiscal outlook gets worse beyond the 10-year window. As the deficits grow larger, the spending cuts required to bring them back to the current level relative to GDP grow larger as well. The TPC argues:

“The longer policy makers wait to institute changes, the larger those adjustments would have to be to hit a given debt target in a given year. Moreover, over a longer [time] horizon, the required annual adjustments are much larger, because the projected fiscal trajectory under current policy continues to deteriorate.”

While no one knows for sure what the future holds, I think the Tax Policy Center makes some very important points, especially the fact that the CBO does not include a recession in its long-term forecasts. It is almost certain we will experience another recession in the next 10 years.

Trillion Dollar Deficits to Become the “New Normal”

As noted above, the Congressional Budget Office updated its annual budget deficit forecasts in early April. In addition to raising its estimate of the FY2018 budget deficit from $563 billion to $804 billion, here are its estimates for FY2019 to FY2028:

| 2019 | $981 billion | 2024 | $1.244 trillion | |

| 2020 | $1.008 trillion | 2025 | $1.352 trillion | |

| 2021 | $1.123 trillion | 2026 | $1.320 trillion | |

| 2022 | $1.276 trillion | 2027 | $1.316 trillion | |

| 2023 | $1.273 trillion | 2028 | $1.526 trillion |

As you can see, the deficit rises to above $1 trillion in FY2020 and never falls below it. If the CBO is remotely correct, the deficit rises by more than 50% to $1.56 trillion by 2028. Again, this assumes no recession in the next decade, which is absurd.

Sadly, most Americans have not seen the latest CBO deficit projections and are oblivious to the fact that our annual deficits will be above $1 trillion in the years ahead. Even worse, I’m not sure how many of our elected officials in Washington really know. Of those who do, I wonder how many even care.

Yet there are real consequences to this mounting debt. First, unless lawmakers control their spending addiction, the United States will have less flexibility to pump up the economy during a downturn or an emergency.

Second, as a new study by economists at the Federal Reserve Bank of Dallas finds, a rising public debt-to-GDP ratio harms economic growth. The study looked at a panel of 40 advanced and emerging economies and four decades of data. The economists found that “a persistent accumulation of public debt over long periods is associated with a lower level of economic activity.”

In other words, more debt means lower growth and ultimately fewer employment opportunities for future generations. That’s because the debt has a negative impact on private-sector investment, productivity, wages and interest rates. This nasty combo will necessarily mean significantly higher income taxes in the years ahead, of course.

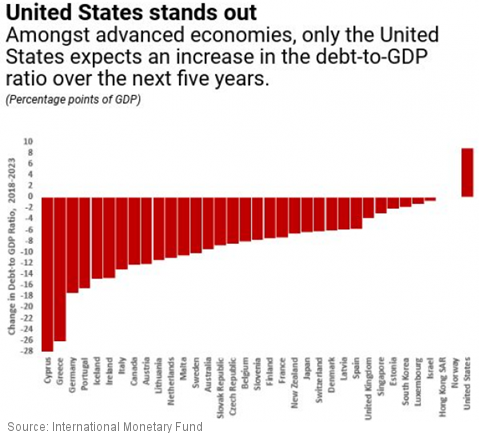

When It Comes to Debt, US Stands Alone in Developed World

Here’s another fact you probably won’t read anywhere else. When it comes to our exploding national debt, the US stands alone among the advanced economies, since virtually all developed nations are expected to reduce their debt-to-GDP ratios over the next half decade — following years of rising debt in the wake of the global financial crisis. The US is the only developed country that is increasing its debt-to-GDP ratio rather than reducing it. Take a look:

Keep in mind that almost all of these nations are increasing their debt, but they are slowing the pace of adding to their debt (ie – reducing their debt-to-GDP ratios), except the US.

The International Monetary Fund’s latest global fiscal survey warns that in five years, the US debt-to-GDP ratio will be higher than Italy’s, a nation well-known for spending beyond its means. The IMF estimates that the US debt ratio will rise to 116.9% by 2023, while Italy’s will fall slightly to 116.6% — and these figures only represent “debt held by the public,” not total national debt.

Finally, I’ll leave you with one last thought that I don’t have space to go into today, but will come back to just ahead. Question: Who are the largest buyers of US government debt? The Federal Reserve, China and Japan. All three are in the process of cutting back on their purchases of US debt.

Which raises the question of how the US is going to run trillion dollar deficits if its major lenders are cutting back on their Treasury purchases. This is a potential train wreck in the making! Think sharply higher interest rates. Think recession. Think a bear market in stocks and bonds. I’ll have more to say about this just ahead.

Of course, I don’t know when these bad things will happen. No one does. My best advice is to diversify your portfolio including some of the alternative investments we offer at Halbert Wealth Management that have the potential to make money in a falling market.

I would also recommend you look at some of the investments we offer that do not include stocks or bonds. We have professional money managers with strategies that invest in various types of real estate, real estate loans, longevity assets, derivatives, options, etc.

To learn more about these alternative investment strategies, call Phil Denney or Spencer Wright at 800-348-3601. You’ll be glad you did.

All the best,

Gary D. Halbert

Gary’s Between the Lines Blog: Americans Hoarding Money in Checking Accounts